Refinancing rental properties has never been a walk in the park, but today's market presents a unique set of hurdles that can trip up even seasoned investors. Between surging insurance costs, tighter lending standards, and unpredictable interest rates, the path to securing favorable terms on an investment property refinance has become significantly more complex.

For real estate investors managing DSCR loans, bridge financing, or traditional rental property loans, understanding these top challenges in rental property refinancing today is crucial for maintaining cash flow and protecting your bottom line. The landscape has shifted dramatically since 2019, and what worked just a few years ago might not deliver the same results now.

This guide walks through the most pressing obstacles investors encounter when refinancing rental properties and offers practical insights to help you navigate these challenges effectively. Whether you're looking to tap equity through a cash-out refinance or simply secure better terms, knowing what lies ahead can make all the difference in your investment strategy.

Skyrocketing Insurance Costs Eating Into Your Margins

Skyrocketing insurance costs eating into your margins represent one of the most significant challenges investors face when refinancing rental properties. Property insurance premiums have surged dramatically, with data showing increases of over 75% between 2019 and 2024. This sharp rise directly impacts your operating expenses and can fundamentally alter the financial picture lenders see when evaluating your refinance application.

When you refinance, lenders recalculate your debt service coverage ratio and overall cash flow projections. Higher insurance costs mean reduced net operating income, which can affect your ability to qualify for the loan terms you're seeking. In some cases, these increased expenses might push your DSCR below lender thresholds, limiting your refinancing options or forcing you to accept less favorable terms.

Operating expense inflation: Insurance premiums now represent a much larger percentage of your total expenses, reducing the profitability metrics lenders use to evaluate your property's performance and refinance eligibility.

Cash flow compression: Even if you pass underwriting requirements, higher insurance costs mean less money in your pocket each month, potentially impacting your ability to cover multiple properties or pursue new investment opportunities.

Rent adjustment pressure: Many investors attempt to pass insurance cost increases to tenants through rent hikes, but market conditions may limit how much and how quickly you can adjust rents without affecting occupancy rates.

Reserve requirements: Lenders may require larger cash reserves when they see elevated insurance costs, tying up more of your capital and reducing liquidity for other investments or unexpected expenses.

These insurance cost challenges don't just affect your current refinance. They also influence your long-term investment strategy and require careful planning when calculating potential returns on rental properties. Accurately forecasting these expenses before you apply can help you set realistic expectations and avoid surprises during the underwriting process.

Higher Rates and Stricter Standards for Investment Properties

Higher rates and stricter standards for investment properties create a double challenge that separates rental property refinancing from primary residence loans. Investment property refinances typically come with interest rates that run higher than what owner-occupants receive, and qualifying criteria tend to be more demanding across the board.

Lenders view rental properties as higher-risk assets because borrowers may prioritize their primary residence payments during financial stress. This perceived risk translates directly into higher borrowing costs and more stringent approval requirements. For investors accustomed to the rates and terms available on personal homes, this difference can be a shock that significantly impacts deal economics.

Rate premiums: Investment property loans often carry interest rates that are 0.5% to 0.75% higher than comparable primary residence mortgages, increasing your monthly debt service and reducing cash-on-cash returns over the life of the loan.

Down payment and equity requirements: Cash-out refinances on rental properties may require you to maintain higher equity positions, limiting how much cash you can extract compared to owner-occupied refinancing scenarios.

Income documentation hurdles: Lenders typically scrutinize rental income more carefully, requiring lease agreements, rent rolls, and sometimes tax returns showing rental income history, which can complicate the application process and extend timelines.

Credit score thresholds: Minimum credit score requirements for investment property refinancing often sit higher than primary residence standards, and investors with multiple properties may face additional scrutiny on their overall debt load.

These stricter lender requirements mean you need to prepare more thoroughly before applying for a refinance on your rental property. Understanding exactly what documentation lenders will require and how they'll calculate your qualifying income can save time and prevent application denials that might affect your credit or delay your investment plans.

Appraisal Gaps and Valuation Uncertainty

Appraisal gaps and valuation uncertainty have become increasingly common problems that can derail an otherwise solid refinance plan. When you apply to refinance a rental property, the lender orders an appraisal to determine current market value. If that appraisal comes in lower than expected, it can reduce the loan amount you qualify for or eliminate refinancing opportunities altogether.

Market volatility and changing neighborhood dynamics make property valuations less predictable than in stable periods. Appraisers rely on recent comparable sales, and in markets with limited transaction volume or rapid changes, finding appropriate comps becomes challenging. For investors counting on a certain loan-to-value ratio to make the numbers work, an unexpected appraisal gap can throw a wrench in the entire strategy.

LTV ratio constraints: A lower-than-expected appraisal reduces your loan-to-value ratio, which might disqualify you from certain loan programs or reduce the amount of cash you can pull out in a refinance.

