DSCR Loan for Small Multifamily Properties: Your Complete Investment Guide

Real estate investors targeting small multifamily properties often find themselves caught between residential and commercial lending requirements. A DSCR loan for small multifamily investments might offer the perfect solution, allowing you to secure financing based on the property's income potential rather than your personal financial statements. These loans typically work well for properties with 5 to 20 units, where traditional lending approaches may fall short of investor needs.

Understanding how lenders evaluate small multifamily properties can make the difference between securing favorable terms and facing unnecessary delays. The underwriting process focuses heavily on the property's ability to generate consistent cash flow, making rent roll analysis and expense ratio review critical components of your loan application.

Common Questions About DSCR Multifamily Financing

Investors often have specific questions when exploring DSCR financing options for their multifamily acquisitions.

Q: What makes a DSCR loan different from traditional multifamily financing?

DSCR loans focus primarily on the property's debt service coverage ratio rather than the borrower's personal income documentation. This approach can be particularly beneficial for investors with multiple properties or complex income structures, as lenders evaluate the investment based on its cash flow potential.

Q: Can I use a DSCR loan for properties with 5 to 20 units?

Yes, many lenders offer DSCR financing for small multifamily properties in this range. However, underwriting requirements may vary depending on the property size, with some lenders requiring more detailed rent roll analysis for larger unit counts.

Q: How important is the expense ratio review in the approval process?

The expense ratio review is typically a crucial component of DSCR loan underwriting. Lenders need to verify that your property's operating expenses align with market standards to ensure accurate cash flow projections and sustainable debt service coverage.

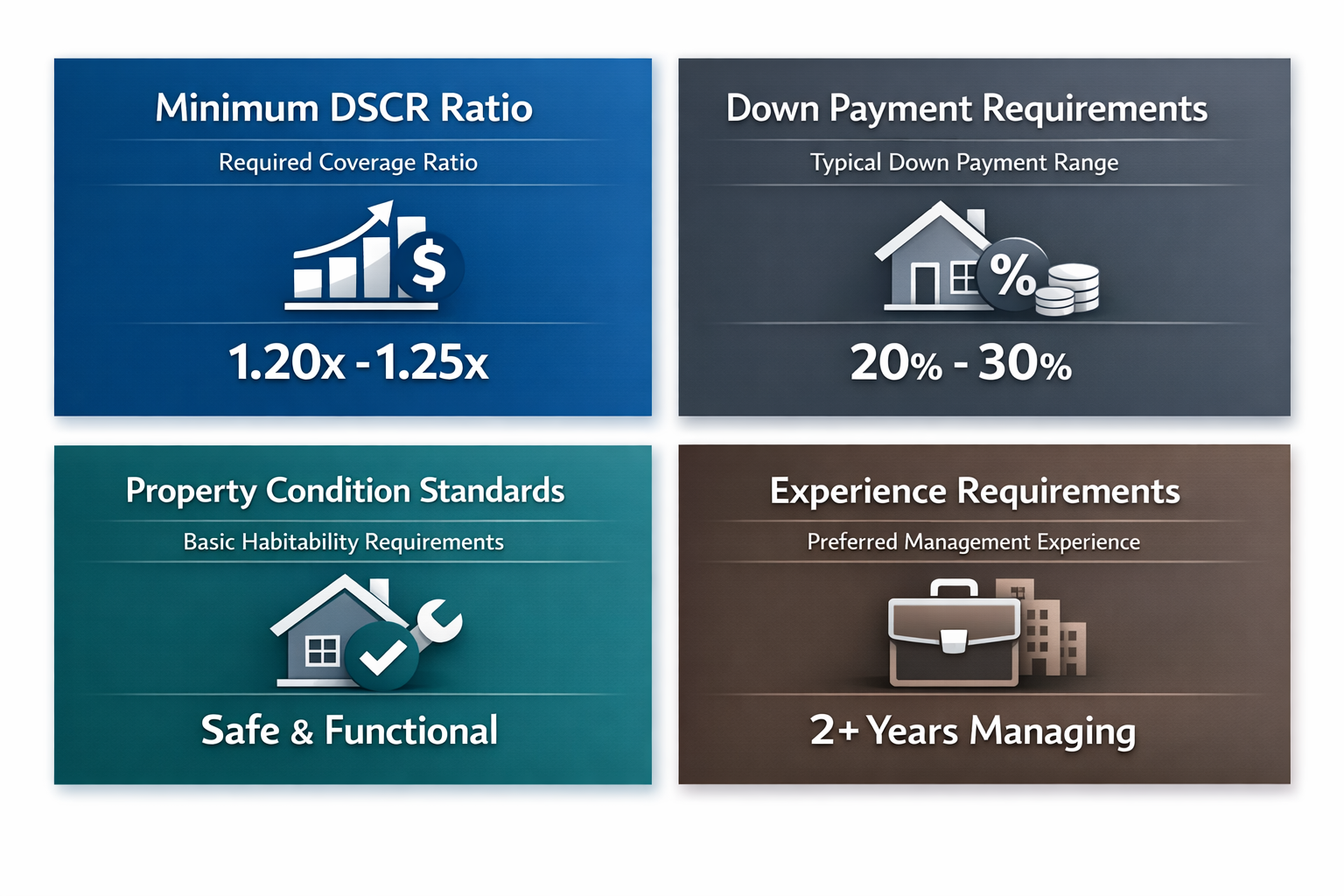

Key Qualification Requirements for Small Multifamily DSCR Loans

Meeting the qualification requirements for small multifamily DSCR loans requires understanding what lenders prioritize during their evaluation process.

