How Lenders Calculate DSCR: A Real Estate Investor's Guide to Better Financing

Understanding how lenders calculate DSCR can be the difference between securing favorable financing terms and facing rejection on your next rental property acquisition. The debt service coverage ratio serves as a crucial metric that determines whether your investment property generates sufficient income to cover its debt obligations.

For real estate investors, mastering this calculation isn't just about meeting minimum requirements. It's about positioning your portfolio to access better rates, higher loan amounts, and more flexible terms. When lenders evaluate DSCR loans, they're essentially measuring the financial health of your property rather than relying solely on your personal income history.

This comprehensive guide breaks down the exact methodology lenders use, giving you the insights needed to optimize your properties for maximum financing potential.

Common Questions About DSCR Calculations

Many investors have similar questions when first encountering DSCR calculations in their financing journey.

Q:What's the basic formula lenders use to calculate DSCR?

Lenders typically calculate DSCR by dividing the property's net operating income by its total debt service payments. This ratio shows whether the rental income can adequately cover mortgage payments, with most lenders requiring a minimum ratio between 1.0 and 1.25.

Q:Do lenders use actual rent or market rent for calculations?

Most lenders may use either existing lease agreements or third-party rent assessments, depending on their specific underwriting guidelines. Some might apply a vacancy factor to account for potential income gaps between tenants.

Q:How do lenders factor in property expenses?

Lenders often calculate expenses using standardized percentages or actual operating statements. Common expense assumptions might include property taxes, insurance, maintenance reserves, and management fees, though the exact methodology can vary between institutions.

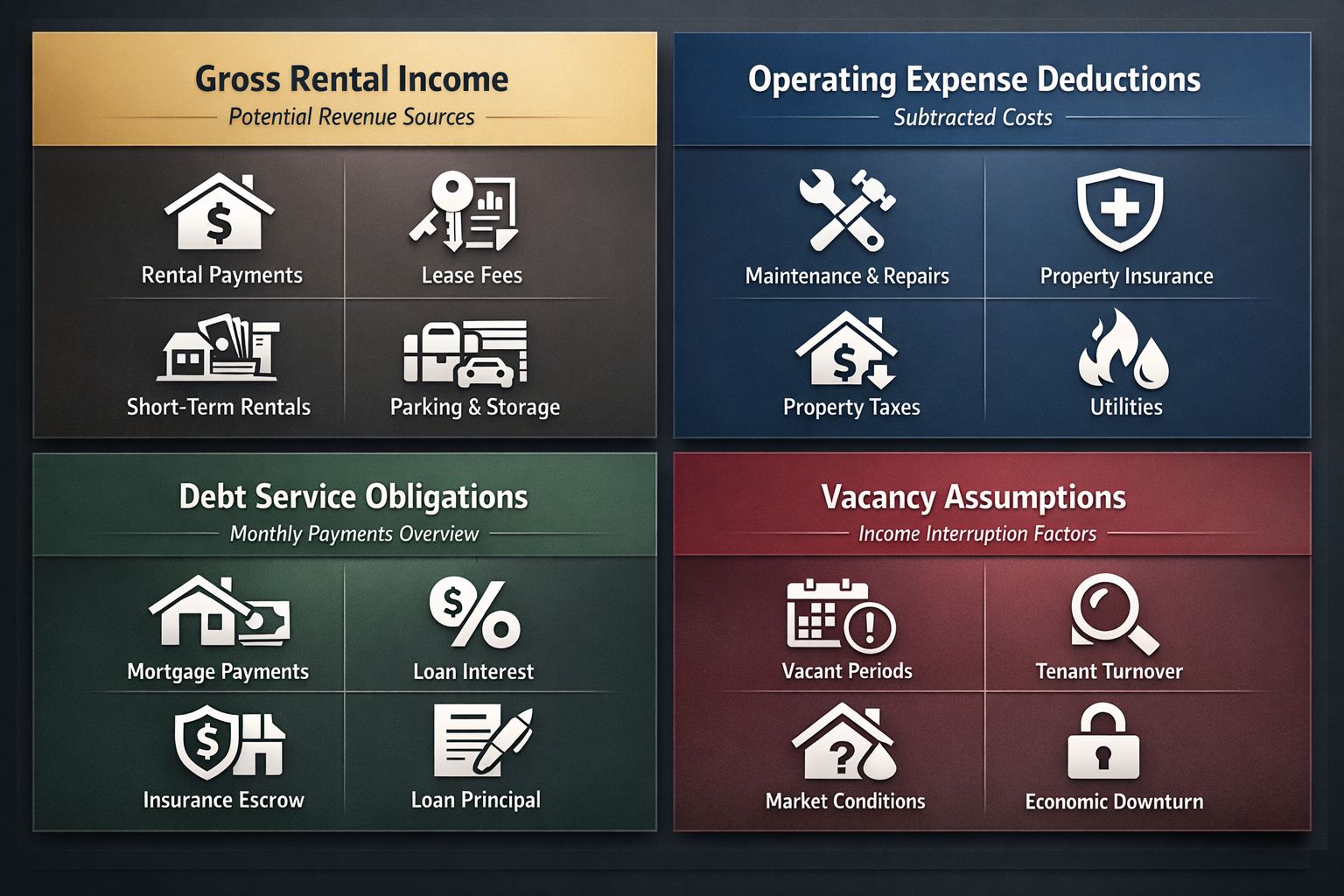

Essential Components of DSCR Analysis

When lenders evaluate your rental property's debt service coverage ratio, they examine several key components that determine the final calculation.

