Owning a vacant rental property presents unique financing challenges that can stump even experienced investors. When you're looking to finance a rental property with no tenants, traditional lenders often hesitate because there's no immediate cash flow to support the loan. Yet plenty of investors find themselves in this exact situation, whether they've just completed a renovation, inherited a property, or are repositioning an asset for a different tenant profile.

The good news? Several financing pathways exist specifically for vacant properties. Understanding how lenders evaluate empty rentals, what documentation strengthens your application, and which loan products accommodate non-occupied investment properties can make the difference between a rejected application and a funded deal. This guide walks through practical strategies that help investors navigate the approval process and secure the capital needed to move forward with confidence.

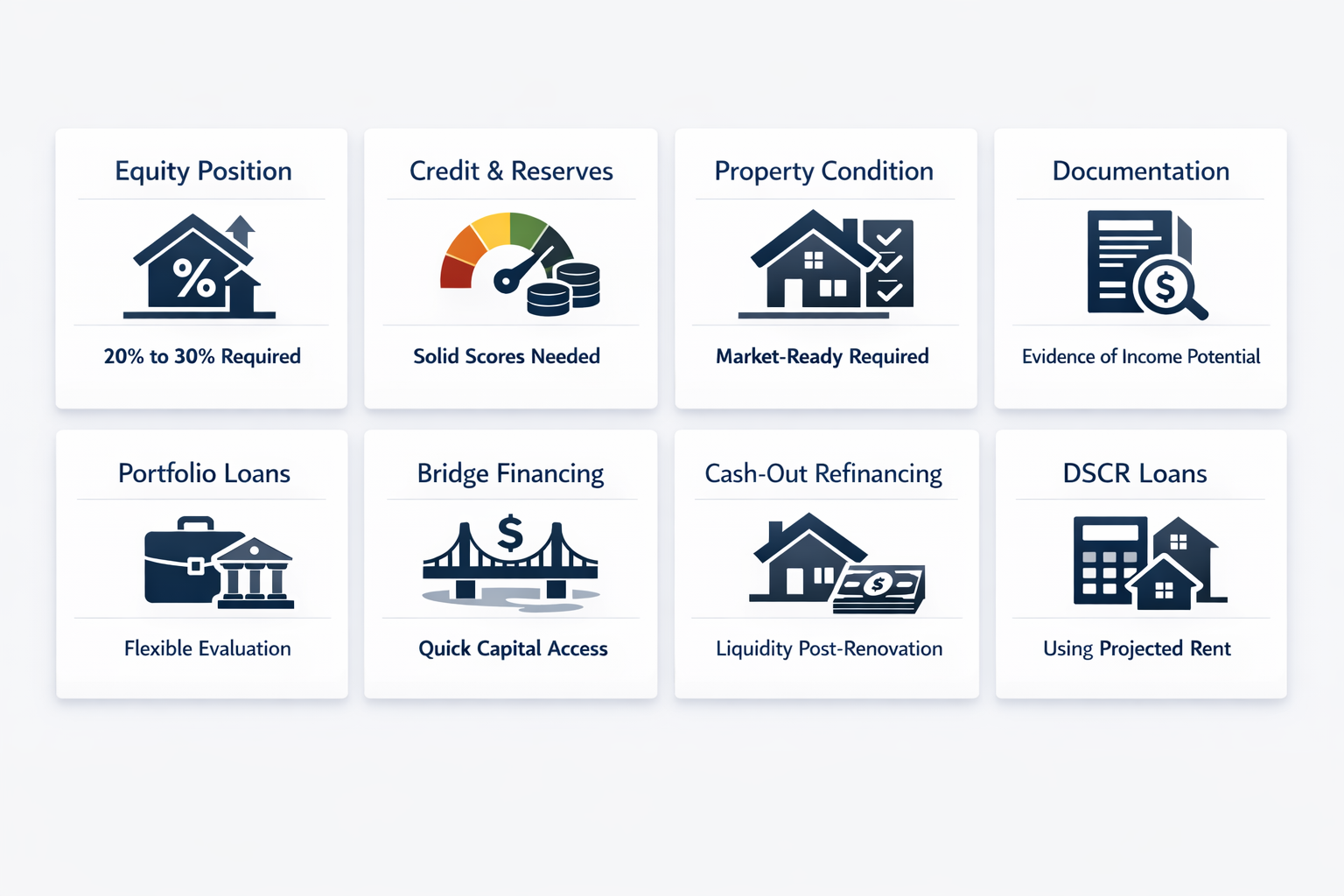

Understanding Vacant Property Loan Requirements

Understanding vacant property loan requirements is the foundation for any investor tackling how to finance a rental property with no tenants. Lenders typically assess vacant properties differently than occupied ones because the absence of current rental income creates perceived risk. However, many financial institutions offer products designed specifically for this scenario.

Equity position matters: Most lenders require substantial equity in the property, often 20% to 30% or more, to offset the risk associated with no immediate cash flow. A stronger equity cushion demonstrates your financial commitment and provides the lender with additional security.

Credit and reserves: Expect lenders to scrutinize your credit profile and liquid reserves more closely when the property sits vacant. Maintaining solid credit scores and demonstrating several months of reserves can improve your approval odds significantly.

Property condition and marketability: Lenders may require appraisals that confirm the property is rent-ready or nearly so. Properties in poor condition might face additional hurdles, while well-maintained, market-ready units tend to receive more favorable consideration.

Documentation of projected income: Even without current tenants, you'll typically need to provide evidence of the property's income potential through comparable rent data, broker opinions of value, or formal rent studies that justify the projected cash flow.

Loan Products That Work for Empty Rentals

Loan products that work for empty rentals come in several forms, each with distinct advantages depending on your investment strategy and financial profile. Exploring diverse financing options can open doors that conventional mortgages might close.

