How to Qualify for a Rental Property Loan Without Income

For many real estate investors, traditional mortgage qualification creates an unnecessary roadblock. If you're growing a rental portfolio, you might find yourself in a common bind: your properties generate strong cash flow, but your personal tax returns don't reflect traditional W-2 income. Perhaps you're self-employed, or maybe you've strategically written off expenses to minimize taxable income. Either way, conventional lenders often turn you away.

The good news? There's a path forward. Learning how to qualify for a rental property loan without income documentation has become increasingly accessible through debt service coverage ratio financing. These investor-focused products shift the qualification criteria from your personal earnings to what really matters: the property's ability to generate rental income.

This approach represents a fundamental shift in how investors can build their portfolios. Instead of being limited by personal income documentation, you can leverage the inherent value and cash flow potential of the properties themselves. Let's explore exactly how this works and what you need to position yourself for approval.

Understanding DSCR as a No Income Alternative

Understanding DSCR as a no income alternative starts with recognizing what sets this financing apart from traditional mortgages. DSCR loans evaluate the property's rental income against the proposed mortgage payment, taxes, insurance, and other carrying costs. If the property generates enough rent to cover these expenses, you may qualify regardless of your personal income situation.

The property's rental income serves as the primary qualification metric, not your W-2 earnings or tax returns

Lenders typically calculate DSCR by dividing monthly rental income by the total monthly debt obligations on the property

This model allows investors to expand their portfolios based on deal quality rather than personal income limits

No tax return financing through DSCR products eliminates the need for extensive personal financial documentation

This shift in underwriting philosophy aligns perfectly with how savvy investors actually operate. You're not buying a home to live in; you're acquiring an income-generating asset. The lender's risk is mitigated by the property's cash flow, not your salary. This represents one of the most significant innovations in investor financing over the past decade.

The mechanics are straightforward but powerful. When you apply for a DSCR loan, the lender orders an appraisal that includes a rental analysis. This analysis estimates the property's market rent, which becomes the income figure used for qualification. If that rental income adequately covers the debt service, you're on your way to approval.

