DSCR Loan for Portfolio Expansion Strategy: A Guide for Real Estate Investors

Scaling a rental property portfolio requires more than just capital. It demands a financing strategy that adapts to your growth trajectory while maintaining healthy cash flow across multiple properties. For real estate investors serious about expansion, a DSCR loan for portfolio expansion strategy offers a pathway that emphasizes rental income over traditional borrower income documentation.

Unlike conventional mortgages that scrutinize personal tax returns and W-2s, DSCR loans evaluate properties based on their ability to generate revenue. This distinction matters significantly when you're acquiring your third, fifth, or tenth rental property. The shift from borrower-centric to property-centric underwriting can streamline approvals and accelerate your acquisition timeline.

In this guide, we'll explore how investors can use DSCR financing to build sustainable rental portfolios, structure loans for maximum scalability, and leverage equity extraction for reinvestment. Whether you're considering your next single property or planning a multi property financing approach, understanding DSCR loan mechanics is essential for measured, profitable growth.

What Makes DSCR Loans Different for Scaling Rentals?

What makes DSCR loans different for scaling rentals is how they evaluate borrowing capacity. When expanding your portfolio, traditional lenders often hit you with income documentation hurdles that become more complex with each additional property.

Q: How does DSCR financing differ from conventional mortgages when scaling rentals?

DSCR loans focus on the property's rental income rather than your personal income documentation. This means the underwriting process evaluates whether the property generates enough cash flow to cover its debt service. For investors managing multiple properties, this approach may reduce the paperwork burden and potentially speed up approvals compared to conventional financing that requires extensive personal income verification for each acquisition.

The debt service coverage ratio itself is a straightforward metric: monthly rental income divided by monthly debt obligations. Lenders typically look for ratios above 1.0, indicating the property generates enough income to cover its mortgage payment. Some lenders may accept ratios slightly below 1.0 if other factors compensate, though requirements vary across institutions.

This property-focused underwriting can be particularly useful when your personal income documentation doesn't fully reflect your investment capacity. Self-employed investors, those with complex tax strategies, or individuals with income spread across multiple LLCs might find DSCR loans align better with their financial structure than conventional products.

