LOAN PROGRAMS

APPLY NOW

Real estate investors face a crucial decision when selecting financing: DSCR loans or conventional mortgages. Understanding the top DSCR vs conventional differences can significantly impact your investment portfolio's growth and profitability. While conventional loans might offer lower interest rates, DSCR loans provide unique advantages for investors focused on rental property income. These financing options serve different investor needs, and the choice between them often determines how quickly you can expand your portfolio and maximize returns.

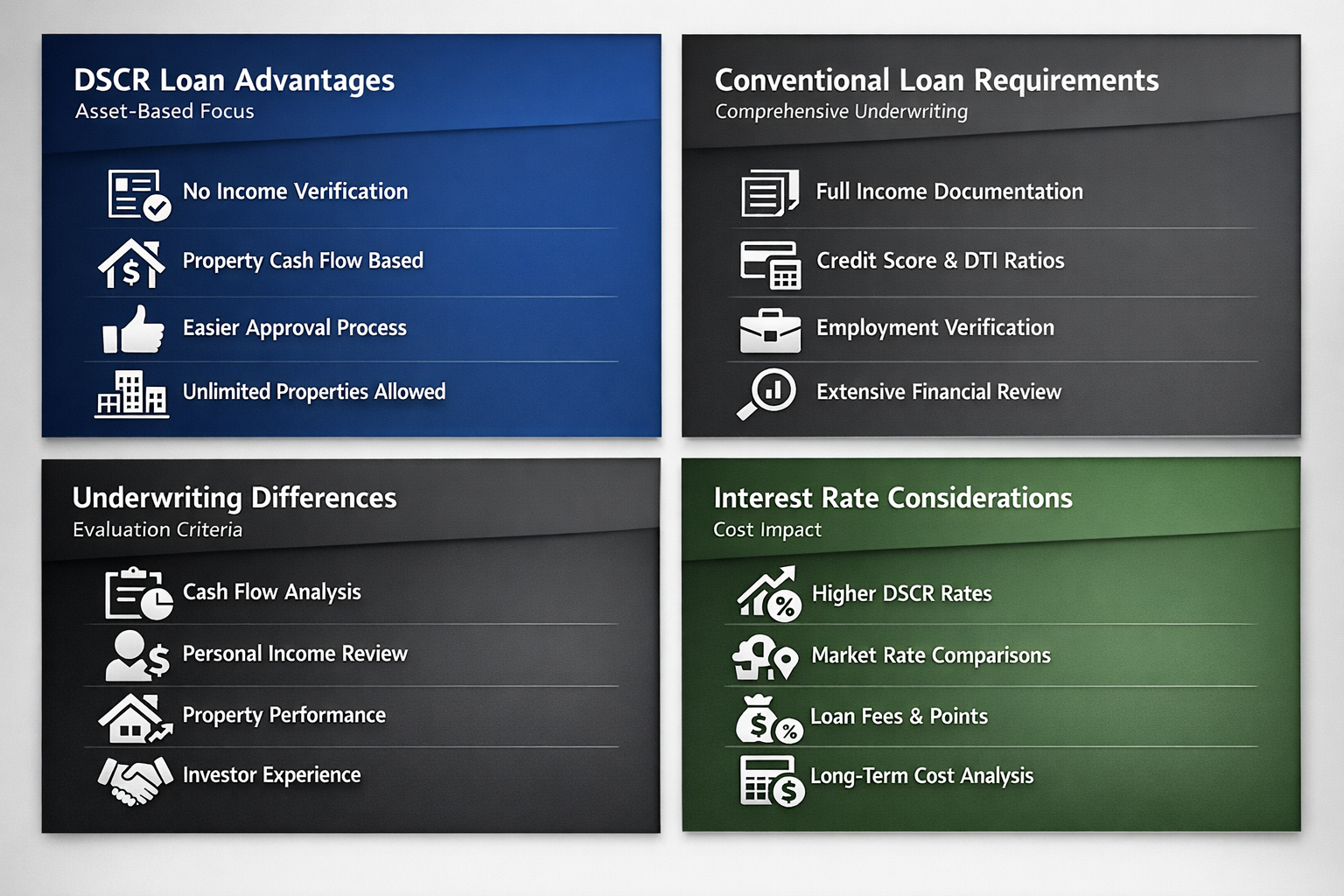

DSCR loan qualification advantages offer investors significant benefits when expanding their real estate portfolios. These asset-based loans focus primarily on property income rather than personal financial documentation.

Conventional loan qualification requirements typically involve comprehensive personal financial underwriting that many investors find restrictive for portfolio expansion.

Critical underwriting differences between DSCR and conventional loans shape how lenders evaluate your investment potential and determine loan approval.

Interest rate considerations for investors reveal important cost differences that could impact your investment strategy and long-term returns.

Portfolio expansion speed comparison shows how loan type selection directly affects your ability to acquire properties and grow your investment portfolio efficiently.

Long-term investment strategy impact varies significantly depending on whether you choose DSCR or conventional financing for your real estate portfolio.

Strategic decision framework for choosing between DSCR and conventional loans should align with your investment goals, timeline, and risk tolerance. Investors focused on rapid portfolio expansion might benefit from DSCR loans despite higher costs, while those prioritizing long-term cost efficiency may prefer conventional financing. The choice often depends on your personal financial situation, property acquisition strategy, and comfort level with different qualification processes. Consider how each loan type supports your specific investment objectives and cash flow requirements.

Understanding the top DSCR vs conventional differences empowers investors to make informed financing decisions that align with their portfolio goals. While conventional loans offer lower rates and greater refinancing flexibility, DSCR loans provide faster qualification and approval processes that could accelerate your investment timeline. The qualification comparison reveals that asset-based DSCR underwriting might suit investors who want to leverage property income rather than personal financial documentation. Ultimately, your choice between these financing options should reflect your investment strategy, risk tolerance, and growth objectives in today's competitive real estate market.