How to Qualify DSCR with LLC: A Complete Guide for Real Estate Investors

Understanding how to qualify DSCR with LLC ownership can significantly impact your real estate investment strategy. DSCR loans offer investors a unique opportunity to secure financing based on property income rather than personal income verification. When structured through an LLC, these loans may provide additional benefits for portfolio growth and asset protection. However, navigating the qualification requirements for LLC-owned DSCR loans requires careful attention to specific criteria that lenders typically evaluate during the approval process.

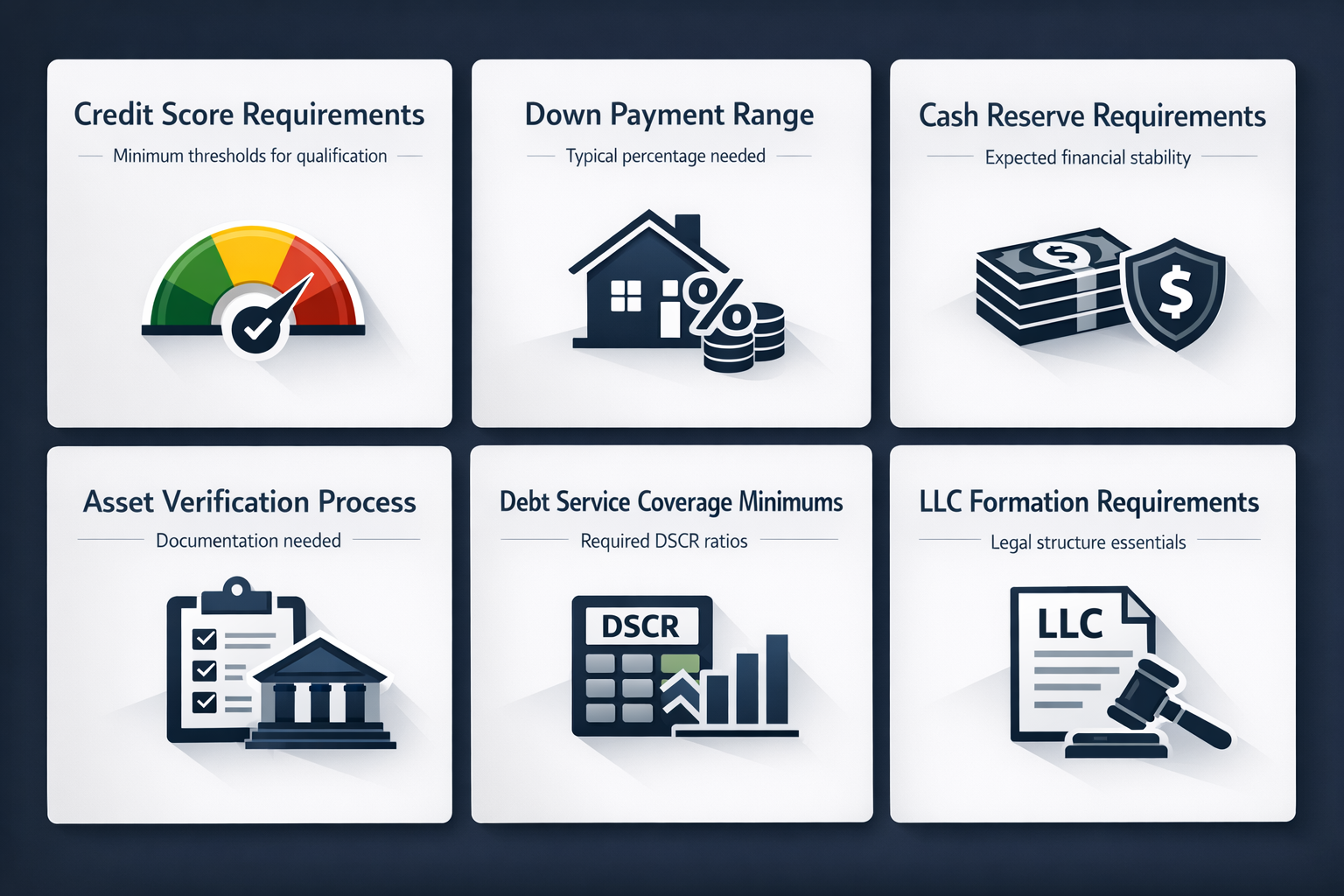

Essential Credit Score Requirements for LLC DSCR Loans

Credit score requirements for LLC DSCR loans can vary significantly among lenders, but understanding the typical thresholds helps investors prepare their applications effectively. The credit evaluation process for entity ownership often focuses on the personal credit profiles of LLC members or guarantors.

