Smart real estate investors know that successful property flipping starts with the right financing approach. Fix and flip financing strategies can make the difference between a profitable deal and a costly mistake. With interest rates for short-term bridge and fix-and-flip loans ranging from 9-12% plus origination points, understanding how to structure your financing becomes critical for maintaining healthy profit margins.

The landscape for fix and flip investments continues evolving, with regional market trends playing an increasingly important role in financing decisions. Whether you're targeting distressed properties in high-growth markets or managing multiple renovation projects, your financing strategy must align with both current market conditions and your investment timeline.

Essential Fix and Flip Loan Structure Components

Understanding fix and flip loan structure fundamentals helps investors negotiate better terms and manage their financing costs effectively. The right loan structure can significantly impact your project's profitability and cash flow during renovation phases.

Interest-only payment terms: These arrangements allow investors to minimize monthly payments during renovation periods, preserving cash flow for project expenses and maximizing overall returns on investment.

Combined purchase and renovation funding: Loans that cover both property acquisition and renovation costs in a single financing package streamline the funding process and reduce administrative complexity for investors.

No prepayment penalty options: Seeking loans without prepayment penalties provides flexibility to exit investments early when market conditions favor quick sales, helping manage overall financing costs.

Short-term commitment periods: Typical loan terms align with renovation timelines, usually ranging from six months to two years, matching the expected project completion and sale schedule.

Renovation Budget Planning for Maximum Returns

Effective renovation budget planning requires balancing improvement costs against potential market value increases. Successful investors typically focus their renovation dollars on improvements that generate the highest return on investment while staying within their financing limits.

Kitchen and bathroom priorities: These high-impact areas often provide the strongest returns on renovation investment, making them logical focuses for budget allocation in most flip projects.

Contingency fund allocation: Setting aside 15-20% of the renovation budget for unexpected issues helps prevent financing shortfalls that could derail project timelines or profitability.

Market-appropriate upgrades: Renovation scope should match the target market's expectations and price point, avoiding over-improvements that won't generate proportional value increases.

Timeline-driven scheduling: Coordinating renovation phases with loan terms helps minimize interest costs and ensures projects stay within their financing windows.

Managing Short Term Loan Risks Effectively

Short term loan risks require careful management since fix and flip projects operate under tight timelines with significant financial leverage. Understanding these risks helps investors develop mitigation strategies that protect their investment capital.

Market timing considerations: Regional market conditions can significantly impact sale timelines and exit strategies, requiring investors to monitor local trends that might affect their ability to sell within loan terms.

Construction delay buffers: Building extra time into project schedules helps account for permit delays, contractor issues, or material shortages that could extend renovation timelines beyond loan maturity dates.

Exit strategy flexibility: Having backup plans such as rental conversion or alternative sale methods provides options when primary exit strategies face unexpected challenges or market shifts.

Qualification requirement awareness: Understanding that lenders may have strict qualification standards and potentially slower approval processes helps investors plan their financing timeline appropriately.

Current Market Rate Environment Impact

The current rate environment significantly affects fix and flip financing strategies, with investors needing to adapt their approaches based on prevailing interest rates and lending conditions. Monitoring these trends helps inform timing decisions and deal evaluation criteria.

Interest rate monitoring: With rates typically ranging from 9-12% plus origination points, investors must factor these costs into their flip profit calculations to ensure deals remain profitable.

Regional variation awareness: Different markets may offer varying financing terms and conditions, making location-specific research important for optimizing financing strategies across multiple markets.

Regulatory impact assessment: Understanding how regulatory changes affect loan qualification requirements helps investors prepare documentation and structure deals to meet evolving lender standards.

Competition factor consideration: Market conditions in key investment areas may influence both property acquisition costs and financing availability, affecting overall investment strategy decisions.