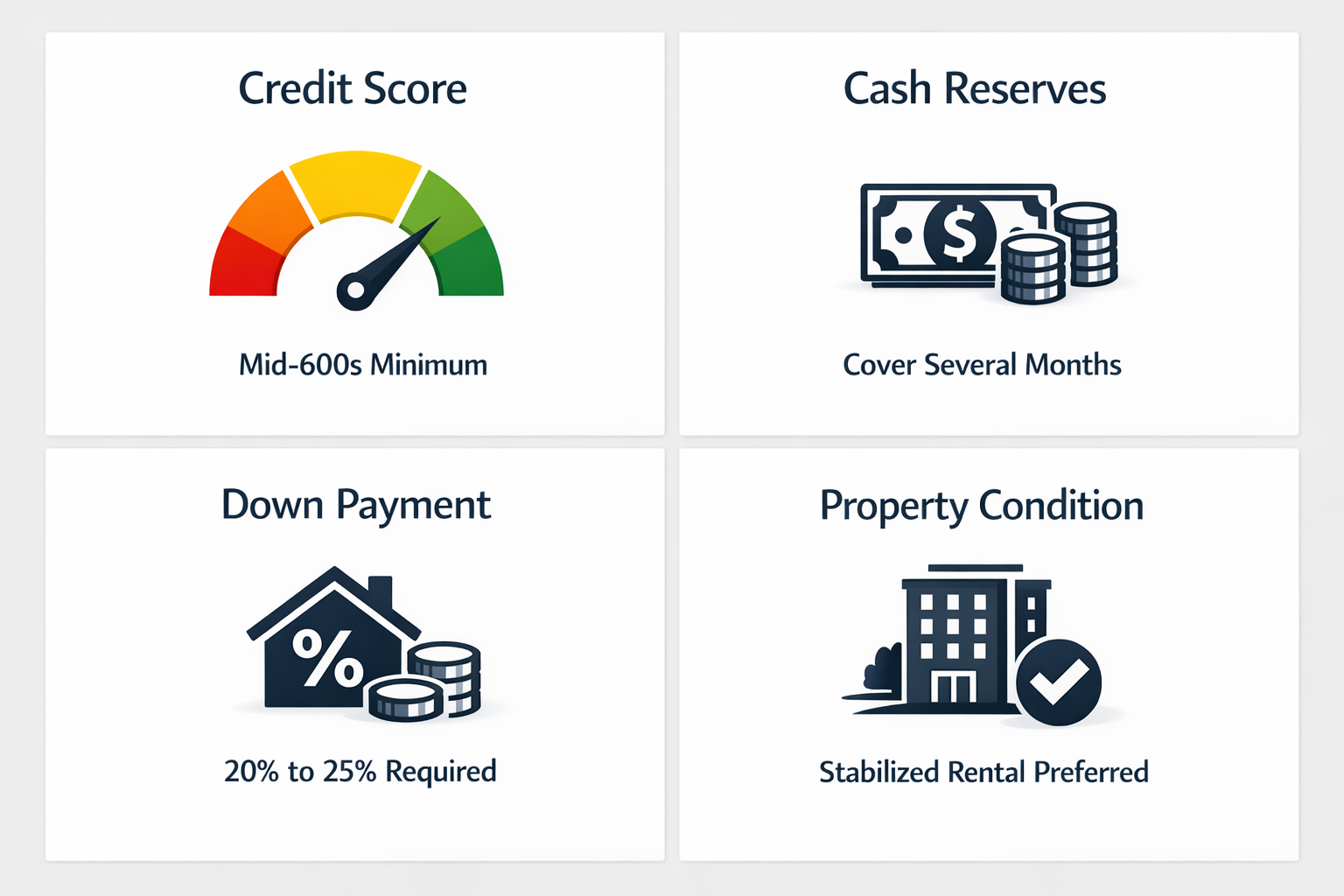

Essential Qualification Requirements Beyond Income

Essential qualification requirements beyond income focus on factors that demonstrate your capacity as an investor and the property's viability. While DSCR loans don't require income verification, lenders still need assurance that you can manage the investment successfully.

Credit requirements typically fall in the mid-600s or higher, though specific minimums vary by lender

Cash reserves covering several months of property expenses may be required to demonstrate financial stability

Down payment requirements often range from 20% to 25%, depending on the property type and your experience level

Property condition and type matter, as lenders prefer stabilized rental properties over major renovation projects

These requirements make sense when you consider the lender's perspective. Without personal income documentation, they're relying heavily on the property's performance and your ability to weather temporary vacancies or repairs. Strong credit history signals responsible financial management, while adequate reserves provide a buffer during lean months.

The down payment component serves multiple purposes. It reduces the lender's exposure, demonstrates your commitment to the investment, and provides equity cushion if property values fluctuate. For investors accustomed to conventional financing, these down payment levels might actually feel familiar. The real difference lies in what you don't need to provide: pay stubs, tax returns, employment verification letters, or detailed explanations of your income sources.

Property Cash Flow Calculations That Matter

Property cash flow calculations that matter determine whether your deal will clear the DSCR threshold. Understanding these numbers helps you evaluate potential acquisitions before you ever submit an application.

Monthly rental income must be documented through current leases, market rent analysis, or appraiser estimates

Total debt service includes principal, interest, taxes, insurance, and HOA fees if applicable

A DSCR of 1.0 means rental income exactly covers expenses, while ratios above 1.0 indicate positive cash flow

Most lenders prefer seeing DSCR ratios of 1.20 or higher for optimal approval odds

Let's break down a practical example. Say you're looking at a property with an estimated market rent of $2,400 per month. The proposed loan payment is $1,500, property taxes run $300 monthly, insurance costs $100, and there's a $50 HOA fee. Your total monthly debt service is $1,950. Divide the $2,400 rental income by $1,950 in expenses, and you get a DSCR of approximately 1.23. That's typically strong enough for approval.

This calculation framework transforms how you evaluate deals. Instead of asking whether a property fits your personal debt-to-income ratio, you're asking whether the property can carry itself. This shift encourages better investment discipline, as you're forced to focus on properties that genuinely make financial sense from a property cash flow metrics perspective.

Step-by-Step DSCR Loan Application Process

The step-by-step DSCR loan application process typically moves faster than conventional mortgages precisely because there's less documentation to gather and verify. Here's how investor approval generally unfolds when you're pursuing no tax return financing.

Submit your initial application with basic personal information, property details, and down payment verification rather than income documents

The lender orders an appraisal that includes a rental market analysis to establish the property's income potential

Underwriting reviews your credit, reserves, down payment source, and most importantly, the property's DSCR calculation

Final approval is issued based on the property's ability to service the debt, and you proceed to closing

The streamlined nature of this process can't be overstated. You're not waiting for employment verification callbacks or scrambling to explain income fluctuations across multiple tax years. The property does the talking. If the numbers work and your credit and reserves are solid, approval often comes quickly.

That said, you'll still need to be organized. Have your bank statements ready to document reserves and down payment funds. Be prepared to explain any credit issues clearly and honestly. Even though income isn't scrutinized, you're still demonstrating that you're a competent, responsible investor who takes the business seriously.