Minimum Credit Score Thresholds: Most lenders require credit scores of 660 or higher for basic qualification, though some may accept scores as low as 550 depending on other compensating factors

Optimal Credit Positioning: Credit scores between 680-700 typically qualify for the best loan terms and interest rates, making this range highly desirable for investors

Credit Score Impact on Terms: Higher credit scores often result in lower down payment requirements and more favorable interest rates, directly affecting your investment returns

Multiple Member Considerations: When your LLC has multiple members, lenders might evaluate the credit profiles of all guarantors or focus on the member with the strongest credit history

Down Payment and Financial Requirements

Financial requirements for LLC DSCR loans typically differ from traditional mortgage products, with specific emphasis on cash reserves and down payment amounts. These requirements help lenders assess the LLC's financial stability and the investment's viability.

Standard Down Payment Range: Most lenders require down payments between 20% to 25% of the property's purchase price for LLC-owned DSCR loans

Cash Reserve Requirements: Lenders often expect LLCs to maintain cash reserves equivalent to several months of property expenses, though specific amounts may vary by lender

Asset Verification Process: The LLC's bank statements and financial records become crucial documentation during the underwriting process

Debt Service Coverage Minimums: Properties must typically demonstrate a DSCR of 0.75 or higher, though some lenders prefer ratios between 1.0 to 1.25 for optimal approval odds

Entity Ownership Rules and LLC Structure

Proper LLC structure plays a vital role in DSCR loan qualification, as lenders evaluate both the entity's legal formation and operational framework. Understanding these entity ownership rules helps investors position their applications for success.

LLC Formation Requirements: The LLC must be properly formed and registered in its state of operation, with all required documentation filed and current

Ownership Transparency: Lenders typically require clear identification of all LLC members and their ownership percentages, ensuring transparency in the ownership structure

Management Structure Clarity: Whether your LLC is member-managed or manager-managed can impact the loan application process and required documentation

Business Purpose Alignment: The LLC's stated business purpose should align with real estate investment activities to support the loan application's credibility

Operating Agreement Requirements and Documentation

Operating agreement requirements form a critical component of the DSCR loan qualification process for LLCs. Lenders use these documents to understand the entity's governance structure and decision-making authority for the proposed investment.

Comprehensive Operating Agreement: A well-drafted operating agreement that clearly outlines member roles, responsibilities, and decision-making authority strengthens your loan application

Property Acquisition Authority: The operating agreement should explicitly grant authority to acquire real estate investments, demonstrating the LLC's legitimate business purpose

Financial Management Provisions: Clear provisions regarding financial management, debt obligations, and property management responsibilities help lenders assess operational competency

Member Liability and Guarantees: The agreement should address personal guarantees and member liability issues, which directly impact the lender's risk assessment

5 Steps to Successfully Qualify Your LLC for DSCR Loans

Successfully qualifying DSCR loans requires a systematic approach that addresses all key lender requirements. Following these essential steps can streamline your application process and improve approval odds.

Establish Strong Credit Foundations: Ensure all LLC members or guarantors maintain credit scores above 660, with optimal positioning in the 680-700 range for best terms

Structure Your LLC Properly: Complete proper entity formation with comprehensive operating agreements that clearly define investment authority and member responsibilities

Prepare Financial Documentation: Gather LLC bank statements, tax returns, and financial records that demonstrate the entity's financial stability and cash reserves

Analyze Property Cash Flow: Calculate the property's debt service coverage ratio to ensure it meets or exceeds the lender's minimum requirements of 0.75 or higher

Secure Adequate Down Payment: Prepare the required 20-25% down payment and additional cash reserves to meet lender expectations for LLC-owned investments

Learning how to qualify DSCR with LLC ownership opens significant opportunities for real estate investors seeking flexible financing solutions. The combination of entity ownership benefits and income-based qualification criteria creates a powerful tool for portfolio expansion. By focusing on credit positioning, proper LLC structure, and comprehensive documentation, investors can position themselves for successful DSCR loan approval. Remember that each lender may have specific requirements, so working with experienced mortgage professionals who understand investor needs can help navigate the application process effectively and secure optimal loan terms for your investment strategy.