Refinance cost recovery: If the appraisal doesn't support your target loan amount, you may not recoup your closing costs within a reasonable timeframe, making the refinance financially unproductive.

Comparable property scarcity: In neighborhoods with few recent sales or unique property features, appraisers may struggle to find truly comparable properties, leading to conservative valuations that don't reflect your property's actual market potential.

Timing complications: Challenging an appraisal or ordering a second opinion adds weeks to your refinance timeline, potentially causing you to miss rate locks or other time-sensitive opportunities.

To minimize appraisal risk, savvy investors often research recent comparable sales in their area before applying and consider property improvements that might boost value. While you can't control the final appraisal figure, understanding local market conditions and providing the appraiser with relevant information about upgrades or neighborhood trends may help ensure a more accurate valuation.

Rental Income Calculation Complexities

Rental income calculation complexities present another layer of difficulty that many investors underestimate when pursuing a refinance. Unlike W-2 employment income that's straightforward to verify, rental income involves multiple variables and lender-specific calculation methods that can significantly affect your qualifying income and debt service coverage ratio.

Different lenders may apply different methods for calculating usable rental income, and these variations can mean the difference between approval and denial. Some lenders use the full lease amount, while others apply a 75% factor to account for vacancy and expenses. Understanding how your target lender calculates rental income before you apply helps you gauge whether your property will meet their DSCR requirements.

Vacancy adjustments: Many lenders automatically reduce your stated rental income by 25% or more to account for potential vacancies, even if your property has maintained full occupancy for years.

Lease documentation requirements: Current, signed lease agreements are typically mandatory, and month-to-month tenancies may receive less favorable treatment or lower income credit than long-term leases.

Historical income verification: Some lenders require tax returns showing rental income over one or two years, which can be problematic for recently acquired properties or those with past vacancies that don't reflect current performance.

Expense estimation variations: Lenders may use standardized expense ratios rather than your actual operating costs, which can work for or against you depending on how efficiently you manage the property.

For investors using DSCR loans specifically designed for rental properties, these income calculation methods might be more flexible than traditional mortgage products. However, even specialized lenders have their own formulas and requirements, making it essential to understand exactly how they'll treat your rental income before committing to a particular refinance path.

