Real estate investors who manage their own properties face unique challenges when securing financing. A DSCR loan with self managed rental properties offers an attractive solution, focusing on the property's income potential rather than personal income documentation. These loans evaluate your property's debt service coverage ratio, which measures whether rental income can adequately cover mortgage payments. For self-managing investors, understanding the specific requirements and documentation standards becomes crucial for successful loan approval. This financing approach may provide greater flexibility for investors with variable personal incomes while leveraging their property management skills to demonstrate cash flow stability.

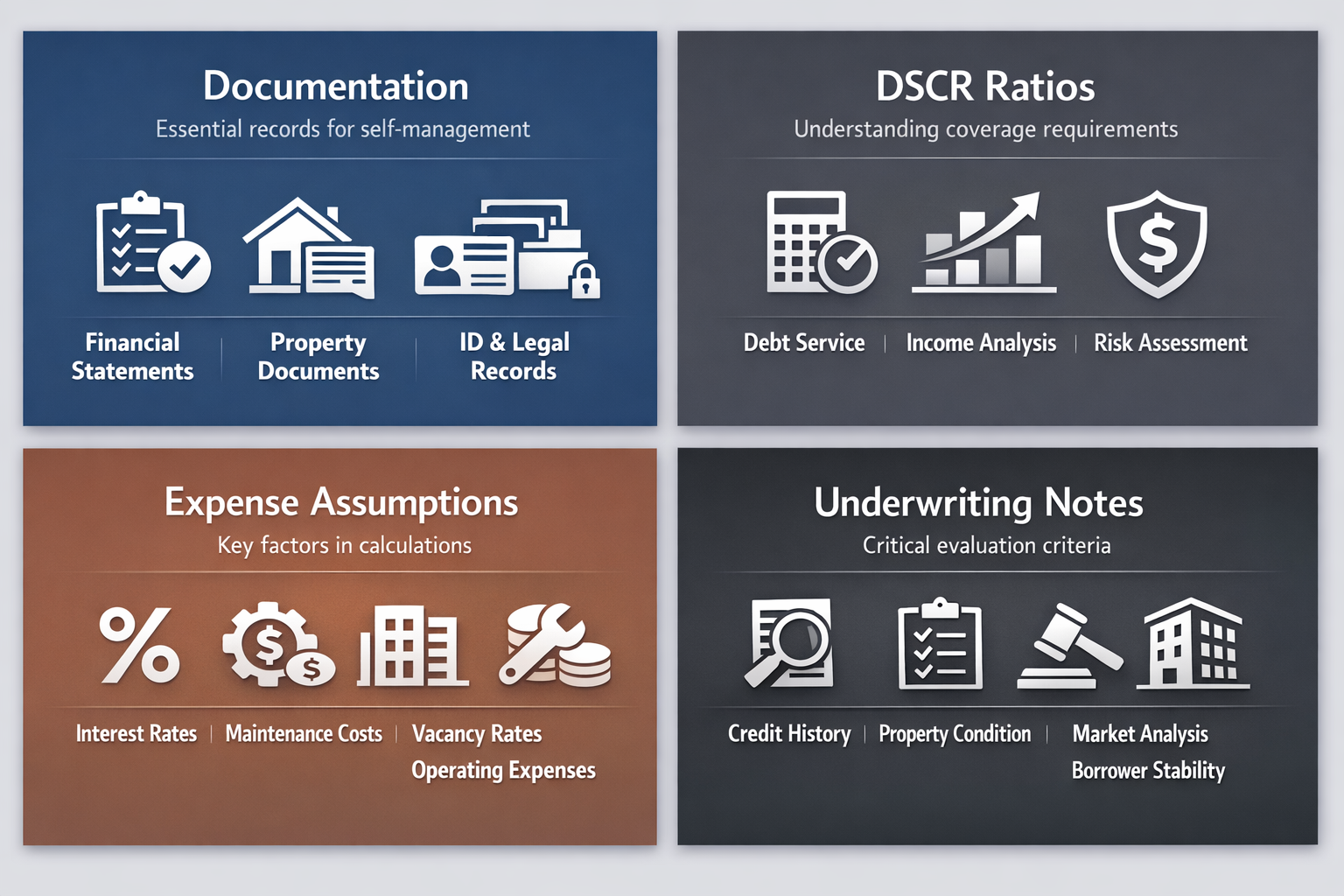

Essential Documentation for Self-Managed Properties

Essential documentation for self-managed properties requires careful preparation and organization to meet lender standards. When you're handling property management independently, lenders typically require more comprehensive records to verify income stability and management competence.