Portfolio loans: These loans are held by the lender rather than sold on the secondary market, giving the institution more flexibility to evaluate vacant properties based on the full investment picture rather than rigid underwriting formulas.

Bridge financing: Short-term bridge loans can provide quick capital for investors planning to lease the property soon or complete minor improvements before securing longer-term financing. These products often accommodate vacant properties more readily than permanent loans.

Cash-out refinancing post-renovation: If you've recently renovated a property and it now sits vacant, cash-out refinancing may provide liquidity while you search for qualified tenants. This approach can work well when you've added significant value and meet the lender's equity and credit criteria.

DSCR loans with projected rent: Some lenders offer DSCR loans that calculate debt service coverage using projected rent rather than actual income, making them particularly useful for vacant rental properties with strong market fundamentals.

Leveraging Projected Rent in Your Application

Leveraging projected rent in your application is a critical tactic when current tenants aren't in place to demonstrate cash flow. Lenders who accept projected rent typically require robust documentation to justify the income assumptions underlying your loan request.

Obtain a professional rent analysis: A formal rent study or broker price opinion that details comparable properties, market vacancy rates, and realistic rent expectations adds credibility to your projections and helps underwriters feel confident in the deal.

Highlight market demand indicators: Data showing low vacancy rates, growing renter populations, or new employers entering the area can strengthen the case that your property will lease quickly at the projected rate.

Present a conservative estimate: Submitting rent projections slightly below market peaks demonstrates prudence and reduces the perceived risk, potentially improving approval odds. Lenders appreciate borrowers who build in a margin of safety rather than chasing optimistic scenarios.

Pre-Approval Strategies to Strengthen Your Position

Pre-approval strategies to strengthen your position can significantly boost your chances of securing financing for a vacant rental property. Taking proactive steps before formally applying often reveals potential obstacles early and gives you time to address them.

Gather comprehensive financial documentation upfront: Assemble tax returns, bank statements, proof of reserves, and details on all existing properties before contacting lenders. Complete documentation signals professionalism and speeds up the underwriting process considerably.

Engage multiple lenders to compare terms: Different institutions have varying appetites for vacant property loans. Shopping around helps you identify which lenders offer the most favorable terms and which underwriting criteria align best with your situation.