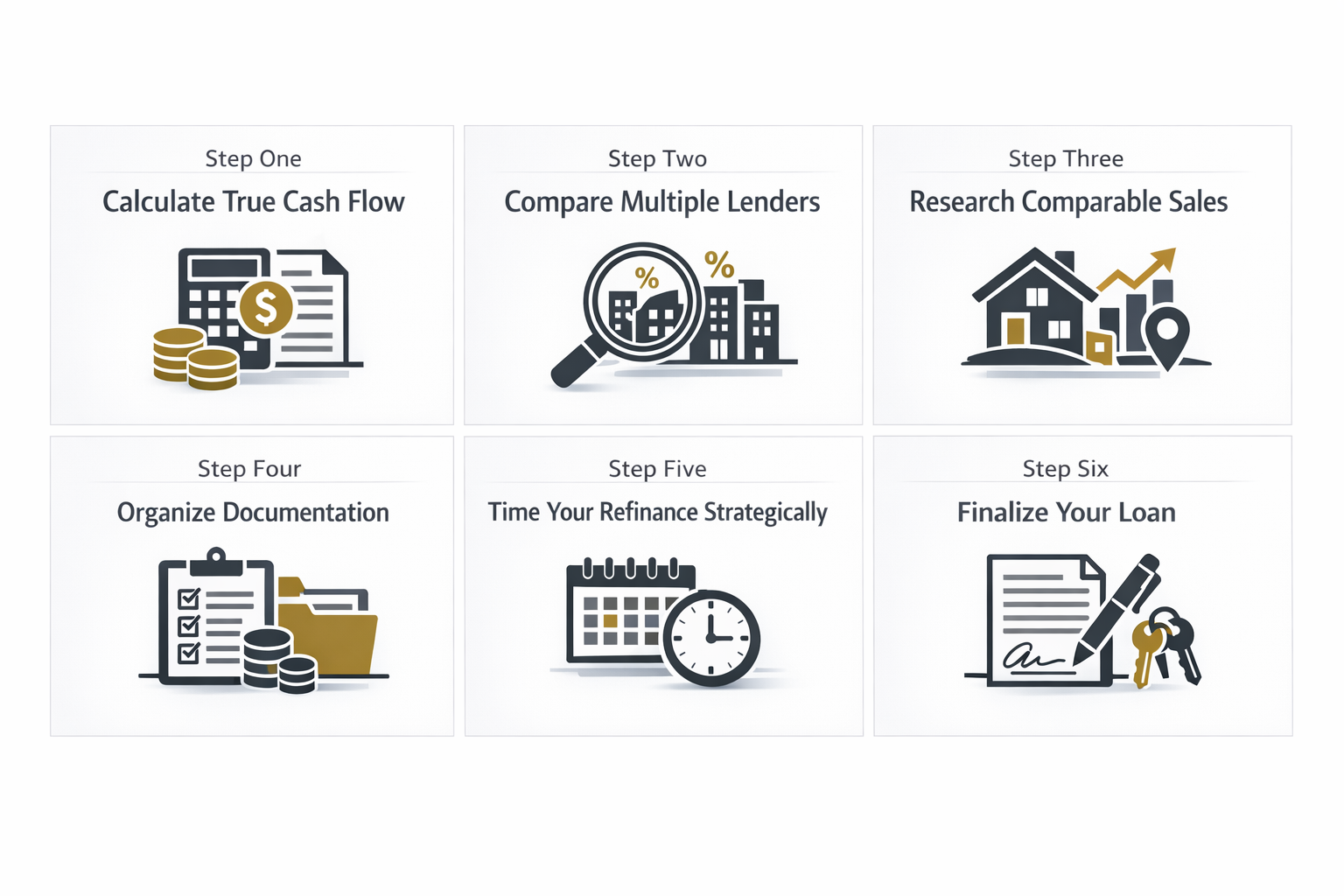

5 Steps to Overcome Refinancing Obstacles

Five steps to overcome refinancing obstacles can help you navigate the top challenges in rental property refinancing today and secure the best possible terms. While the hurdles are real, investors who approach refinancing strategically and prepare thoroughly tend to achieve better outcomes than those who rush into applications without proper planning.

Taking a methodical approach allows you to address potential problems before they derail your refinance and positions you to negotiate from a place of strength. These steps reflect insights drawn from successful investor strategies and lender requirements across the current market landscape.

Calculate your true cash flow with current expenses: Before approaching any lender, run your numbers using today's actual insurance costs, property taxes, and maintenance expenses rather than historical figures. This gives you a realistic picture of your DSCR and helps you determine whether refinancing makes financial sense at current rates. Include a buffer for potential cost increases so you're not caught off guard if expenses rise further before closing.

Compare multiple lenders and loan products: Investment property refinance terms can vary significantly between lenders, with some specializing in DSCR loans while others focus on traditional income verification. Request quotes from at least three to five lenders, paying attention not just to rates but also to how they calculate rental income, their LTV limits, and their underwriting flexibility. This comparison shopping can save thousands over the loan term.

Research comparable sales and property values: Conduct your own informal appraisal by reviewing recent sales of similar properties in your area before applying. This helps you set realistic expectations and may reveal opportunities to make strategic improvements that could boost your appraisal. If you discover your estimated value might fall short of what you need, you can adjust your loan amount expectations or delay refinancing until market conditions improve.

Organize documentation and strengthen your application: Gather all required documents including lease agreements, tax returns, insurance policies, and property expense records well before you apply. Having this information organized and readily available speeds up the process and demonstrates professionalism to lenders. Consider addressing any credit issues or paying down other debts to improve your overall financial profile and qualifying ratios.

Time your refinance strategically: Avoid refinancing during market extremes or when your property faces temporary challenges like tenant turnover or deferred maintenance. If interest rates are elevated but expected to moderate, consider whether waiting a few months might yield better terms. Conversely, if you're locked into a high rate and current market rates offer meaningful savings, acting quickly might make sense even if conditions aren't perfect.

These steps won't eliminate every challenge, but they can substantially improve your chances of a successful refinance at terms that support your investment goals. The key is treating the refinance process as seriously as you would treat acquiring a new property, with thorough due diligence and realistic expectations based on current market realities.

The top challenges in rental property refinancing today require investors to approach the process with eyes wide open and strategies firmly in place. Rising insurance costs, higher interest rates, stricter lending standards, appraisal uncertainties, and rental income calculation complexities all combine to create a more demanding environment than many investors faced in previous years.

Yet these obstacles don't make refinancing impossible or even inadvisable for many situations. Investors who understand these challenges, prepare thoroughly, and work with lenders experienced in investment property financing can still secure favorable terms that improve cash flow, extract equity for new opportunities, or simply reduce overall borrowing costs.

The key is recognizing that rental property refinancing isn't a set-it-and-forget-it transaction. It requires active management, careful number-crunching, and realistic expectations about what today's market can deliver. By accounting for increased operating expenses, comparing multiple lenders, understanding how your rental income will be calculated, and timing your application strategically, you position yourself to overcome these challenges and make refinancing work for your portfolio.

Remember that your depreciation schedule remains unaffected by refinancing, preserving important tax benefits regardless of your new loan terms. This stability in the tax treatment of your property can help offset some of the challenges posed by higher costs and stricter lending standards, maintaining the overall attractiveness of real estate investment even in a more complex refinancing environment.