How to Analyze Rental Property Cash Flow Correctly

Real estate investors know that cash flow can make or break a deal. Whether you're evaluating your first rental property or adding another asset to your portfolio, understanding how to analyze rental property cash flow correctly separates profitable investments from financial headaches. This skill becomes even more critical when you're pursuing DSCR loans or other investor-focused financing, where lenders scrutinize your property's ability to generate consistent income.

Cash flow analysis isn't just about subtracting expenses from rent. It's a comprehensive evaluation that helps you understand whether a property will generate the returns you expect, sustain itself through market fluctuations, and qualify for the financing terms you need. With interest rates shifting and market conditions constantly evolving, investors who master accurate cash flow calculations position themselves to identify opportunities others might overlook.

In this guide, we'll walk through the core components of rental property cash flow analysis, from income calculation to expense ratios, so you can evaluate deals with confidence and build a portfolio that performs.

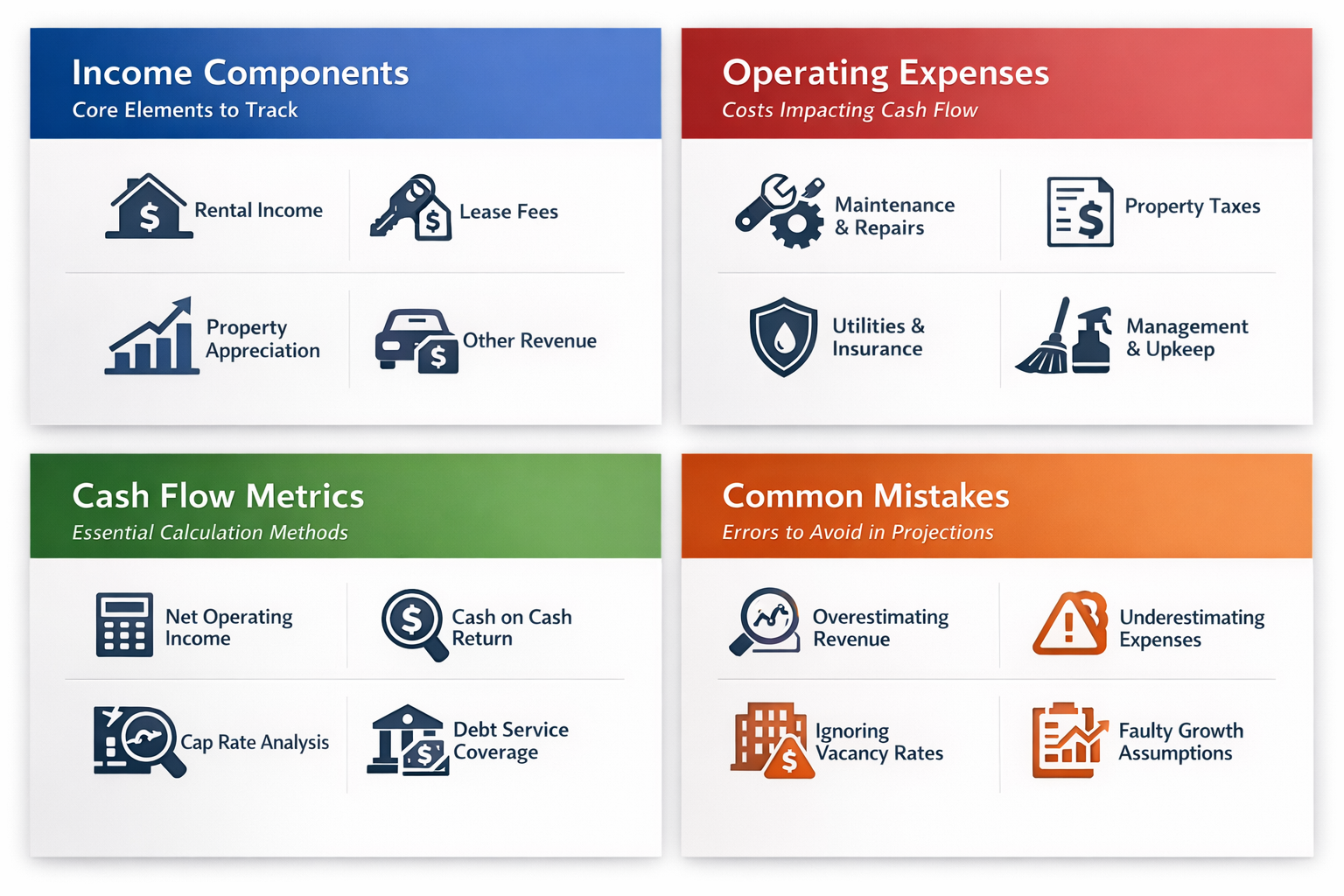

Core Income Components Every Investor Must Track

When analyzing rental property cash flow correctly, you need to start with a clear picture of your income potential. Core income components every investor must track form the foundation of your entire deal analysis. Without accurate income figures, every subsequent calculation will be flawed, potentially leading you to overestimate returns or miss warning signs.

Gross rental income: This represents the total rent you could collect if the property remained fully occupied year-round. It's your starting point, but never your endpoint. Calculate this by multiplying monthly rent by twelve, accounting for all units if you're analyzing a multi-family property.

Vacancy adjustments: Properties don't stay occupied 100% of the time. Vacancy rates account for turnover periods, seasonal fluctuations, and tenant transitions. Even well-managed properties typically experience some vacancy, so subtracting a realistic vacancy rate from gross income is essential for honest projections.

Other income streams: Many rental properties generate additional revenue beyond base rent. Parking fees, laundry facilities, storage rentals, or pet fees can contribute to your bottom line. Including these in your income calculation provides a more complete picture of the property's earning potential.