Current lease agreements showing rental terms, monthly payment amounts, and tenant information for all units in the investment property

Bank statements demonstrating consistent rental income deposits over the past 12-24 months, with clear identification of rental payments

Property management documentation including maintenance records, expense tracking, and evidence of responsible property oversight

Tax returns or Schedule E forms reflecting rental income and expenses from previous years to establish income patterns

Understanding DSCR Requirements and Ratios

Understanding DSCR requirements and ratios helps investors position their properties for loan approval. Lenders typically seek a debt service coverage ratio between 1.0 and 1.25, though some may accept lower ratios depending on other factors.

Minimum DSCR threshold of 1.00 ensures rental income fully covers mortgage payments, with higher ratios improving approval odds

Property income calculation based on current market rents or existing lease agreements, whichever provides more conservative estimates

Expense assumptions that lenders apply to account for vacancy rates, maintenance costs, and property management fees even for self-managed properties

Monthly debt service calculations including principal, interest, taxes, and insurance to determine the complete payment obligation

Self Management Documentation Strategies

Self management documentation strategies can strengthen your loan application by demonstrating professional property oversight. Lenders may view self-managed properties as higher risk without proper documentation systems in place.

Organized financial records separating rental income and property expenses in dedicated accounts to show clear cash flow management

Maintenance and repair logs documenting property upkeep, contractor relationships, and preventive maintenance schedules

Tenant communication records showing professional tenant relations, lease enforcement, and timely resolution of property issues

Market analysis documentation supporting rental rate decisions and demonstrating knowledge of local rental properties market conditions

Expense Assumptions in DSCR Calculations

Expense assumptions in DSCR calculations often surprise self-managing investors, as lenders may apply standard expense ratios regardless of actual management costs. Understanding these assumptions helps investors prepare realistic expectations for loan qualification.

Vacancy allowances typically range from 5-10% of gross rental income, even if your property maintains full occupancy historically

Maintenance reserves may be calculated at 10-15% of rental income to account for ongoing property upkeep and unexpected repairs

Property management fees could be included in calculations even when self-managing, often estimated at 8-12% of rental income

Insurance and tax escalations projected over the loan term to ensure the DSCR remains stable despite potential cost increases

Underwriting Notes for Self-Managed Properties

Underwriting notes for self-managed properties focus on risk assessment and income verification beyond standard property evaluation. Lenders may apply additional scrutiny to ensure sustainable cash flow and competent property management.

Property condition assessments become more critical as lenders evaluate whether self-management maintains adequate property standards and value

Rental income verification requires thorough documentation of payment history, tenant stability, and market rate justification

Experience evaluation where lenders may consider your property management track record, real estate investor history, and local market knowledge

Cash flow sustainability analysis examining whether current rental income patterns can reasonably continue throughout the loan term

Exit strategy considerations reviewing your ability to maintain payments if rental income decreases or property management becomes challenging

Securing a DSCR loan with self managed rental properties requires thorough preparation and understanding of lender expectations. Success typically depends on maintaining comprehensive documentation that demonstrates both property performance and management competence. While self-management can reduce operating expenses and increase cash flow, lenders may still apply conservative expense assumptions in their calculations. Investors who organize their records professionally, understand DSCR requirements, and prepare for underwriting scrutiny often find these loans provide valuable financing flexibility. The key lies in treating your self-managed properties with the same documentation standards that professional management companies would maintain, ensuring lenders can confidently assess your investment's income potential and your capability as a property manager.