DSCR Loan for Portfolio Investors: Your Path to Multi-Property Success

Portfolio investors face unique challenges when scaling their real estate holdings. Traditional mortgage products often create bottlenecks with personal income verification requirements and strict debt-to-income ratios. A DSCR loan for portfolio investors offers a different approach, focusing on property cash flow rather than personal financial statements.

This financing strategy has evolved significantly, with 2026 bringing new product innovations that could reshape how investors approach multiple property acquisitions. Understanding these changes might be the key to unlocking your portfolio's growth potential.

Essential DSCR Qualification Requirements for Portfolio Growth

Essential DSCR qualification requirements for portfolio growth center on property performance rather than personal income documentation. The qualification process typically evaluates how well each property's rental income covers its mortgage obligations.

Property cash flow analysis: Lenders examine rental income versus mortgage payments, with ratios often needing to exceed 1.0 to demonstrate positive cash flow

No traditional income verification: W-2s, tax returns, and employment letters may not be required, streamlining the application process for busy investors

Credit score requirements: Most programs require credit scores in the mid-600s range, though specific thresholds can vary by lender

Down payment expectations:Portfolio investors might need to provide 20-25% down payments, depending on the property type and loan program

Cash Flow Strategies That Maximize DSCR Performance

Cash flow strategies that maximize DSCR performance help portfolio investors present stronger loan applications and secure better terms. These approaches focus on optimizing the relationship between rental income and debt service.

Market rent analysis: Research comparable properties to ensure rental rates reflect current market conditions and support loan qualification

Expense optimization: Review property management costs, maintenance reserves, and operational expenses to improve net operating income

Lease structure improvements: Consider longer-term leases or rent escalation clauses that demonstrate stable cash flow to lenders

Property condition upgrades: Strategic improvements might justify higher rents and strengthen the debt service coverage ratio

Multiple Properties Financing Approach

Multiple properties financing approach requires careful coordination to maximize efficiency while managing risk across your portfolio. Each property typically needs to qualify independently under DSCR guidelines.

Sequential acquisition strategy: Plan property purchases to allow time for seasoning and cash flow stabilization between acquisitions

Geographic diversification considerations: Spreading investments across different markets might reduce concentration risk and appeal to lenders

Property type mixing: Combining single-family rentals with small multifamily properties could provide portfolio balance

Refinancing coordination: Time existing loan refinances to align with new acquisition financing for better overall portfolio management

