Real estate investors face unique challenges when securing financing for rental properties. Traditional mortgage underwriting often focuses on personal income documentation, which may not reflect an investor's true capacity to service debt through property cash flow. Rental cash flow qualification offers a more logical approach, allowing investors to secure financing based on a property's actual income-generating potential rather than complex personal tax situations.

This shift toward cash flow-based underwriting has opened doors for investors who might struggle with conventional loan requirements. Understanding how lenders evaluate rental income and calculate debt service coverage ratios can significantly impact your ability to build a profitable portfolio.

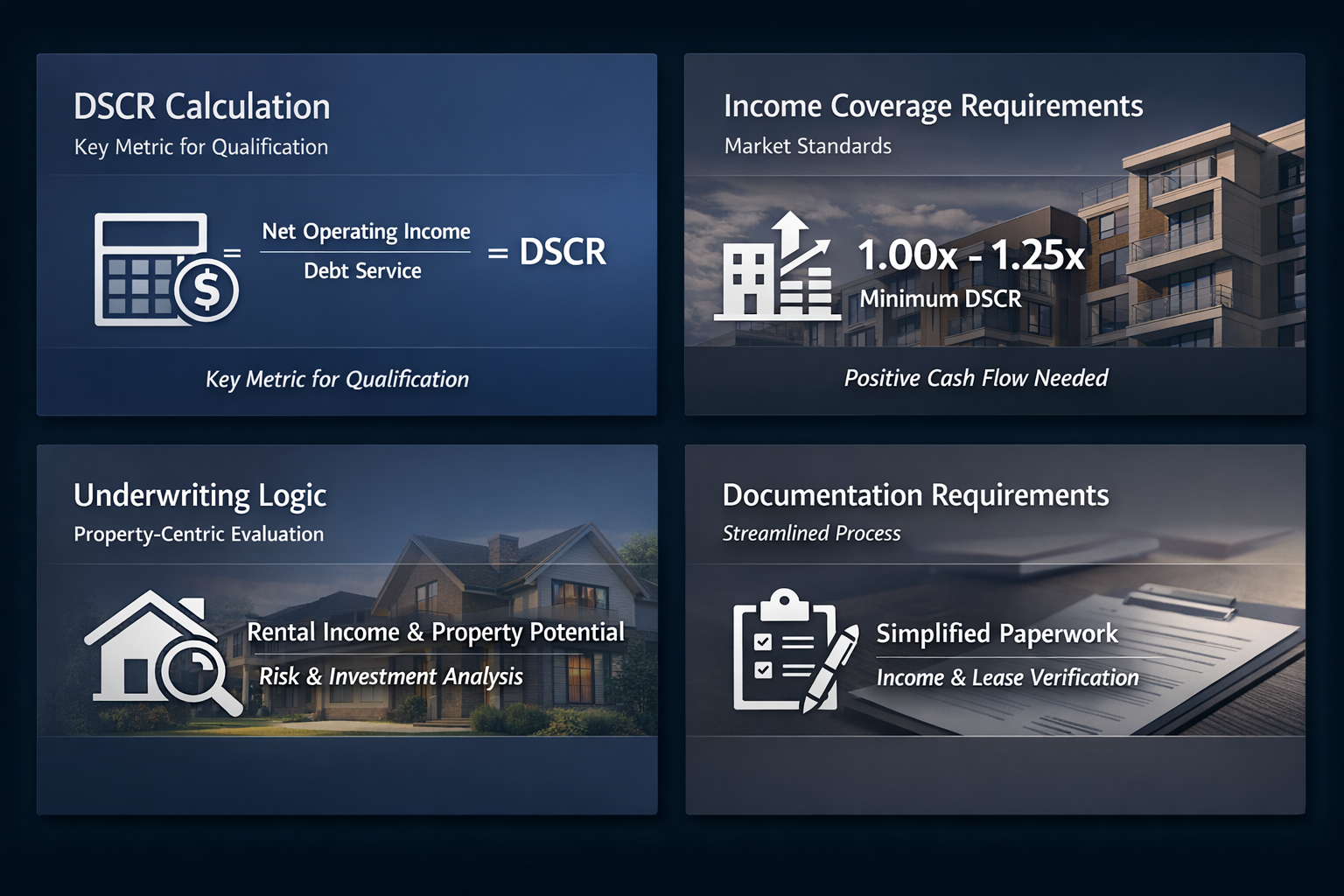

Understanding DSCR Calculation Fundamentals

DSCR calculation forms the backbone of rental cash flow qualification, providing lenders with a clear picture of a property's ability to cover its debt obligations. This calculation typically involves dividing the property's net operating income by its total debt service payments.

Lenders often count 75% of projected rental income toward qualifying income, creating a conservative buffer for vacancy and collection risks

A DSCR of 1.25 or higher may unlock the lowest rates and maximum leverage for qualified investors

Properties with strong cash flow can qualify investors even when personal income documentation proves challenging

The calculation bypasses traditional employment verification, focusing instead on property performance metrics

Income Coverage Requirements and Market Standards

Income coverage standards have evolved to reflect the realities of investment property ownership, with lenders developing sophisticated methods to evaluate rental income potential. These requirements balance risk management with investor accessibility.

Most lenders apply a 75% factor to projected rental income, accounting for potential vacancy periods and maintenance costs

Market rent analysis often involves comparing similar properties within a specific radius to establish realistic income projections

Seasoned rental properties with established income history may receive more favorable treatment than new acquisitions

Geographic market conditions can influence income coverage requirements, with some areas receiving preferential treatment based on rental market stability

Underwriting Logic Behind Cash Flow Qualification

Underwriting logic for rental cash flow qualification represents a fundamental shift from personal income verification to property-centric evaluation methods. This approach recognizes that investment properties should stand on their own financial merits.

Property cash flow analysis eliminates the need for complex personal tax return documentation that might not reflect true earning capacity

