Securing the right financing for investment properties can make or break your returns. Yet even experienced real estate investors often fall into traps that delay approvals, create leverage problems, or trigger costly refinancing headaches down the road.

Understanding the top investment property loan mistakes to avoid is essential for anyone pursuing DSCR loans, fix and flip financing, or rental property mortgages. The difference between a smooth closing and a stalled deal often comes down to preparedness and informed decision-making.

This guide examines the critical errors that can derail your investment strategy, drawing on real-world scenarios and lender expectations. You'll discover practical steps to prevent approval delays, optimize your leverage decisions, and sidestep refinance issues that could undermine your portfolio growth.

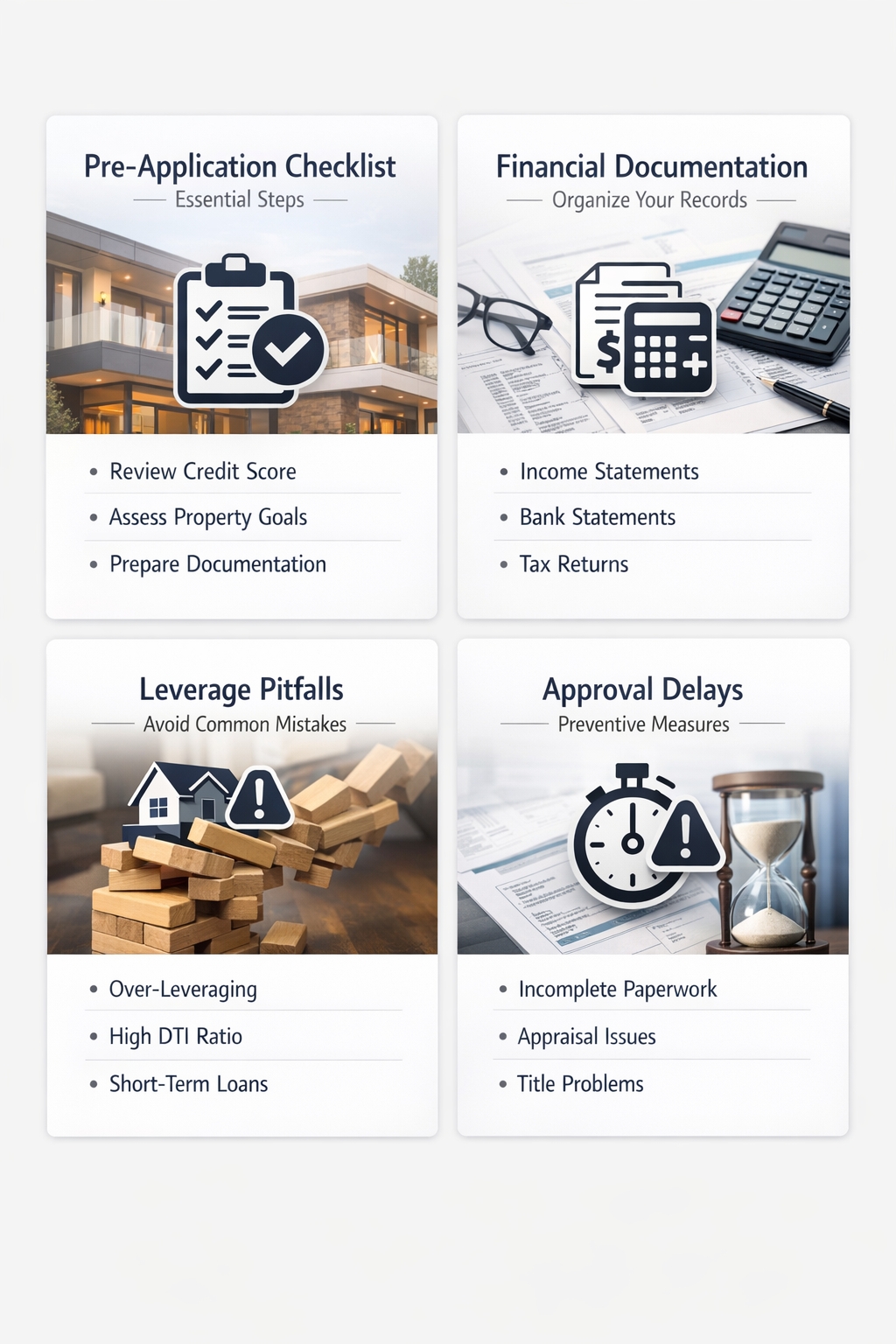

Pre-Application Due Diligence Checklist

Pre-application due diligence is where many real estate investors stumble before they even submit their first document. Skipping thorough research on a property can lead to approval delays that push back your entire investment timeline.

