How to Calculate Return on Rental Property Investment

Understanding how to calculate return on rental property investment is one of the most critical skills for any real estate investor. Whether you're evaluating your first rental acquisition or refinancing an existing portfolio, knowing the numbers behind your investment separates profitable deals from costly mistakes. Many investors skip this step or rely on guesswork, only to discover later that their property doesn't generate the cash flow they expected.

The good news? Calculating return on rental property investment doesn't require an advanced degree in finance. With a few straightforward formulas and an understanding of key metrics like cap rate and cash on cash return, you can quickly assess whether a deal makes sense. These calculations also play a vital role when applying for DSCR loans or other investor-focused financing, as lenders want to see that your property can support its debt service.

In this guide, we'll walk through the essential ROI formulas every investor should know, break down the components that affect your returns, and show you how to use these metrics to make smarter financing and acquisition decisions. Let's dive into the numbers that matter most.

Core Components of Rental Property ROI

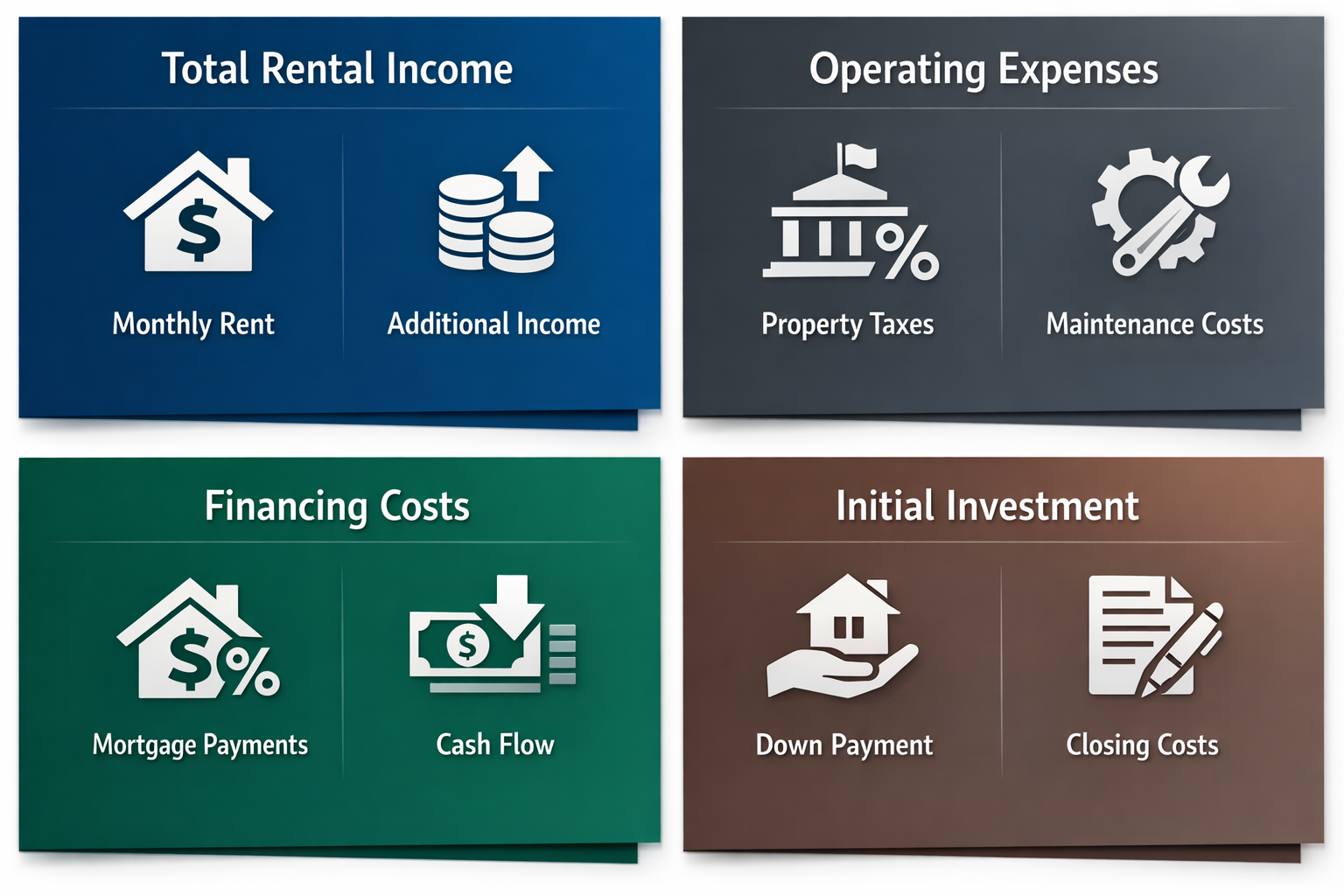

Before you can calculate return on rental property investment accurately, you need to understand what goes into the calculation. Core components of rental property ROI include both the income your property generates and the expenses it incurs. Missing even one category can skew your projections and lead to poor investment decisions.

Total rental income: This includes monthly rent collected from tenants, as well as any additional income from parking fees, laundry facilities, or storage rentals. Researching local rent prices helps you estimate realistic income figures before acquisition.

Operating expenses: These typically cover property taxes, insurance, maintenance, repairs, property management fees, utilities paid by the landlord, and vacancy allowances. Estimating monthly expenses accurately is crucial for understanding net operating income.

Financing costs: Mortgage payments, including principal and interest, affect your cash flow but may not always be included in certain ROI formulas like cap rate. However, they're essential when calculating cash on cash return.

Initial investment: This encompasses the down payment, closing costs, renovation expenses for fix and flip projects, and any immediate repairs needed to make the property rent-ready.

Getting these numbers right from the start helps investors qualify for DSCR loans, where lenders assess whether the property's income can cover its debt obligations. Accurate projections also ensure you're comparing apples to apples when evaluating multiple deals in different markets.

Essential ROI Formulas for Real Estate Investors

Essential ROI formulas for real estate investors provide a framework for comparing different properties and strategies. While there are several ways to measure returns, three formulas stand out as particularly useful for rental property analysis. Each offers a slightly different perspective on profitability.