Lenders evaluate the property's historical performance and market comparables to establish realistic income expectations

The focus shifts from personal debt-to-income ratios to property-level debt service coverage capabilities

This logic allows investors with fluctuating personal income or complex tax situations to access financing based on property fundamentals

Documentation Requirements for Cash Flow Loans

Documentation requirements for rental cash flow qualification typically streamline the application process while maintaining appropriate risk assessment standards. This approach reduces paperwork burden while focusing on relevant financial metrics.

Property appraisals and rent rolls replace extensive personal income documentation in many cases

Market rent studies and comparable property analysis become primary evaluation tools for lenders

Basic personal financial statements may still be required, but the emphasis shifts to property performance

Existing lease agreements and rental history can strengthen qualification when available

Maximizing Your Qualification Success Rate

Maximizing your qualification success rate requires strategic preparation and understanding of how lenders evaluate rental cash flow scenarios. These steps can improve your chances of securing favorable terms.

Target properties with DSCR ratios of 1.25 or higher to access the most competitive rates and leverage options available in the market

Gather comprehensive market rent analysis and comparable property data to support realistic income projections during underwriting

Prepare detailed property operating expense estimates to demonstrate thorough due diligence and realistic cash flow expectations

Consider working with lenders who specialize in investor-focused products and understand the nuances of rental property financing

Maintain strong personal credit profiles even though personal income documentation may be less critical for qualification purposes

Rental cash flow qualification represents a significant advancement in investment property financing, aligning loan approval criteria with the economic reality of rental property ownership. By understanding DSCR calculation methods, income coverage standards, and underwriting logic, investors can position themselves for success in today's competitive market.

The shift toward cash flow-based qualification opens opportunities for investors who might otherwise struggle with traditional mortgage requirements. As market conditions continue evolving, these financing tools become increasingly valuable for building and expanding rental property portfolios.

Success in rental cash flow qualification depends on thorough preparation, realistic income projections, and working with lenders who understand investor needs. By focusing on property fundamentals rather than personal income complexity, investors can access the capital needed to grow their real estate investments effectively.