Real estate investors who rely on cash flow and rental income know that DSCR loans offer a powerful path to scale portfolios without traditional income verification. But what happens when you're ready to refinance and the appraisal comes in lower than expected? A dscr loan refinance with appraisal gap issues can stall your timeline, reduce available equity, and force you back to the drawing board.

Appraisal gaps occur when the property's assessed market value falls short of the purchase price or the amount needed to support your refinance goals. For investors, this isn't just a minor inconvenience. It can limit loan-to-value ratios, increase cash requirements, and even jeopardize deal approval. Understanding how to manage valuation disputes and explore reconsideration strategies can help you push through approval delays and secure the financing you need.

This guide walks through the most effective approaches for handling appraisal shortfalls during DSCR refinancing, so you can protect your investment and keep your projects moving forward.

What Is a DSCR Loan Refinance With Appraisal Gap Issues?

A dscr loan refinance with appraisal gap issues happens when the property appraisal comes in below the value you expected or needed to complete your refinance. DSCR loans, which qualify investors based on the rental income a property generates rather than personal income, still depend on accurate property valuations to determine how much a lender will finance.

Q: Why does an appraisal gap matter in a DSCR refinance?

An appraisal gap matters because lenders use the appraised value to calculate your loan-to-value ratio. If the appraisal is lower than anticipated, the lender may reduce the amount they're willing to lend, require you to bring more cash to closing, or delay approval while they review alternative documentation. This can impact your cash-out goals, your ability to pay off existing debt, or your plan to fund additional investments.

Q: Are appraisals always required for DSCR loans?

In most cases, appraisals are required to confirm fair market value and protect both the lender and investor from overleveraging. The appraisal process ensures that the property is worth the investment and that loan terms align with current market conditions. Accurate valuations help investors avoid overpayment and manage risk, especially in fluctuating or competitive markets.

