Financing Properties with Shared Amenities Explained

May 26, 2026

•

7 min read

Understanding DSCR Loans for Properties with Shared Amenities

Real estate investors increasingly encounter properties that feature shared amenities, from community pools and fitness centers to common gardens and parking structures. When you're evaluating a DSCR loan for properties with shared amenities, the financing process becomes more nuanced than a straightforward single-family rental. These properties often operate within homeowners associations or similar governance structures that add layers of cost allocation and underwriting complexity.

For investors focused on rental income strategies, understanding how lenders assess properties with shared spaces is critical. The presence of association dues, maintenance responsibilities, and revenue-sharing arrangements can significantly impact your debt service coverage ratio and, ultimately, your ability to secure favorable financing terms. This guide walks through the essential considerations that shape DSCR lending for properties with communal features, helping you position your investment for approval.

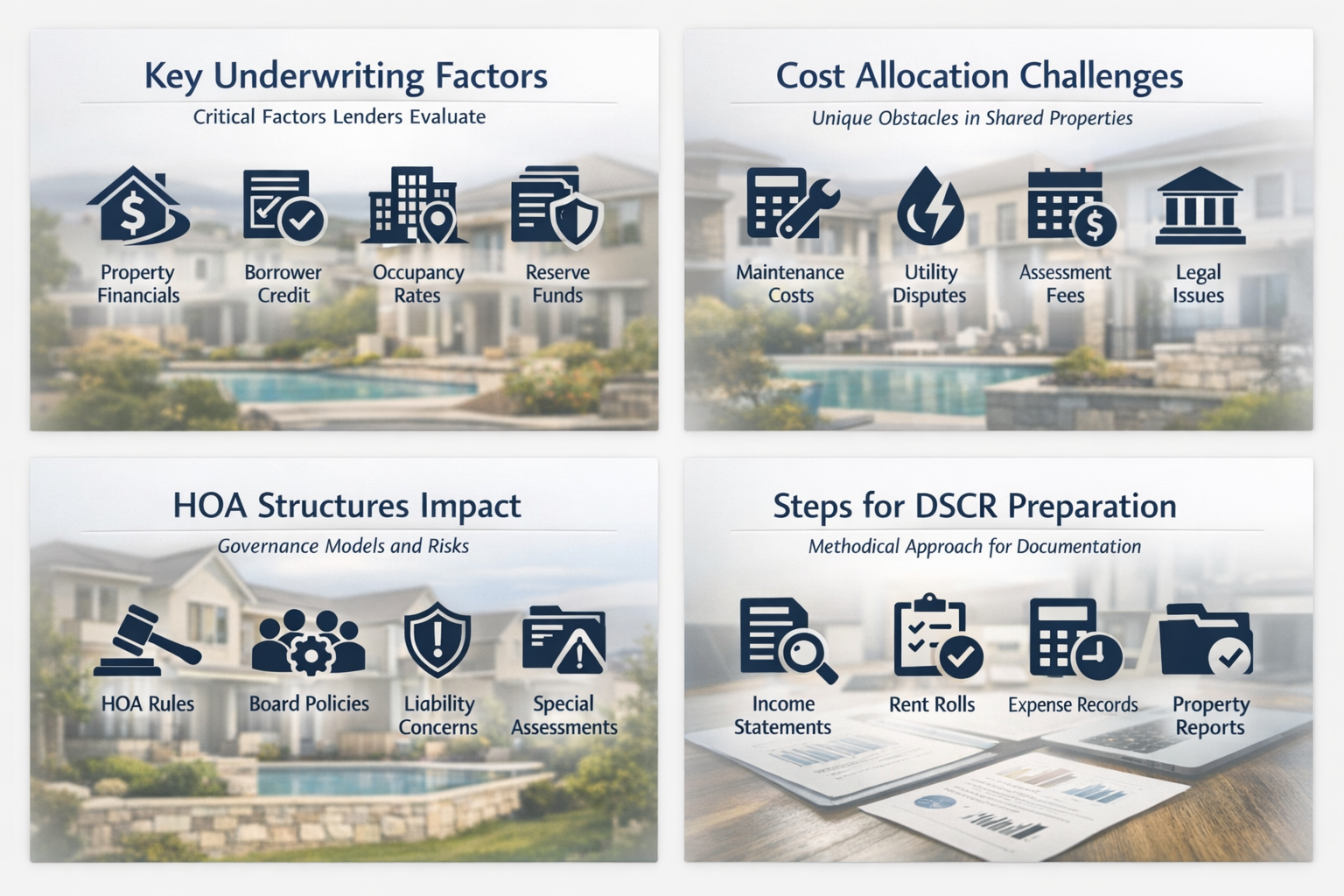

Key Underwriting Factors Lenders Evaluate

When you apply for a DSCR loan for properties with shared amenities, lenders examine several critical factors that differ from traditional single-family financing. Key underwriting factors lenders evaluate during underwriting include the property's net operating income after accounting for all shared-cost obligations and how those expenses affect your debt service coverage ratio.

Net Operating Income Calculation: Lenders typically subtract association dues and shared maintenance costs from your potential gross rent before calculating the debt service coverage ratio, which may reduce your qualifying income.

Association Financial Health: The stability and reserve levels of the HOA or property association can influence lender confidence, as special assessments or underfunded reserves pose risk to ongoing cash flow.

Property Type Classification: Mixed-use properties or rent-by-the-room arrangements with shared amenities may face different underwriting standards compared to conventional single-family rentals.

Debt Service Coverage Benchmarks: Most lenders prefer a DSCR of at least 1.20 to 1.25, meaning your net operating income should exceed your debt service by 20 to 25 percent to account for the additional complexity of shared-cost structures.

Cost Allocation Challenges in Shared Amenity Properties