Basic ROI formula: The simplest approach involves subtracting total expenses from total income, then dividing by your initial investment. This straightforward calculation gives you a percentage return that's easy to understand and communicate.

Capitalization rate (cap rate): This metric divides net operating income by the property's purchase price or current market value. Cap rate is useful because it excludes financing costs, allowing you to evaluate the property's performance independent of how you paid for it.

Cash on cash return: This formula divides annual pre-tax cash flow by the total cash invested, including your down payment and closing costs. It's particularly relevant for leveraged investments and helps you understand the return on your actual out-of-pocket money.

Internal rate of return (IRR): More advanced investors may use IRR to account for the time value of money and project returns over a multi-year hold period. Financial calculators can compute IRR based on projected cash flows and eventual sale proceeds.

Each of these ROI formulas serves a different purpose in your analysis. Basic ROI offers simplicity, cap rate enables market comparison, and cash on cash return reveals leverage efficiency. Using multiple formulas together gives you a more complete picture of your investment's potential.

Step-by-Step: Calculating Cap Rate

Step-by-step: calculating cap rate begins with determining your property's net operating income. The cap rate is one of the most widely used metrics in commercial and residential investment analysis because it provides a snapshot of a property's profitability before financing enters the equation.

Calculate gross rental income: Start by multiplying your monthly rent by 12 to get annual income. Include any additional revenue streams like parking or laundry, but be conservative in your estimates to account for occasional vacancies.

Subtract operating expenses: Deduct all annual expenses including property taxes, insurance, maintenance, management fees, and a vacancy allowance. This gives you your net operating income, the numerator in the cap rate formula.

Divide by property value: Take your net operating income and divide it by either the purchase price or current market value of the property. Multiply by 100 to express the result as a percentage.

Compare to market averages: Once you have your cap rate, compare it to similar properties in the same market. Higher cap rates typically indicate higher returns but may also signal higher risk or less desirable locations.

Cap rate is especially useful when evaluating DSCR loan opportunities because it helps lenders and investors quickly assess whether a property generates sufficient income relative to its value. A property with a strong cap rate in a stable market often qualifies more easily for investor financing and may support better loan terms.

How to Calculate Cash on Cash Return

Determine your total cash invested: Add up your down payment, closing costs, loan fees, and any immediate renovation or repair expenses. This total represents the actual cash you've put into the deal, not including the borrowed portion of your financing.