Request pre-qualification or pre-approval letters: Obtaining written confirmation of your borrowing capacity demonstrates to sellers and partners that you're a serious buyer. It also clarifies exactly what loan amount and terms you can realistically expect, allowing you to structure deals accordingly.

Address credit or reserve gaps proactively: If preliminary conversations reveal weaknesses in your application, take time to pay down debts, build reserves, or improve credit scores before submitting a formal loan request. Small improvements can shift the approval decision in your favor.

Preparing Your Property for Lender Evaluation

Preparing your property for lender evaluation involves more than just aesthetic improvements. Lenders assess vacant rentals on both their current condition and their income-generating potential, so presenting the asset in the best possible light can influence underwriting outcomes.

Complete necessary repairs and maintenance: Fix deferred maintenance issues, address code violations, and ensure all systems function properly. Properties in move-in condition typically appraise higher and face fewer financing obstacles than those needing significant work.

Stage or clean the property thoroughly: Even if you're not selling, a clean, well-presented property photographs better for appraisals and signals to lenders that the asset is market-ready. First impressions matter, even in lending.

Document recent capital improvements: Provide receipts, permits, and before-and-after photos of renovations or upgrades. This evidence can support higher appraised values and justify projected rent figures, both of which strengthen your loan application.

Prepare a property fact sheet: Create a one-page summary highlighting square footage, bed and bath count, recent improvements, neighborhood amenities, and comparable rent data. This organized presentation helps lenders quickly understand the asset's value proposition.

Navigating Common Approval Challenges

Navigating common approval challenges requires anticipating lender concerns and preparing clear, data-driven responses. Vacant properties inherently raise questions, but thoughtful preparation can turn potential red flags into manageable discussions.

Addressing the income gap directly: Be upfront about the vacancy and explain your plan for leasing the property. Whether you're working with a property manager, listing on multiple platforms, or offering move-in incentives, a concrete action plan reassures lenders that the vacancy is temporary.

Demonstrating broader portfolio performance: If you own other rental properties, strong performance across your portfolio can offset concerns about a single vacant unit. Providing rent rolls, occupancy history, and cash flow summaries for your other assets shows you're a capable operator.

Offering additional collateral or a larger down payment: When lenders remain hesitant, increasing your equity stake or offering cross-collateralization with another property might tip the decision in your favor. These concessions reduce lender risk and demonstrate your confidence in the investment.

Working with experienced loan officers: Lenders familiar with investor loans and vacant property scenarios can navigate internal underwriting more effectively than generalists. Partnering with the right loan officer often makes the difference between approval and denial.

Key Takeaways for Vacant Property Financing

Key takeaways for vacant property financing center on preparation, documentation, and strategic lender selection. Investors who understand that financing a rental property with no tenants requires a different approach than traditional occupied property loans are better positioned to succeed. Building a strong equity position, maintaining solid credit and reserves, and presenting well-documented projected rent calculations form the foundation of most successful applications. Exploring diverse loan products, from portfolio loans to DSCR options based on projected income, expands your financing options and increases approval odds. Finally, taking a proactive stance by engaging multiple lenders, preparing comprehensive documentation, and addressing potential concerns upfront can transform a challenging financing scenario into a straightforward process. With the right strategy and preparation, securing capital for vacant rental properties becomes not only possible but also a repeatable part of your investment toolkit.

Financing a rental property with no tenants might feel daunting at first glance, but it's a challenge many investors successfully navigate with the right knowledge and approach. By understanding lender requirements, exploring loan products suited to vacant properties, and presenting strong documentation around projected rent and property condition, you position yourself for approval even when cash flow isn't immediately evident. Taking time to prepare your application thoroughly, engage experienced lenders, and address potential concerns proactively can make all the difference.

Remember, every investor faces vacancies at some point, whether planned or unexpected. Developing the skills to secure financing during these periods adds a powerful tool to your investment strategy and keeps your portfolio moving forward. As you apply these strategies, you'll likely find that lenders are more flexible than you initially expected, especially when you demonstrate professionalism, preparation, and a clear plan for generating income. Keep refining your approach with each deal, and vacant property financing will become just another manageable aspect of building long-term real estate wealth.