Rent escalation potential: Consider whether current rents align with market rates. Properties rented below market value might offer immediate upside, while those at premium rates may have less room for growth. This factor influences both current cash flow and long-term appreciation potential.

Accurate income calculation sets the stage for everything that follows. Overestimating rents or ignoring vacancy realities can make a marginal deal look attractive on paper, only to disappoint when actual performance falls short. DSCR lenders particularly scrutinize income projections, as they rely on rental income to cover debt service rather than personal income verification.

Operating Expenses That Impact Your Bottom Line

Operating expenses that impact your bottom line often get underestimated by newer investors, leading to cash flow surprises after closing. These ongoing costs eat into your rental income every month, and missing even one category can throw off your entire deal analysis. Experienced investors know that conservative expense estimates protect against unexpected shortfalls.

Property taxes and insurance: These fixed costs vary significantly by location and property type. Property taxes can increase over time, especially after a sale triggers reassessment. Insurance premiums fluctuate based on claims history, property condition, and market factors. Both represent non-negotiable expenses that must be paid regardless of occupancy.

Repairs and maintenance: Properties require ongoing upkeep. HVAC systems need servicing, roofs eventually need replacement, and appliances break down. Setting aside a percentage of gross income for repairs, typically between 5% and 15% depending on property age and condition, helps ensure you're prepared for inevitable maintenance issues.

Property management fees: Whether you self-manage or hire a property management company, there's a cost to operations. Professional management typically runs 8% to 12% of collected rent, while self-management still involves your time, marketing costs, and administrative expenses that should be factored into your analysis.

Utilities and services: Depending on your lease structure, you might cover water, sewer, trash, landscaping, or snow removal. In multi-family properties, common area utilities and services add to your expense burden. Understanding which utilities you'll cover versus those paid by tenants is critical for accurate projections.

Calculating expense ratios helps you benchmark a property against similar investments. Dividing total operating expenses by gross income gives you an operating expense ratio that typically ranges from 35% to 80% depending on property type and management intensity. Properties with ratios on the higher end require more scrutiny to ensure adequate cash flow remains after debt service.