Cost allocation challenges in shared amenity properties create unique obstacles during the underwriting process. When multiple units or owners share facilities, determining each party's financial responsibility requires careful documentation and transparent accounting practices.

Variable Monthly Dues: HOA fees might fluctuate based on usage, occupancy levels, or deferred maintenance projects, making it harder to project stable net operating income over the loan term.

Special Assessments: Unexpected capital improvements to shared spaces can result in one-time or multi-year assessments that temporarily reduce your cash flow and affect your ability to service debt.

Revenue Attribution: In properties where shared amenities generate income, such as laundry facilities or parking fees, lenders need clear documentation showing how that revenue is allocated and whether it offsets operating expenses.

HOA Structures and Their Impact on Financing

HOA structures and their impact on financing can determine whether your investment property qualifies for a DSCR loan at competitive terms. Different governance models carry varying levels of risk from a lender's perspective, particularly when those structures control significant portions of the property's operating budget.

Master-Planned Communities: Large-scale developments with comprehensive amenity packages may impose higher monthly fees, but they often provide detailed financial statements and reserve studies that reassure lenders.

Condo and Townhome Associations: These structures typically feature more extensive shared amenities and complex bylaws that can restrict rental activity or impose investor caps, potentially affecting your exit strategy.

Voluntary vs. Mandatory Membership: Properties where association membership is optional might present lower predictability in maintenance funding, which could raise red flags during underwriting for a DSCR loan for properties with shared amenities.

Steps to Prepare Your Property for DSCR Underwriting

Preparing your property for DSCR underwriting when shared amenities are involved requires a methodical approach to documentation and financial transparency. Following these steps can streamline the approval process and help you secure better loan terms.

Gather Association Documents: Collect at least two years of HOA financial statements, budgets, reserve studies, and meeting minutes to demonstrate the association's fiscal responsibility and long-term planning.

Document Rental Income Accurately: Provide lease agreements, rent rolls, and historical income records that clearly separate your unit's revenue from any shared-income sources like parking or amenity fees.