Calculate annual pre-tax cash flow: Start with your gross rental income, subtract all operating expenses including property management and maintenance, then subtract your annual mortgage payments (both principal and interest). The result is your pre-tax cash flow for the year.

Divide cash flow by cash invested: Take your annual pre-tax cash flow and divide it by your total cash invested. Multiply by 100 to express this as a percentage. This percentage is your cash on cash return.

Adjust for multiple scenarios: Run the calculation under different assumptions, such as higher vacancy rates or unexpected repair costs. This sensitivity analysis helps you understand the range of possible outcomes and prepare for less favorable conditions.

How to calculate cash on cash return becomes particularly important when you're using leverage to acquire rental properties. Since DSCR loans and other investor financing options allow you to put down less cash upfront, your cash on cash return can be significantly higher than your overall ROI. This metric helps you evaluate whether using financing makes sense compared to an all-cash purchase.

Common Mistakes When Calculating Returns

Underestimating expenses: Many investors fail to account for the full range of operating costs, particularly maintenance, capital expenditures, and vacancy periods. Property management fees, even if you self-manage initially, should be included because your time has value and you may eventually hire a manager.

Using unrealistic rent projections: Overestimating what tenants will pay is a fast track to disappointing returns. Research comparable rentals in the neighborhood and adjust for the condition and features of your specific property. Market rent data should come from recent listings and actual lease agreements, not aspirational pricing.

Ignoring capital expenditures: Roofs, HVAC systems, and appliances don't last forever. Setting aside a percentage of rental income for future capital improvements ensures you're not caught off guard when major systems need replacement. This reserve should be factored into your expense calculations.

Forgetting to update calculations: Markets change, and so do expenses. Revisiting your ROI calculations annually helps you spot trends, identify underperforming properties, and make informed decisions about refinancing, selling, or making improvements that could boost returns.

Avoiding these common mistakes when calculating returns can mean the difference between a profitable investment and one that drains your resources. Lenders evaluating DSCR loan applications pay close attention to whether your projections are realistic, so building conservative, well-supported estimates strengthens your financing position and protects your investment capital.

Using ROI Metrics for Financing Decisions

Using ROI metrics for financing decisions helps investors determine which loan products best suit their investment strategy. When you understand your projected returns, you can evaluate whether the cost of financing makes sense and which loan structures offer the most favorable terms relative to your goals.

For instance, DSCR loans focus primarily on the property's debt service coverage ratio, which compares the property's net operating income to its debt obligations. If your cap rate calculation shows strong income relative to property value, and your cash on cash return projections demonstrate solid cash flow even after mortgage payments, you're likely to qualify for favorable DSCR loan terms. Lenders want to see that the rental income can comfortably cover the monthly debt service with room to spare.

Similarly, when considering fix and flip financing, your ROI calculations help you determine how much you can afford to borrow while still hitting your profit targets. If your after-repair value projections and cost estimates yield a strong return, you can confidently pursue short-term bridge loans knowing the numbers support your exit strategy. On the other hand, if the margins are tight, you might opt for more conservative financing or look for a different property altogether.

Ultimately, these metrics give you the confidence to negotiate with lenders, choose between competing loan offers, and structure deals that align with your investment objectives. They transform financing from a guessing game into a strategic tool for building wealth through real estate.

Knowing how to calculate return on rental property investment empowers you to evaluate deals with clarity and confidence. The ROI formulas we've covered, including cap rate, cash on cash return, and basic return calculations, provide the foundation for sound investment decisions. Each metric offers a different lens through which to view profitability, and using them together gives you a comprehensive understanding of any property's potential.

These calculations aren't just academic exercises. They directly influence your ability to secure financing, negotiate better terms, and build a portfolio that generates consistent cash flow. Whether you're applying for a DSCR loan, evaluating a fix and flip opportunity, or deciding between multiple rental properties, the numbers guide your strategy and protect your capital.

Take the time to research local rent prices, estimate expenses conservatively, and run multiple scenarios before committing to any investment. The few hours you spend crunching numbers upfront can save you from years of underperformance or financial stress. With these tools in hand, you're ready to approach rental property investing with the professionalism and precision that separate successful investors from the rest.