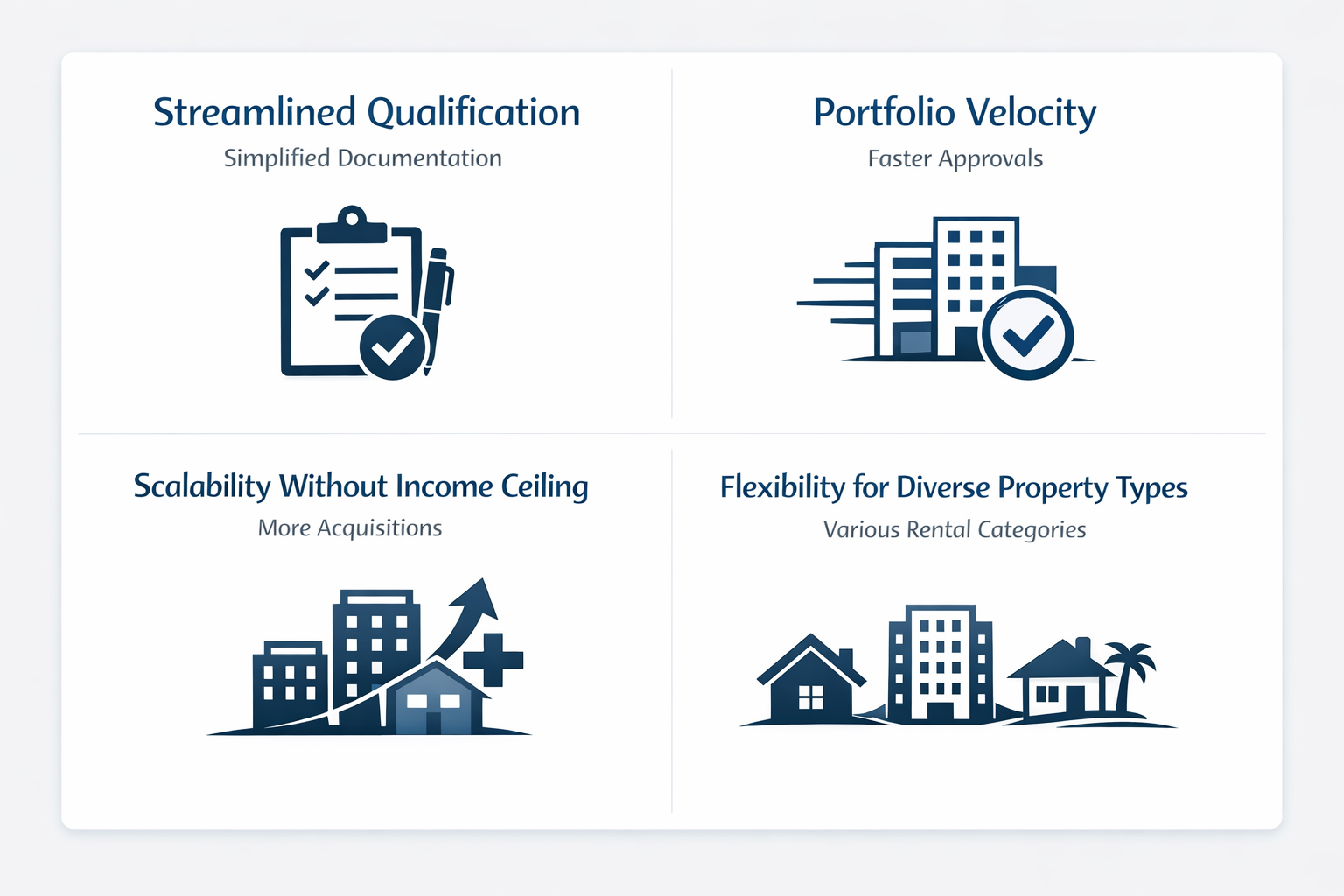

Key Benefits of Using DSCR Loans for Multi Property Financing

Key benefits of using DSCR loans for multi property financing extend beyond simplified documentation. When you're building a rental portfolio, the financing structure itself can either accelerate or constrain your growth trajectory.

Streamlined qualification process: DSCR loans may reduce the documentation burden for each subsequent property acquisition. Rather than compiling extensive personal income records for every deal, the focus shifts to rental income projections and property performance metrics.

Portfolio velocity: With potentially faster approvals, investors might close on multiple properties within shorter timeframes. This can be valuable in competitive markets where delays cost opportunities.

Scalability without income ceiling constraints: Traditional lending often imposes debt-to-income ratio limits that cap how many mortgages you can carry. DSCR financing typically evaluates each property individually, which may allow for more acquisitions as long as each property meets cash flow requirements.

Flexibility for diverse property types: DSCR loans can often be used across various rental property categories, from single-family homes to small multifamily units, allowing investors to diversify their holdings under a consistent financing approach.

These advantages position DSCR financing as a practical tool for investors focused on measured expansion. However, it's worth noting that DSCR loans may carry different rate structures or down payment requirements compared to conventional products, so the overall cost of capital should factor into your acquisition analysis.

Structuring Your DSCR Loan for Future Portfolio Growth

Structuring your DSCR loan for future portfolio growth requires thinking beyond the immediate acquisition. How you configure loan terms today can impact your flexibility for tomorrow's opportunities.

Optimize cash flow over payment minimization: While securing the lowest monthly payment might seem attractive, structuring loans to maintain strong cash reserves can provide acquisition capital for future deals. Balancing debt service with retained cash flow is central to sustainable scaling.

Consider loan-to-value positioning: Lower LTV ratios might offer better rates and terms, but they also tie up more capital per property. Higher LTV financing preserves capital for additional acquisitions but may increase overall borrowing costs. Your leverage approaches should reflect your growth timeline and risk tolerance.

Align amortization with hold strategy: If you plan to refinance or sell properties within a specific timeframe, interest-only periods or shorter amortization schedules might align better with your exit strategy than standard 30-year terms.

Build in refinance optionality: Some DSCR loan structures may include prepayment penalties or restrictions. Understanding these terms upfront helps you plan for future refinancing when you want to extract equity or improve terms.

The goal is to structure financing that supports both current acquisitions and future scalability. Each property should contribute to overall portfolio cash flow while maintaining enough liquidity to pursue the next opportunity when it arises.

Equity Extraction and Reinvestment Through DSCR Refinancing

Equity extraction and reinvestment through DSCR refinancing can accelerate portfolio expansion without requiring external capital sources. As properties appreciate and you pay down principal, the equity position in each asset grows.

Cash-out refinancing mechanics: DSCR cash-out refinances allow you to access accumulated equity while maintaining the property in your portfolio. This capital can fund down payments on additional properties, creating a self-sustaining growth cycle.

Strategic timing considerations: Refinancing decisions should account for current interest rate environments, property valuations, and your acquisition pipeline. Extracting equity when rates are favorable and you have identified strong acquisition targets can maximize the value of this strategy.

Portfolio-wide equity analysis: Rather than viewing each property in isolation, successful investors often analyze equity positions across their entire portfolio to identify which properties offer the best refinancing opportunities at any given time.