Conduct environmental assessments early: Potential environmental issues such as soil contamination or asbestos can stop a loan approval in its tracks. Identifying these problems before you apply helps prevent delays that could disrupt your acquisition or renovation schedule.

Verify zoning and permit compliance: Confirm that the property meets local zoning requirements and that any planned improvements won't require lengthy permit approvals. Lenders may hesitate if zoning conflicts exist.

Review property condition reports: Order inspections to uncover structural or mechanical issues that might impact the property's value or insurability. Surprises during underwriting often trigger re-negotiations or denials.

Confirm clear title and lien status: Title defects or outstanding liens can delay closing significantly. A preliminary title search reveals problems you'll need to resolve before lenders will proceed.

Taking these steps before applying for DSCR loans or bridge financing might seem time-consuming, but they typically save weeks or months of headaches later. Lenders appreciate borrowers who arrive prepared, and that preparation often translates into smoother approvals and better terms.

Financial Planning and Documentation Essentials

Incomplete or disorganized financial documentation is a leading cause of approval delays and poor loan terms. Real estate investors need to treat their loan application like a business proposal, not a casual inquiry.

Organize tax returns and financial statements: Have at least two years of personal and business tax returns ready, along with current profit and loss statements for any existing rental properties. Missing documents trigger requests for information that can push your timeline back weeks.

Prepare a clear investment plan: Develop a written strategy that outlines your acquisition criteria, expected cash flow, and exit options. Lenders want to see that you've thought through the numbers and understand the investment's risk profile.

Document all income sources: If you're relying on rental income from other properties or alternative income streams, compile lease agreements, bank statements, and rent rolls. DSCR loans focus on property cash flow, so proving consistent income is critical.

Maintain sufficient reserves: Many lenders require several months of reserves to cover mortgage payments, insurance, and maintenance. Having liquid assets ready demonstrates financial stability and reduces lender risk.

A well-defined financial plan helps you avoid poor leverage decisions by clarifying how much debt your portfolio can realistically support. Emotion-driven investments without solid financial backing often lead to over-leverage and refinancing problems when market conditions shift.

Common Leverage and Loan Structure Pitfalls

Choosing the wrong loan structure or taking on too much leverage ranks among the top investment property loan mistakes to avoid. Many investors focus solely on getting approved without considering whether the terms align with their investment strategy.

Avoid over-leveraging your portfolio: Borrowing the maximum amount might seem attractive, but it leaves little cushion for vacancies, repairs, or market downturns. Conservative leverage typically provides more flexibility and lower refinance risk.

Match loan terms to your investment horizon: Short-term bridge loans work well for fix and flip projects, while longer-term rental property loans suit buy-and-hold strategies. Mismatching your financing to your timeline can create unnecessary refinance pressure.

Consider prepayment penalties and flexibility: Some investment property loans include steep penalties for early payoff. If you plan to sell or refinance within a few years, these penalties could eat into your profits.

Evaluate rate types carefully: Adjustable-rate mortgages may offer lower initial payments but can increase your costs significantly over time. Fixed rates provide predictability that helps with long-term cash flow planning.

Poor leverage decisions often stem from focusing on acquisition rather than ongoing operations. Running scenarios that account for vacancy rates, maintenance costs, and potential rate increases helps you select loan structures that support sustainable growth rather than creating future problems.

Steps to Prevent Approval Delays

Approval delays frustrate investors and can cause you to miss time-sensitive opportunities. Following a systematic approach to your loan application helps keep the process moving forward.

Notify your lender about any financial changes: If your employment status, income sources, or credit profile changes during the application process, inform your lender immediately. Discovering these changes during underwriting can halt your approval and require starting portions of the process over.

Respond to lender requests promptly: When underwriters ask for additional documentation or clarification, provide it within 24 to 48 hours. Delays on your end compound and can push your closing date back significantly.

Avoid making major financial moves: Don't open new credit accounts, make large purchases, or change bank accounts while your loan is being processed. These actions can trigger additional review and verification requirements.

Work with experienced loan officers: Lenders who specialize in investment property financing understand common issues and can guide you through potential obstacles before they become problems. Their expertise often prevents delays that less experienced loan officers might miss.

Build in timeline buffers: Even with perfect preparation, unexpected issues can arise. Plan for your financing to take longer than the minimum estimate, especially if you're using a loan product you haven't used before.