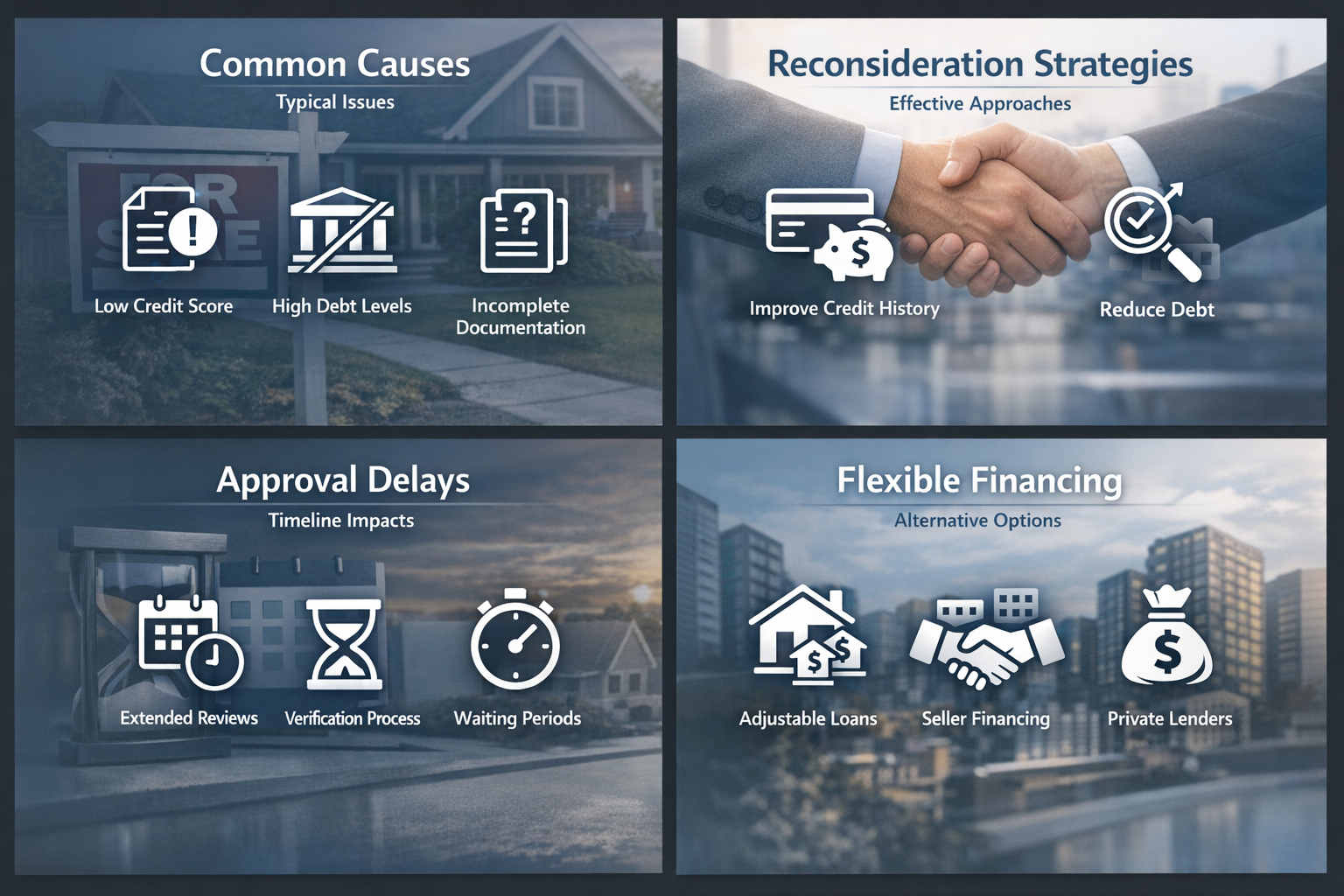

Common Causes of Valuation Disputes in DSCR Refinancing

Valuation disputes during DSCR refinancing often stem from a handful of common issues. Knowing what typically causes appraisal gaps can help you prepare and respond more effectively.

Use of outdated or irrelevant comparable properties: Appraisers rely on recent sales of similar properties in the area. If the comparables selected don't accurately reflect your property's condition, location, or features, the valuation may fall short.

Market volatility or rapid shifts: In fast-moving or declining markets, appraisals might not keep pace with recent changes in property values. This can result in appraisals that don't align with current investor expectations or contract prices.

Appraiser oversight or errors: Mistakes happen. An appraiser might miss key improvements, incorrectly measure square footage, or overlook income-generating features like updated units or additional rentable space.

Property condition concerns: If the property has deferred maintenance, outdated systems, or cosmetic issues, the appraiser may adjust the value downward to reflect repair costs or reduced marketability.

Understanding these causes allows you to anticipate potential problems and gather documentation that strengthens your case if a reconsideration becomes necessary.

Strategies for Challenging a Low Appraisal

When you receive an appraisal that's lower than expected, it's not the end of the road. You have several reconsideration strategies available to dispute the valuation and potentially adjust the outcome.

Request a detailed appraisal review: Start by carefully reviewing the appraisal report for errors or omissions. Look for inaccurate property details, incorrect square footage, missing improvements, or inappropriate comparable sales. Document any discrepancies clearly.

Provide additional comparable sales data: If you believe the appraiser used poor comparables, gather recent sales of similar properties that better reflect your property's value. Submit these along with a formal request for reconsideration of value to your lender.

Highlight property improvements and income performance: If you've made significant upgrades or the property generates strong rental income that wasn't fully considered, compile receipts, rental agreements, and cash flow statements to support a higher valuation.

Consider ordering a second appraisal: In some cases, lenders may allow a second appraisal if the first contains clear errors or if you can demonstrate that the initial appraiser lacked adequate local market knowledge.

These strategies may help close the appraisal gap or at least reduce it enough to move forward with your refinance on more favorable terms.

How Approval Delays Impact Your Refinance Timeline

Approval delays caused by appraisal gaps can disrupt your refinancing schedule and affect other parts of your investment strategy. Understanding the potential timeline impacts helps you plan contingencies and manage expectations.

Extended underwriting and review periods: When a lender receives a low appraisal, they may pause the approval process to conduct additional reviews, request more documentation, or evaluate whether they can proceed with adjusted terms. This can add weeks to your closing timeline.