Essential Cash Flow Calculation Methods

Essential cash flow calculation methods provide the framework for determining whether a property will generate positive returns. These formulas transform raw income and expense data into actionable metrics that inform your investment decisions and financing strategies.

Net Operating Income (NOI): This fundamental metric represents your property's profitability before financing costs. Calculate NOI by subtracting all operating expenses from your effective gross income (gross income minus vacancy). NOI gives you a clear picture of the property's operational performance independent of how you finance it.

Cash flow after debt service: This is the actual cash remaining after you've paid your mortgage. Subtract your monthly principal and interest payments from your monthly NOI to arrive at this figure. Positive cash flow means the property pays for itself plus extra, while negative cash flow requires you to contribute funds monthly.

Cash-on-cash return: This metric helps you evaluate how efficiently your invested capital performs. Divide your annual cash flow by your total cash investment (down payment plus closing costs and any immediate repairs) to calculate this percentage. It allows you to compare rental property returns against other investment opportunities.

Debt Service Coverage Ratio (DSCR): DSCR lenders use this calculation to determine loan eligibility. Divide your annual NOI by your annual debt service (all loan payments for the year). A DSCR of 1.0 means income exactly covers debt, while ratios above 1.25 typically qualify for better loan terms and demonstrate stronger cash flow cushion.

These calculation methods work together to provide multiple perspectives on the same investment. A property might show strong NOI but weak cash flow if debt service is too high, or it might have modest cash flow but excellent cash-on-cash returns if you minimized your initial investment. Understanding how these metrics interact helps you structure deals that align with your investment goals and financing requirements.

Step-by-Step Deal Analysis Workflow

A step-by-step deal analysis workflow brings structure to your evaluation process, ensuring you don't overlook critical factors when assessing rental property opportunities. Following a consistent approach helps you compare deals objectively and identify potential issues before committing capital.

Gather accurate property data: Start by collecting rent rolls, historical expenses, tax records, and insurance quotes. Request at least two years of financial statements from the seller. Verify current market rents by researching comparable properties in the area. The quality of your analysis depends entirely on the accuracy of your input data.

Calculate gross income with vacancy: Determine the property's gross potential income, then apply a realistic vacancy rate based on local market conditions and property type. In stable markets, this might be 5% to 8%, while transitioning areas or properties requiring repositioning may warrant higher vacancy assumptions. This gives you effective gross income for subsequent calculations.

Itemize all operating expenses: Build a comprehensive expense budget that includes property taxes, insurance, repairs, maintenance, management, utilities, and any other recurring costs. Compare your expense estimates against the property's historical performance and industry benchmarks. When in doubt, estimate conservatively to avoid cash flow surprises.

Project debt service and calculate metrics: Based on anticipated loan terms, including interest rate, loan-to-value ratio, and amortization period, calculate your expected monthly and annual debt service. Apply this to your NOI calculation to determine cash flow, then calculate your DSCR, cash-on-cash return, and cap rate to evaluate the deal from multiple angles.

Stress test your assumptions: Run scenarios where rents decline, expenses increase, or vacancy rises to understand your downside risk. Properties that maintain positive cash flow even under adverse conditions offer greater security and may qualify for more favorable financing terms from DSCR lenders who appreciate conservative underwriting.

This systematic workflow transforms deal evaluation from guesswork into a disciplined process. Investors who follow structured analysis methods typically avoid problematic acquisitions and identify opportunities with genuine upside potential. The time invested in thorough analysis pays dividends through better acquisition decisions and stronger portfolio performance over time.

Common Mistakes That Distort Cash Flow Projections

Common mistakes that distort cash flow projections can turn seemingly attractive deals into underperforming assets. Even experienced investors occasionally fall into these traps, particularly when market enthusiasm or competitive pressure clouds judgment. Recognizing these pitfalls helps you maintain realistic expectations and avoid costly errors.

