Understanding the DSCR loan DSCR ratio target is crucial for real estate investors seeking optimal financing terms in 2026. The debt service coverage ratio serves as the primary metric lenders use to evaluate rental property cash flow against mortgage obligations. With lenders typically requiring minimum DSCR thresholds of 1.00 or higher, investors must strategically position their properties to meet these standards while maximizing their financing potential.

The landscape of investor financing continues to evolve, with lenders offering increasingly favorable rates and terms for properties that exceed basic ratio requirements. Properties achieving ratios of 1.25 or higher often unlock premium lending conditions, including better interest rates and increased leverage options. This creates a clear incentive for investors to optimize their rental income and property selection strategies around these key benchmarks.

Essential Do's for DSCR Ratio Success

Following proven strategies for DSCR ratio optimization can significantly improve your loan approval chances and financing terms. These essential practices help investors maintain strong cash flow positions while meeting lender expectations.

Target a 1.25+ DSCR ratio to access premium lending rates and terms that can reduce overall financing costs

Ensure properties are rent-ready before applying, as lenders typically require immediate income-generating capability

Maintain detailed rental income documentation including lease agreements and market rent analysis to support your ratio calculations

Plan for 20-25% down payments as standard requirements that complement strong DSCR ratios for loan approval

Critical Don'ts That Hurt Your Approval

Avoiding common pitfalls in DSCR loan applications protects your approval chances and prevents costly delays in your investment timeline. These mistakes often create approval sensitivity that could derail your financing plans.

Don't apply with ratios below 1.00 as most lenders maintain this as a firm minimum threshold for any consideration

Don't overlook property condition requirements since non-rent-ready properties typically face immediate rejection or extensive delays

Don't underestimate operating expenses in your ratio calculations, as lenders scrutinize realistic cash flow projections

Don't rush the application without proper documentation of rental income potential and property financial performance