This leverage approach transforms static equity into active investment capital. However, refinancing does reset your loan terms and may increase debt service on the refinanced property, so the analysis should include how the new loan impacts property-level and portfolio-level cash flow.

Used strategically, DSCR refinancing can provide the capital needed for expansion without diluting ownership or bringing in partners. It's a tool that becomes more powerful as your portfolio matures and equity accumulates across multiple properties.

Single Property vs. Portfolio DSCR Loan Strategy: Which Fits Your Goals?

Single property vs. portfolio DSCR loan strategy presents different paths for investors at various stages of growth. Understanding when to use each approach can optimize your financing efficiency.

Single property DSCR loans: These involve financing each acquisition individually, with underwriting focused on that specific property's rental income and debt service coverage. This approach offers maximum flexibility, allowing you to shop rates for each deal and match loan terms to individual property characteristics. It works well for investors building portfolios one property at a time or those acquiring properties with different profiles.

Portfolio DSCR financing: Some lenders offer products that finance multiple properties under a single loan structure or evaluate your application considering your entire portfolio's performance. This might streamline the process when acquiring several properties simultaneously or refinancing multiple assets together. Portfolio approaches may provide efficiencies in closing costs and administrative overhead.

Hybrid strategies: Many investors use a combination, financing some properties individually while grouping others when it makes sense. This flexibility allows you to optimize for each situation based on property characteristics, market timing, and available terms.

Your choice between these strategies might depend on factors like your acquisition pace, whether you're buying properties in clusters or individually, and how lenders in your market structure their DSCR products. There's no universal right answer, but aligning your financing strategy with your investment goals and operational preferences can make portfolio management more efficient.

As your portfolio grows, the strategy that worked for properties one through five might need adjustment for properties ten through twenty. Staying flexible and reassessing your approach periodically keeps your financing aligned with evolving goals.

Managing Cash Flow and Stability Across Multiple DSCR-Financed Properties

Managing cash flow and stability across multiple DSCR-financed properties becomes increasingly important as your portfolio expands. Each property's debt service coverage needs to remain healthy while the overall portfolio maintains adequate reserves.

Maintain property-level performance tracking: Monitor each property's DSCR independently to identify underperformers before they impact your overall portfolio health. Properties with declining coverage ratios may need rent adjustments, expense reduction, or refinancing consideration.

Build portfolio-wide reserve funds: While DSCR loans evaluate properties individually, successful investors typically maintain reserves that account for portfolio-wide vacancy, maintenance, and market fluctuations. This buffer provides stability when individual properties experience temporary cash flow disruptions.

Diversify property types and markets: Spreading acquisitions across different property types or geographic markets can reduce concentration risk. If one market softens or one property type faces headwinds, diversification may help maintain overall portfolio stability.

Plan for cash flow cycles: Rental income isn't always perfectly steady. Lease renewals, seasonal markets, and turnover can create cash flow variations. Structuring your portfolio to account for these cycles helps maintain consistent debt service coverage even during temporary dips in individual property performance.

DSCR financing offers predictability because loan amounts are tied to rental income rather than fluctuating personal financial situations. This stability can be particularly valuable when navigating uncertain economic environments, as your financing remains anchored to property performance rather than external factors.

As you scale, developing systems to monitor and manage cash flow across all properties becomes essential. What works for two or three properties may not scale rental portfolios to ten or fifteen without more structured processes and potentially property management support.

A well-executed DSCR loan for portfolio expansion strategy can fundamentally change how you scale your rental property business. By shifting focus from personal income documentation to property performance, DSCR financing may remove traditional barriers that limit portfolio growth.

The most successful investors approach DSCR loans not just as financing tools, but as components of a broader expansion strategy. They structure loans to optimize cash flow, use refinancing to extract and redeploy equity, and choose between single property and portfolio approaches based on specific goals and market conditions.

Scaling rentals through multi property financing requires more than just access to capital. It demands careful attention to cash flow management, strategic leverage decisions, and ongoing portfolio performance monitoring. DSCR loans provide flexibility in these areas, but the ultimate success depends on how you integrate them into your overall investment approach.

Whether you're acquiring your next property or planning expansion to double-digit holdings, understanding how to structure and utilize DSCR financing can provide a competitive advantage. The property-centric underwriting, potential for equity extraction, and scalability without conventional income constraints make DSCR loans a practical option for serious real estate investors focused on measured, sustainable portfolio growth.

As with any financing decision, the specific terms, rates, and requirements will vary across lenders and market conditions. Evaluating multiple options and aligning your financing structure with your long-term investment goals remains essential for building a profitable, resilient rental portfolio.