Calculate Net Operating Income Conservatively: Subtract all association dues, insurance premiums, property taxes, and estimated maintenance costs before presenting your cash flow projections to the lender.

Obtain a Property Appraisal Early: A professional appraisal that accounts for shared amenities and comparable sales within similar HOA structures helps establish realistic loan-to-value expectations.

Review Association Bylaws for Rental Restrictions: Confirm there are no lease caps, minimum rental periods, or investor quotas that could limit your ability to generate income or resell the property in the future.

Navigating Mixed-Use and Rent-by-the-Room Properties

Navigating mixed-use and rent-by-the-room properties introduces additional layers of underwriting complexity when pursuing a DSCR loan. These property types often feature shared amenities that serve both residential and commercial tenants, requiring lenders to evaluate multiple income streams and occupancy dynamics.

Separate Income Streams: Clearly delineate residential rental income from commercial lease revenue, as lenders may apply different underwriting criteria or loan-to-value ratios to each component.

Shared Space Management: Demonstrate that common areas like lobbies, hallways, or courtyards are maintained by a formal management structure or association, reducing the risk of deferred maintenance impacting property value.

Occupancy and Lease Terms: Rent-by-the-room arrangements with shared kitchens or bathrooms may require individual lease documentation and proof that each tenant contributes to overall net operating income reliably.

Zoning and Compliance Verification: Ensure the property's mixed-use status or shared-housing model complies with local zoning ordinances and building codes, as violations can delay or derail financing approval.

Optimizing Your Debt Service Coverage Ratio

Optimizing your debt service coverage ratio becomes essential when shared amenities increase your operating expenses and reduce net income. Investors who proactively manage costs and revenue can often meet or exceed the preferred DSCR thresholds that lenders require.

Increase Rental Income: Consider market-rate adjustments, lease renewals with escalation clauses, or value-add improvements that justify higher rents without triggering significant association fee increases.

Reduce Discretionary Expenses: Audit your property management fees, maintenance contracts, and utility allocations to identify savings opportunities that improve your net operating income.

Negotiate HOA Fees: While association dues are typically fixed, participating actively in board meetings or cost-reduction initiatives may lead to fee stabilization or reductions that benefit all owners.

Refinance Strategically: If your current debt service is high, explore refinancing options or loan restructuring that lowers monthly payments and raises your DSCR above the 1.20 minimum threshold.

Final Considerations for Shared Amenity Investments

Final considerations for shared amenity investments revolve around balancing the appeal of communal features with the financial realities of association governance and underwriting complexity. Properties with pools, gyms, and common spaces can command premium rents and attract quality tenants, but they also require investors to maintain higher operating reserves and navigate more detailed lender scrutiny. By preparing thorough documentation, understanding cost allocation structures, and maintaining a conservative approach to net operating income projections, you position yourself for success when seeking a DSCR loan for properties with shared amenities. The key is demonstrating to lenders that the benefits of shared features outweigh the risks, ensuring your investment generates consistent cash flow and meets or exceeds debt service requirements over the long term.

Securing financing for properties with shared amenities doesn't have to be overwhelming if you approach the process with a clear understanding of lender expectations and cost allocation realities. DSCR loans offer a powerful tool for real estate investors who want to leverage rental income rather than personal earnings, even when dealing with complex HOA structures and communal spaces. By focusing on strong net operating income, transparent association financials, and a debt service coverage ratio that exceeds typical benchmarks, you can navigate underwriting complexity with confidence.

As you evaluate your next investment opportunity, remember that properties with shared amenities often provide competitive advantages in tenant attraction and retention. The financing process may require extra documentation and careful planning, but the potential for steady cash flow and portfolio diversification makes these properties worth the effort. Whether you're exploring mixed-use buildings, rent-by-the-room models, or traditional condos with resort-style features, understanding how lenders assess shared-cost structures will help you make informed decisions and secure favorable loan terms.