Underestimating maintenance reserves: Many investors use low maintenance estimates to make deals look more attractive. Properties require ongoing upkeep, and deferred maintenance eventually catches up with you. Older properties or those with aging systems need higher reserve allocations. Failing to budget adequately forces you to cover shortfalls from personal funds or watch the property deteriorate.

Ignoring capital expenditures: Operating expenses cover routine maintenance, but capital expenditures address major replacements like roofs, HVAC systems, or parking lot resurfacing. These predictable but irregular costs can devastate cash flow if not anticipated. Setting aside funds for future capital needs, typically 5% to 10% of income for older properties, prevents these expenses from becoming emergencies.

Overstating rental income potential: Basing projections on optimistic rent assumptions without market validation leads to disappointment. Just because one comparable property commands premium rents doesn't mean yours will, especially if it lacks similar amenities or location advantages. Conservative rent estimates based on actual market data produce more reliable projections.

Forgetting about vacancy and turnover costs: Vacancy doesn't just mean lost rent. Turnover involves cleaning, repairs, marketing, and sometimes concessions to attract new tenants. These transition costs add up quickly and should be factored into your expense calculations. Properties in markets with high tenant turnover require larger reserves for these recurring costs.

Misclassifying financing assumptions: Using incorrect interest rates, overlooking prepayment penalties, or forgetting about mortgage insurance can significantly impact your debt service calculations. When analyzing deals for DSCR loan financing, ensure your debt service projections reflect actual available terms rather than idealized scenarios.

Avoiding these mistakes requires discipline and honest assessment. Markets reward optimism, but cash flow responds only to reality. Investors who maintain conservative projections and thorough due diligence build portfolios that perform consistently across various market conditions, positioning themselves for long-term success and easier access to investor financing.

Key Takeaway for Investor Success

Understanding how to analyze rental property cash flow correctly is not just a technical skill but a fundamental discipline that separates successful real estate investors from those who struggle. The difference between profitable portfolios and problematic ones often comes down to the accuracy and honesty of your initial analysis. When you master income calculation, expense estimation, and the various metrics that define property performance, you gain the confidence to evaluate deals quickly and make offers on properties with genuine potential.

This analytical rigor becomes especially valuable when seeking DSCR loans or other investor-focused financing. Lenders who specialize in rental property loans scrutinize the same cash flow metrics you should be evaluating, and properties with strong fundamentals naturally qualify for better terms. Your ability to demonstrate solid cash flow projections based on conservative assumptions can mean the difference between loan approval and rejection, or between favorable rates and expensive terms.

The most successful investors treat cash flow analysis as an ongoing practice rather than a one-time exercise. They continually refine their assumptions based on actual performance data, market changes, and lessons learned from previous acquisitions. This commitment to accurate analysis compounds over time, improving deal selection, portfolio performance, and ultimately, your returns as a real estate investor.

Accurate cash flow analysis forms the backbone of sound real estate investment strategy. By systematically evaluating income potential, operating expenses, and financing costs, you can identify properties that will genuinely contribute to your wealth-building goals rather than drain your resources. The formulas and workflows outlined here provide a framework you can apply consistently across every deal you evaluate.

Remember that conservative assumptions protect your downside while thorough analysis reveals upside opportunities others might miss. Properties that cash flow well under realistic scenarios tend to perform even better in practice, especially when you implement value-add strategies or benefit from market appreciation. These same properties also attract favorable financing terms from DSCR lenders and other investor-focused mortgage products designed for rental property investors.

As you apply these cash flow analysis techniques to your next investment opportunity, focus on building repeatable processes that become second nature. The time you invest in mastering these skills pays dividends through better acquisition decisions, stronger portfolio performance, and greater confidence in your ability to evaluate rental property deals correctly. With solid analytical foundations, you're positioned to build a rental property portfolio that generates the consistent returns you're seeking.