Gross rental income: This includes all potential rental revenue from the property, often based on current leases or market rent studies that provide realistic income projections for the area.

Operating expense deductions: Lenders typically subtract property taxes, insurance, maintenance reserves, and management fees to arrive at the net operating income figure used in their calculations.

Debt service obligations: This encompasses the total monthly principal and interest payments, and may include other debt-related costs depending on the loan structure and lender requirements.

Vacancy assumptions: Many lenders apply vacancy factors ranging from 5% to 10% to account for potential rental income interruptions and provide a more conservative assessment.

Income Coverage Formula Variables

The income coverage formula that lenders use involves several variables that can significantly impact your DSCR calculation and loan approval prospects.

Market rent assessments: Professional appraisers or rent studies help lenders determine realistic income potential, especially when current rents might be below market rates or when properties are vacant.

Expense ratio calculations: Lenders often use standardized expense ratios based on property type and location, though they may accept detailed operating statements for properties with established income histories.

Seasonal income adjustments: For properties in seasonal markets, lenders might average income over 12 months or apply specific adjustments to account for fluctuating rental demand throughout the year.

Multiple unit considerations: Multi-family properties may receive different treatment, with lenders potentially applying higher vacancy factors or using unit-by-unit analysis for larger buildings.

Expense Assumptions in Underwriting

Understanding how lenders calculate DSCR can help investors prepare more accurate financial projections for their DSCR loan applications.

Standard expense percentages: Many lenders use industry benchmarks that typically range from 35% to 50% of gross rental income, depending on property type, age, and local market conditions.

Required reserve accounts: Some lenders mandate monthly escrows for property taxes and insurance, while others might require additional reserves for maintenance and capital improvements.

Management fee considerations: Even if you self-manage properties, lenders often include management fees in their calculations, usually ranging from 8% to 12% of gross rental income.

Utility responsibility factors: Properties where landlords pay utilities receive different expense treatment, with lenders adding these costs to their operating expense calculations.

Step-by-Step DSCR Calculation Process

Following the systematic approach that lenders use can help investors better prepare their financing applications and optimize their property's financial presentation.

Determine gross rental income: Start with either existing lease rates or market rent assessments, ensuring the figures reflect realistic income potential based on current market conditions and property characteristics.

Calculate net operating income: Subtract all operating expenses including property taxes, insurance, maintenance, management fees, and any vacancy allowances to arrive at the property's true cash flow.

Identify total debt service: Include principal and interest payments for the proposed loan, and factor in any existing debt that will remain on the property after the new financing.

Apply the DSCR formula: Divide the net operating income by the total debt service to get your ratio, with most lenders requiring results above 1.0 for loan approval.

Review and optimize: Analyze areas where you might improve the ratio through rent increases, expense reductions, or different loan structures that could enhance your financing terms.

Underwriting Logic Behind DSCR Requirements

Lenders apply specific underwriting logic when evaluating DSCR calculations, and understanding their perspective can improve your loan approval chances.

Risk assessment priorities: Lenders focus on the property's ability to generate consistent cash flow rather than borrower income, making DSCR loans particularly attractive for investors with multiple properties or irregular personal income streams.

Market condition adjustments: Underwriters may apply different DSCR requirements based on local market stability, property types, and economic conditions that could affect rental income sustainability over the loan term.

Portfolio diversification factors: Some lenders consider your overall investment portfolio when setting DSCR requirements, potentially offering better terms to investors with demonstrated experience and diversified holdings.

Property quality considerations: Newer properties or those in prime locations might qualify for lower DSCR requirements, while older buildings or properties in transitional areas could face higher ratio demands.

Mastering how lenders calculate DSCR puts real estate investors in a stronger position to secure favorable financing terms and grow their portfolios effectively. The income coverage formula, expense assumptions, and underwriting logic all work together to determine whether your rental property qualifies for DSCR loans and at what terms.

By understanding these calculation methods, investors can make strategic improvements to their properties' financial profiles before applying for financing. This might involve optimizing rent levels, reducing operating expenses, or choosing loan structures that enhance the overall DSCR ratio.

As the lending landscape continues to evolve, staying informed about DSCR calculation methodologies helps investors maintain access to competitive financing options and capitalize on market opportunities as they arise.