These preventive steps are particularly important when dealing with DSCR loans or other investor-focused products, where underwriting requirements may differ from conventional mortgages. Clear communication and responsiveness typically separate smooth closings from frustrating delays.

Refinancing Strategy and Timing Considerations

Refinance issues often catch investors off guard, especially when they haven't planned for changing market conditions or evolving lender requirements. Strategic thinking about future refinancing needs should begin when you take out your initial loan.

Monitor current loan guidelines and market rates: Investment property loan requirements and interest rates shift over time. Staying informed helps you identify optimal refinancing windows and understand what documentation you'll need when that time comes.

Track your property's cash flow performance: For DSCR loans, your refinancing options depend heavily on the property's debt service coverage ratio. Maintaining strong rental income and controlling expenses improves your refinancing position.

Plan for seasoning requirements: Many lenders require you to hold a property for six to twelve months before refinancing. Understanding these timelines prevents situations where you need to refinance but don't qualify due to insufficient ownership history.

Consider rate-and-term versus cash-out refinancing: Rate-and-term refinancing typically faces fewer restrictions, while cash-out refinancing may require higher credit scores, lower loan-to-value ratios, and more reserves. Know which type you'll need and plan accordingly.

Build relationships with multiple lenders: Having options when refinancing time arrives gives you negotiating power and backup plans. Don't wait until you need to refinance to start exploring your options.

Refinance issues frequently stem from investors treating their initial loan as permanent when it should be viewed as one step in an evolving financial strategy. Market conditions change, property values fluctuate, and lender appetites shift, so flexibility in your refinancing approach protects your investment returns.

Emotional Decision-Making and Investment Discipline

Letting emotions drive your financing decisions represents one of the most damaging mistakes real estate investors make. Excitement about a property or fear of missing out can lead to hasty loan commitments that don't serve your long-term interests.

Establish clear investment criteria before shopping: Define your target cash-on-cash return, acceptable debt service coverage ratios, and maximum loan terms before you start looking at properties. Having these parameters in place helps you evaluate opportunities objectively.

Run the numbers independently: Don't rely solely on seller projections or optimistic rental estimates. Verify income potential using comparable properties and conservative vacancy assumptions to ensure the loan structure makes financial sense.

Resist pressure to accept suboptimal terms: If a lender offers terms that don't meet your criteria, walk away and keep searching. The short-term disappointment of passing on a deal beats the long-term pain of struggling with an inappropriate loan structure.

Separate property excitement from financial reality: You might love a property's location or potential, but if the financing doesn't support your investment thesis, it's the wrong deal. Successful investors prioritize numbers over feelings.

Build decision-making frameworks: Create checklists or scoring systems that help you evaluate both properties and financing options consistently. This systematic approach reduces the influence of emotional factors on critical decisions.

Real estate investors who maintain discipline around their financing strategy tend to build more resilient portfolios. They avoid over-extending themselves during hot markets and can capitalize on opportunities when others are overleveraged and forced to sell.

Key Takeaways for Investor Success

Key takeaways for investor success center on preparation, discipline, and ongoing education. The top investment property loan mistakes to avoid share a common thread: they typically result from rushing the process or failing to understand how lender requirements align with your investment goals.

Successful real estate investors treat financing as a strategic tool rather than a simple transaction. They conduct thorough due diligence before applying, maintain organized financial records, and choose loan structures that support their specific investment strategy. They stay informed about changing market conditions and lender criteria, which helps them avoid approval delays and positions them for successful refinancing when the time comes.

Most importantly, they keep emotions in check and make decisions based on solid financial analysis rather than excitement or fear. This disciplined approach might mean passing on deals that don't meet their criteria, but it ultimately leads to a stronger, more profitable portfolio.

By focusing on these fundamentals and learning from common financing mistakes, you can navigate the investment property financing landscape more effectively and build the real estate portfolio you're working toward.

Avoiding the top investment property loan mistakes to avoid requires vigilance, preparation, and a commitment to making informed decisions. From conducting environmental assessments that prevent approval delays to developing emotion-free investment plans that optimize leverage, each step in the financing process matters.

Real estate investors who take time to understand lender expectations, organize their documentation, and align their financing choices with their investment strategy typically experience smoother transactions and better long-term results. They recognize that securing financing is just one component of successful real estate investing, but it's a component that can significantly impact overall returns.

Whether you're pursuing DSCR loans for rental properties or bridge financing for fix and flip projects, the principles remain consistent: do your homework, communicate clearly with lenders, and make decisions based on financial fundamentals rather than emotions. These practices help you avoid the pitfalls that derail less prepared investors and position you for sustained success in real estate investing.