Strategic Advantages for Portfolio Growth

Strategic advantages for portfolio growth become apparent once you've closed your first DSCR loan. This financing model removes traditional scaling constraints that hold many investors back from building substantial rental portfolios.

You can acquire multiple properties without hitting personal debt-to-income limits that cap conventional mortgage approvals

Self-employed investors and business owners can expand their holdings without traditional income verification complications that typically delay or derail applications

Cash flow-focused underwriting encourages better deal selection, as you're naturally drawn to properties with strong rental fundamentals

Long-term financing options, potentially spanning 30 years, provide stability and predictable payments for strategic planning

Consider how this plays out in practice. An investor using conventional financing might hit their DTI ceiling after three or four financed properties, regardless of how well those properties perform. With DSCR financing, each property is evaluated independently based on its own cash flow. If you find ten properties with solid DSCR ratios, you could potentially finance all ten, limited only by your down payment capital and reserve requirements.

This model also rewards investors who do their homework. Those who become skilled at identifying undervalued properties in strong rental markets can move quickly without being held back by personal income documentation delays. The focus shifts to deal analysis and market knowledge, which are the skills that separate successful investors from the rest anyway.

Common Qualification Mistakes to Avoid

Common qualification mistakes can derail even promising applications. Knowing what to watch for helps you position your deal for success from the start.

Overestimating rental income or underestimating expenses leads to DSCR calculations that don't hold up under lender scrutiny

Insufficient cash reserves signal risk to lenders, even when the property's cash flow looks strong on paper

Ignoring credit issues or hoping they won't matter because income isn't verified can result in unexpected denials

Choosing properties that require significant renovation may not qualify, as DSCR loans typically work best for stabilized, rent-ready assets

The rental income estimation deserves special attention. Some investors get excited about a property's potential and project optimistic rents that don't align with current market data. Lenders rely on appraiser rent analyses, which are grounded in comparable properties. If you're banking on rents that exceed what similar properties command, your DSCR won't support approval no matter how convinced you are of the property's potential.

Similarly, the reserve requirement isn't arbitrary. Lenders have learned through experience that rental properties occasionally face vacancy periods, unexpected repairs, or tenant issues. Adequate reserves demonstrate that you can handle these situations without defaulting. Trying to minimize your reserve position to deploy more capital elsewhere might seem smart in the moment, but it can cost you the deal entirely.

Key Takeaway for Investor Success

The landscape of rental property financing has evolved dramatically to accommodate how real estate investors actually operate. If you've been frustrated by traditional mortgage requirements that don't recognize the value of your rental income or penalize you for legitimate tax strategies, DSCR loans represent a practical solution worth exploring.

Success with this approach comes down to shifting your mindset from personal income qualification to property performance qualification. Focus on acquiring properties with strong rental fundamentals, maintain solid credit and adequate reserves, and prepare for down payments in the 20% to 25% range. When you align your investment strategy with these principles, figuring out how to qualify for a rental property loan without income becomes not just possible, but straightforward.

The investors who thrive with DSCR financing are those who embrace data-driven deal analysis and maintain financial discipline. They understand that removing income verification requirements doesn't mean removing all standards. Rather, it means the standards now align with what actually matters for rental property investments: cash flow, market fundamentals, and the property's ability to service its own debt. That's a framework that rewards smart investing, and it's accessible to anyone willing to approach their portfolio strategically.

Qualifying for rental property financing without traditional income documentation represents a significant opportunity for investors at every experience level. Whether you're self-employed, strategically minimizing taxable income, or simply focused on building a portfolio that isn't constrained by personal earnings, DSCR loans provide a viable path forward.

The key lies in understanding that while personal income verification is removed from the equation, other qualification factors remain important. Your credit profile, available reserves, down payment capacity, and most critically, the property's rental income potential all play essential roles in the approval process. Lenders aren't eliminating standards; they're applying standards that make sense for investment properties.

As you evaluate your next acquisition, consider whether a DSCR approach might accelerate your portfolio growth. Run the numbers on potential properties using debt service coverage ratios rather than personal debt-to-income calculations. You might find that deals you previously thought were out of reach are suddenly accessible, simply because you're using a financing structure designed for investors rather than homebuyers.

The rental property market continues to offer compelling opportunities for those who approach it strategically. By leveraging financing products that recognize property cash flow as the true measure of an investment's viability, you can build the portfolio you've envisioned without being held back by conventional lending constraints. That's the advantage of knowing how to qualify for a rental property loan without income, and it's available to investors who are ready to focus on what really matters: finding properties that perform.