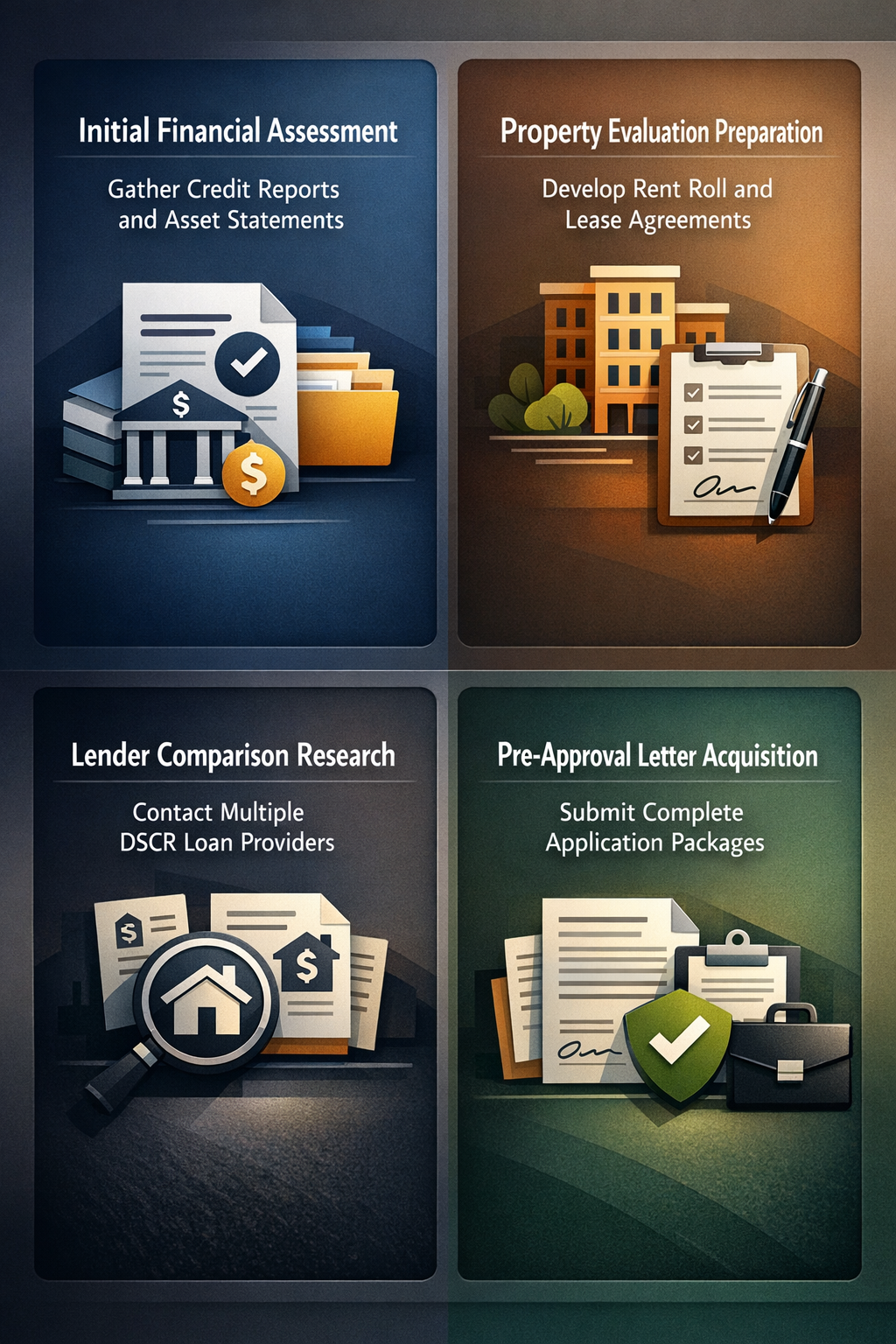

Step-by-Step Pre-Approval Process for Investors

Step-by-step pre-approval process for investors helps streamline property acquisitions and positions you competitively in fast-moving markets. The 2026 guidelines emphasize preparation and documentation efficiency.

Initial financial assessment: Gather credit reports, asset statements, and existing property documentation to establish your baseline qualification profile

Property evaluation preparation: Develop rent roll documentation, lease agreements, and market rent analyses for properties you plan to finance

Lender comparison research: Contact multiple DSCR loans providers to understand their specific requirements, rates, and portfolio lending policies

Pre-approval letter acquisition: Submit complete application packages to secure pre-approval letters that demonstrate your financing capacity to sellers

Innovative DSCR products reshaping portfolio scaling have emerged as the lending landscape evolves to meet investor needs. These developments could provide new opportunities for efficient portfolio growth.

Hybrid financing structures: Some lenders now offer products that combine DSCR evaluation with limited personal income verification for enhanced qualification flexibility

Portfolio-level underwriting: Rather than evaluating each property separately, some programs assess the overall portfolio performance and cash flow stability

Streamlined documentation processes: Digital platforms and automated valuation models might reduce the time and paperwork required for loan approval

Flexible seasoning requirements: New products may offer reduced waiting periods between property acquisitions, allowing faster portfolio expansion

Key Considerations for Successful Portfolio Management

Key considerations for successful portfolio management extend beyond initial loan approval to long-term investment strategy and risk management. These factors often determine whether your DSCR loan strategy delivers sustained results.

Market conditions play a significant role in portfolio performance, as rental rates and property values affect both cash flow and refinancing opportunities. Investors typically benefit from staying informed about local market trends and maintaining relationships with property management professionals who understand DSCR loan requirements.

Additionally, maintaining adequate cash reserves becomes crucial when managing multiple properties with DSCR financing. Unexpected maintenance costs or vacancy periods could impact debt service coverage ratios, potentially affecting future financing opportunities. Successful portfolio investors often plan for these scenarios by maintaining conservative cash flow projections and building contingency funds.

A DSCR loan for portfolio investors represents a powerful tool for scaling real estate holdings efficiently. The focus on property cash flow rather than personal income creates opportunities for investors who might struggle with traditional financing constraints.

As lending products continue evolving, staying informed about new qualification requirements and innovative financing structures could provide competitive advantages. The key lies in understanding how these loans work within your broader investment strategy and preparing thorough documentation that demonstrates property performance.

Success with DSCR portfolio financing typically requires careful planning, realistic cash flow projections, and ongoing attention to property management quality. When executed thoughtfully, this approach might unlock significant growth potential for serious real estate investors.