Minimum DSCR Ratio: Most lenders require a debt service coverage ratio of at least 1.0 to 1.25, though some may accept slightly lower ratios with compensating factors like larger down payments or stronger property locations.

Down Payment Requirements: DSCR loans for small multifamily properties typically require down payments ranging from 20% to 25%, with some lenders offering up to 85% LTV ratios for qualified investors.

Property Condition Standards: The property must meet basic habitability requirements and pass a professional appraisal, with some lenders requiring additional inspections for older buildings or properties needing significant repairs.

Experience Requirements: While not universal, many lenders prefer borrowers with existing multifamily management experience, particularly for properties with higher unit counts in the 15 to 20 unit range.

Essential Components of Rent Roll Analysis

A thorough rent roll analysis forms the foundation of your DSCR loan application, providing lenders with the income data they need to evaluate your property's cash flow potential.

Current Rent Documentation: Provide detailed records of current rental rates for each unit, including lease start dates, terms, and any pending rent increases that could affect future cash flow projections.

Vacancy Rate Assessment: Document historical vacancy rates and provide realistic projections based on local market conditions, as lenders typically apply conservative vacancy assumptions during underwriting.

Market Rent Comparisons: Include comparable rent data from similar properties in your area to demonstrate that your current rents align with market rates or show potential for increases.

Tenant Quality Indicators: While not always required, information about tenant payment history and lease renewal rates can strengthen your application by showing stable occupancy patterns.

Understanding Expense Ratio Review Process

The expense ratio review helps lenders verify that your property's operating costs are reasonable and sustainable, directly impacting your loan's debt service coverage calculation.

Operating Expense Categories: Document all major expense categories including property management, maintenance, insurance, property taxes, and utilities, ensuring you capture both fixed and variable costs accurately.

Market Expense Comparisons: Lenders often compare your expense ratios to industry benchmarks for similar properties, so be prepared to explain any significant deviations from typical ranges.

Capital Expenditure Planning: While not always included in operating expenses, having a clear capital improvement plan can demonstrate your understanding of long-term property maintenance needs.

Step-by-Step Application Process for DSCR Multifamily Loans

Following a systematic approach to your DSCR loan application can help streamline the approval process and improve your chances of securing favorable terms.

Gather Financial Documentation: Collect recent rent rolls, operating statements, tax returns for the property, and bank statements showing rental income deposits to establish a clear financial picture.

Obtain Professional Appraisal: Schedule a professional appraisal early in the process, as this often becomes a bottleneck and is required for final loan approval and terms determination.

Submit Complete Application Package: Provide all required documentation upfront, including property photos, lease agreements, and any relevant property management contracts to avoid delays during underwriting.

Review and Negotiate Terms: Once you receive initial approval, carefully review the proposed terms and negotiate any aspects that don't align with your investment strategy or market expectations.

Market Considerations for Small Multifamily Investments

Understanding current market dynamics can help you position your DSCR loan application more effectively and identify opportunities for better returns.

Interest Rate Environment: With DSCR loan rates starting around 5.42% in some markets, timing your application during favorable rate periods can significantly impact your overall investment returns.

Geographic Market Selection: Focus on markets with strong rental demand and reasonable price-to-rent ratios, as these factors directly influence your property's debt service coverage potential.

Property Type Preferences: Lenders may have preferences for certain property types or age ranges within the small multifamily category, so understanding these preferences can guide your property selection.

Future Market Trends: Consider how demographic shifts and employment patterns in your target market might affect long-term rental demand and property values.

Securing a DSCR loan for small multifamily properties requires careful preparation and understanding of lender requirements, but the benefits often justify the effort. By focusing on properties with strong cash flow potential and presenting comprehensive rent roll analysis and expense ratio documentation, you can position yourself for approval even in competitive lending environments.

The key to success lies in treating your DSCR loan application as a business case for your investment rather than a personal lending request. When you can demonstrate that your property generates sufficient income to cover its debt service with room for unexpected expenses, lenders gain confidence in your investment's long-term viability.

Remember that DSCR lending continues to evolve, with new programs and requirements emerging regularly. Staying informed about current market conditions and maintaining relationships with experienced multifamily lenders can help you access the best financing options as opportunities arise in your local market.