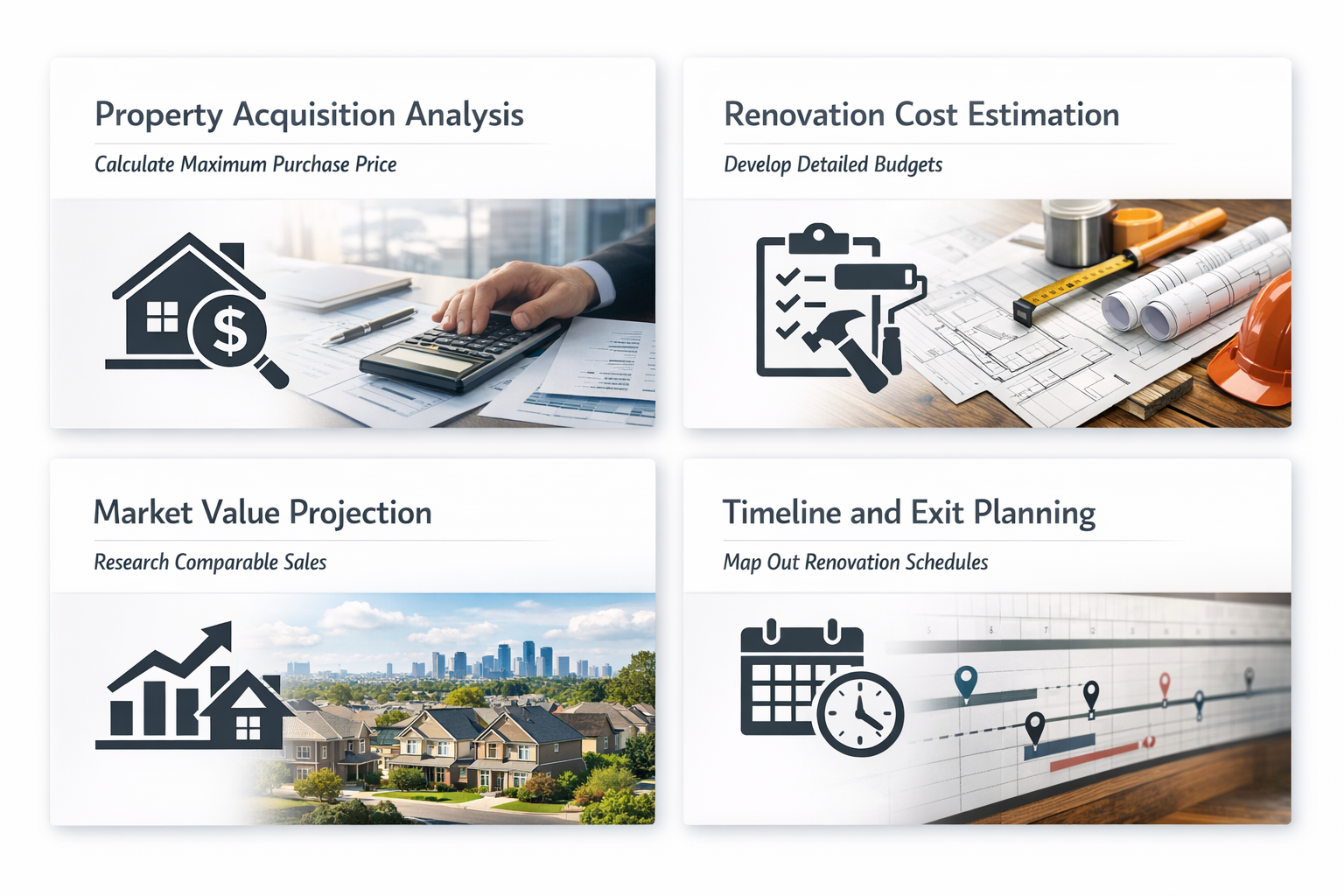

Step-by-Step Deal Evaluation Process

A systematic approach to evaluating potential fix and flip deals helps investors identify profitable opportunities while avoiding costly mistakes. This process should integrate financing considerations from the initial property assessment through final sale projections.

Property acquisition analysis: Calculate the maximum purchase price that allows for renovation costs, financing expenses, and target profit margins while remaining competitive in your target market.

Renovation cost estimation: Develop detailed budgets that include materials, labor, permits, and contingencies, ensuring these costs align with your available financing limits and timeline requirements.

Market value projection: Research comparable sales and current market trends to establish realistic after-repair value estimates that support your financing strategy and profit goals.

Timeline and exit planning: Map out renovation schedules and sale timelines that work within your loan terms, including buffers for potential delays or market fluctuations.

Final profitability verification: Confirm that projected returns justify the risks and financing costs involved, accounting for all expenses including interest, origination fees, and holding costs.

Optimizing Cash Flow During Projects

Effective cash flow management during fix and flip projects helps investors maintain financial flexibility while maximizing returns. The right financing structure combined with careful expense management can significantly improve project profitability.

Interest-only payment utilization: Taking advantage of interest-only loan terms during renovation phases preserves cash for project expenses and unexpected costs while maintaining financial flexibility throughout the project timeline.

Draw schedule coordination: Aligning renovation funding draws with project milestones ensures adequate cash availability for each phase while minimizing interest costs on unused funds.

Expense timing management: Strategically timing major expenses and contractor payments helps maintain steady cash flow and prevents funding shortfalls during critical project phases.

Reserve fund maintenance: Keeping adequate reserves available helps handle unexpected costs or delays without requiring additional financing that could impact overall project profitability.

Successful fix and flip financing strategies require careful attention to loan structure, renovation budgeting, and risk management. By focusing on interest-only terms, maintaining adequate reserves, and understanding current market conditions, investors can position themselves for profitable outcomes even in challenging rate environments.

The key to long-term success lies in adapting your financing approach to match regional market trends while maintaining flexibility through favorable loan terms. As the fix and flip market continues evolving, investors who master these financing fundamentals will be best positioned to capitalize on emerging opportunities and navigate potential challenges effectively.