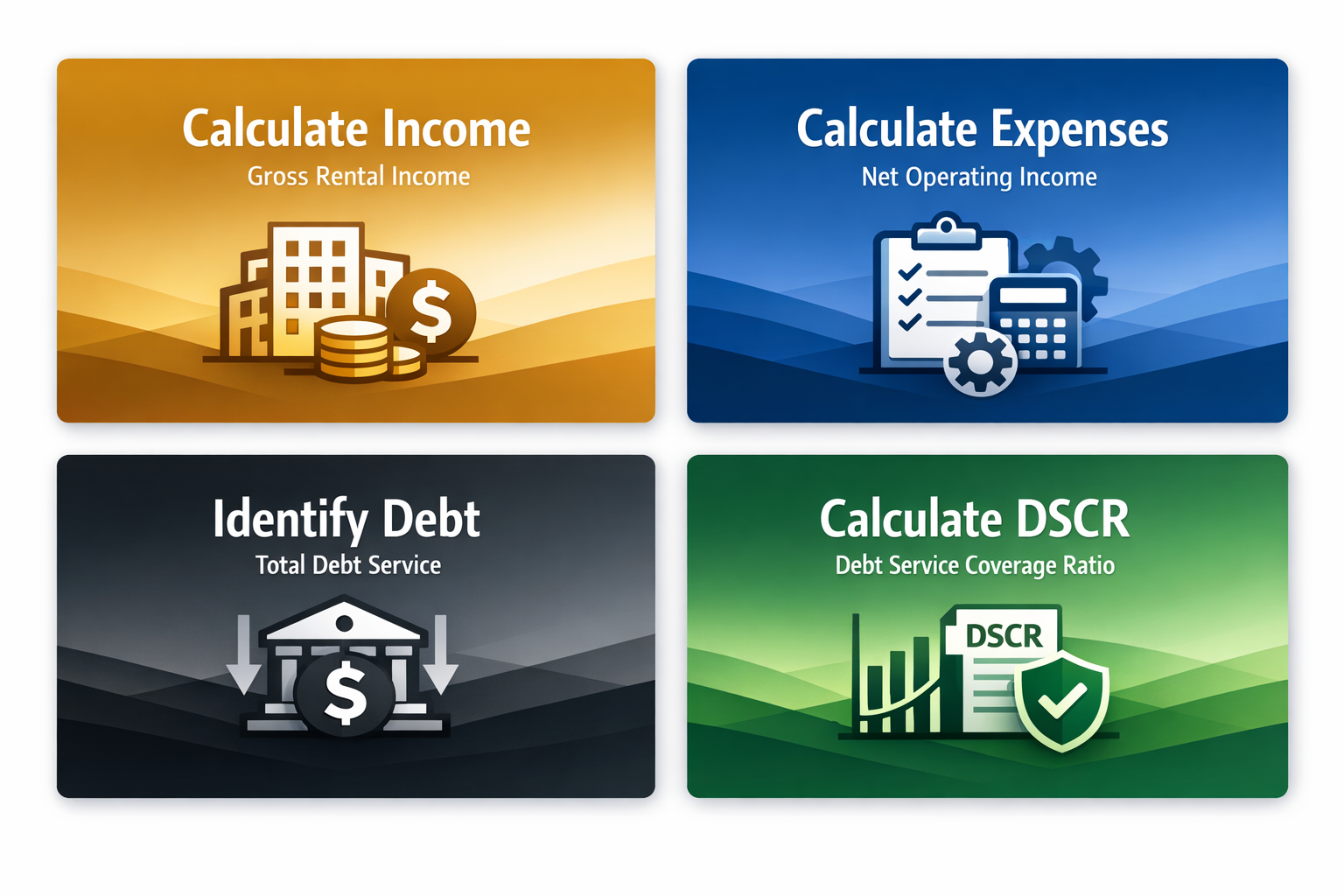

5 Steps to Calculate Your Target DSCR

Accurately calculating your DSCR loan DSCR ratio target ensures you understand exactly where your property stands before approaching lenders. This systematic approach helps identify potential issues early in the process.

Determine gross rental income using current lease agreements or professional market rent analysis for vacant properties

Calculate net operating income by subtracting property taxes, insurance, maintenance reserves, and management fees from gross rental income

Identify total debt service including principal, interest, taxes, and insurance payments for the proposed mortgage loan

Divide net operating income by total debt service to arrive at your property's debt service coverage ratio

Compare results against minimum DSCR thresholds to determine if your property meets lender requirements and qualifies for premium terms

4 Strategies for Improving Low Ratios

Properties that initially fall short of minimum DSCR thresholds may still become viable investments through strategic improvements. These approaches can help boost your cash flow buffer and meet lender expectations.

Increase rental income through property improvements that justify higher market rents and directly boost your numerator in DSCR calculations

Reduce operating expenses by negotiating better insurance rates, optimizing property management costs, or implementing energy-efficient upgrades

Consider larger down payments to reduce monthly debt service obligations and improve the overall ratio performance

Explore alternative loan structures such as bridge-to-DSCR refinancing that may offer more flexible initial terms while building toward target ratios

3 Key Factors Affecting Approval Sensitivity

Understanding what drives approval sensitivity in DSCR lending helps real estate investors anticipate potential challenges and prepare accordingly. These factors often determine whether borderline applications receive approval or face rejection.

Property location and market stability influence how lenders evaluate rental income sustainability and may affect minimum ratio requirements in specific markets

Borrower experience and portfolio size can impact lender confidence, with seasoned investors sometimes receiving more favorable consideration on marginal ratios

Economic conditions and lending environment may cause lenders to adjust their minimum DSCR thresholds or become more stringent in their cash flow analysis

Mastering DSCR loan DSCR ratio target requirements positions real estate investors for success in 2026's competitive lending environment. The clear benchmark of 1.00 minimum with premium benefits at 1.25 and above creates straightforward goals for property evaluation and financing strategy. Investors who consistently target these ratios while maintaining rent-ready properties and proper documentation will find themselves well-positioned to secure favorable financing terms.

The key to long-term success lies in viewing DSCR requirements not as obstacles but as guidelines for building a stronger, more profitable rental property portfolio. Properties that comfortably exceed minimum DSCR thresholds typically generate better cash flow, face fewer financing challenges, and provide more flexibility for future investment opportunities. By focusing on these fundamentals, investors can build sustainable wealth through strategic property acquisition and optimal financing structures.