Renegotiation or restructuring requirements: If the appraisal gap is significant, you might need to renegotiate loan terms, increase your down payment, or adjust the loan amount. Each of these steps takes time and may require new approvals from both your lender and any other parties involved.

Impact on other investment opportunities: Delays in one refinance can tie up capital you planned to use elsewhere. If you're juggling multiple properties or looking to fund new acquisitions, a prolonged approval process can limit your flexibility and slow portfolio growth.

Being aware of these potential delays allows you to build buffer time into your plans and explore backup financing options if needed.

Step-by-Step Process to Address an Appraisal Gap

When faced with a dscr loan refinance with appraisal gap issues, following a structured approach can improve your chances of a successful resolution. Here's a step-by-step process investors can use to tackle the problem.

Review the appraisal report thoroughly: As soon as you receive the appraisal, read through it carefully. Check all property details, measurements, comparable sales, and adjustments. Highlight any errors or areas that seem inconsistent with the property's true value or market conditions.

Gather supporting documentation: Collect evidence that supports a higher valuation. This might include recent sales data, inspection reports, renovation receipts, rent rolls, or income statements. Organize everything in a clear, professional format.

Submit a formal reconsideration of value request: Contact your lender and request a reconsideration of value. Provide your supporting documentation and a written explanation of why you believe the appraisal is inaccurate. Be specific and factual, avoiding emotional or subjective language.

Explore alternative financing structures: If the appraisal cannot be changed, work with your lender to explore options such as bringing additional cash to closing, adjusting the loan amount, or considering non-QM loan products that may offer more flexible underwriting criteria.

Consider negotiating the purchase or refinance terms: If you're refinancing to pull cash out or consolidate debt, evaluate whether adjusting your goals slightly can still meet your investment needs while accommodating the lower appraisal.

This methodical approach helps you address the appraisal gap efficiently and keeps your refinance on track.

Exploring Non-QM and Flexible Financing Alternatives

When a traditional DSCR loan refinance hits a wall due to appraisal gaps, non-QM loans and other flexible financing alternatives can provide a path forward. These alternatives often use different underwriting criteria that may help you bridge the valuation gap.

Understand how non-QM loans handle appraisal gaps: Non-QM loans can offer more flexibility by allowing investors to supplement lower appraisals with other documentation, such as cash flow statements, bank records, or alternative income verification. This can make it easier to close deals in competitive or volatile markets where appraisals might lag behind offer prices.

Evaluate portfolio lenders and private financing: Some portfolio lenders hold loans on their own books and may have more discretion in how they evaluate appraisals and loan terms. Private or hard money lenders might also consider factors beyond appraised value, such as exit strategy, investor experience, or overall deal structure.

Consider blended or layered financing structures: In some cases, combining a primary DSCR loan with a second lien, seller financing, or additional private capital can help you cover the appraisal gap without needing to bring excessive cash to the table.

Weigh the costs and benefits: Flexible financing options may come with higher interest rates, shorter terms, or additional fees. Run the numbers carefully to ensure the cost of bridging the appraisal gap doesn't erode your investment returns or cash flow.

Exploring these alternatives gives you more tools to work with when appraisal issues threaten to derail your refinance plans.

Dealing with a dscr loan refinance with appraisal gap issues can be frustrating, but it doesn't have to stop your investment momentum. By understanding the causes of valuation disputes, preparing strong reconsideration strategies, and exploring flexible financing alternatives, you can navigate approval delays and find solutions that keep your projects moving forward.

The key is to act quickly, stay organized, and work closely with your lender to identify the best path. Whether that means challenging the appraisal, adjusting your financing structure, or tapping into non-QM loan options, informed investors have multiple strategies at their disposal.

At Trulo Mortgage, we specialize in helping real estate investors overcome financing challenges like appraisal gaps. Our team understands the unique needs of rental property investors and can guide you through DSCR loan refinancing with clarity and confidence. If you're facing an appraisal shortfall or want to explore your options before you refinance, reach out today to discuss how we can help you close your next deal.