Financing Properties Through Recent Tenant Turnover

April 17, 2026

•

7 min read

Tenant turnover is one of those inevitable headaches that every real estate investor faces at some point. One day you've got steady rental income flowing in, and the next, you're staring at a vacancy gap that could last weeks or even months. For investors looking to refinance or acquire new properties during these transitions, the timing can feel downright awful.

Here's the good news: a DSCR loan for properties with recent tenant turnover might offer a path forward when traditional financing would slam the door shut. Unlike conventional mortgages that scrutinize your personal income and employment history, DSCR loans focus primarily on the property's ability to generate cash flow. This approach can be particularly valuable when you're dealing with income instability caused by tenant changes.

Understanding how lenders evaluate properties with vacancy gaps and what approval considerations come into play can make the difference between closing a deal or watching it slip away. Let's dive into how these investor-focused loans work and what strategies can help you navigate financing during periods of tenant transition.

What Makes DSCR Loans Different During Tenant Transitions

What makes DSCR loans different during tenant transitions is their fundamental focus on property performance rather than borrower income. While traditional lenders might panic at the sight of recent tenant turnover, DSCR lenders typically take a more measured approach to evaluating your property's financing potential.

The debt service coverage ratio itself measures whether your property generates enough rental income to cover the mortgage payment. Lenders calculate this by dividing the property's monthly or annual rental income by its debt obligations. A DSCR of 1.0 means the property breaks even, while anything above indicates positive cash flow. Most lenders prefer to see ratios ranging from 1.0 to 1.25 or higher, though some programs may accept lower thresholds.

When tenant turnover enters the picture, the calculation becomes more nuanced. Lenders understand that vacancy is part of the rental business, but they still need confidence that the property can perform once re-tenanted. This is where the property's location, condition, and market rental rates become critical factors in the approval process.

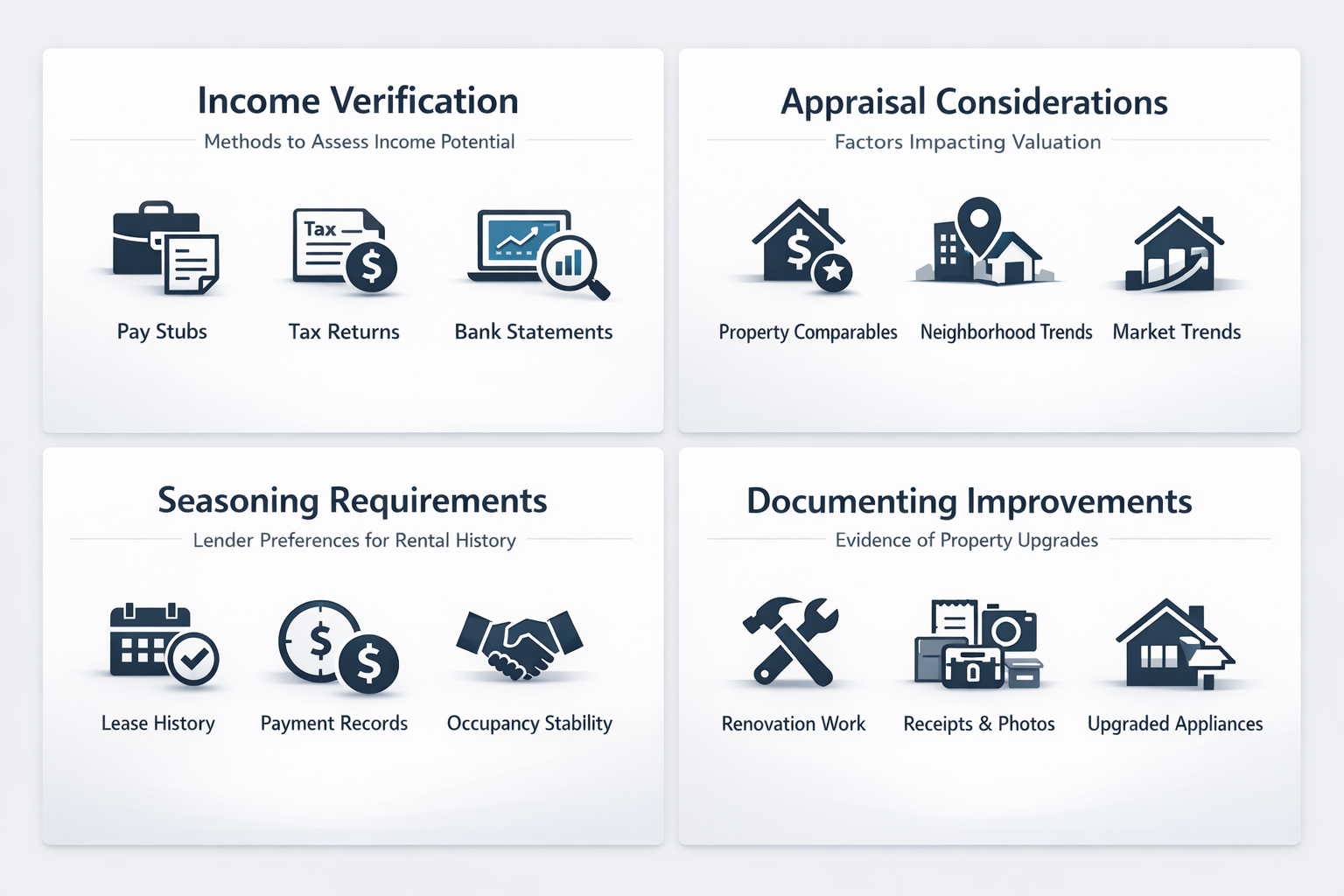

Income verification methods: Instead of relying solely on current lease agreements, some lenders may use market rent analysis to determine the property's income potential. This approach can work in your favor if you're between tenants but the property commands strong market rents in its area.

Appraisal considerations: The appraiser will typically provide a market rent opinion as part of the valuation process. If recent tenant turnover occurred because you're upgrading the property or repositioning it for higher rents, the appraisal might reflect that upside potential.

Seasoning requirements: Some lenders may have specific seasoning requirements, meaning they prefer properties with established rental history. However, many DSCR programs are flexible enough to work with properties experiencing temporary vacancy gaps.

Key Approval Considerations When Income Shows Gaps

Key approval considerations when income shows gaps often revolve around how lenders assess risk and potential. When you're applying for a DSCR loan for properties with recent tenant turnover, understanding what underwriters look for can help you position your application more effectively.

Documentation becomes your best friend during this process. Even if you don't have a current tenant in place, you'll want to demonstrate the property's income-generating capability through other means. Market rent comparables, previous lease agreements, and rental history all paint a picture of what the property can reasonably produce.

Establish market rent credibility: Gather comparable rental data from similar properties in your area. The more evidence you can provide that your property will command competitive rents once occupied, the stronger your application becomes. Property management companies or local real estate agents can often provide this documentation.

Highlight property improvements: If the vacancy gap resulted from renovations or upgrades, document the work completed and how it positions the property for higher rents. Before and after photos, contractor invoices, and upgraded feature lists all support your case that the property will perform well.

Demonstrate investor experience: While DSCR loans don't typically require extensive documentation of your personal income, showing a track record of successful property management can reassure lenders. If you've successfully navigated tenant transitions before, that experience matters.

Prepare for reserve requirements: Some lenders may require higher cash reserves when financing properties with recent turnover. Having six to twelve months of mortgage payments in liquid reserves shows you can weather extended vacancy periods if needed.

Smart Strategies to Strengthen Your DSCR Application

Smart strategies to strengthen your DSCR application can turn a borderline deal into an approval, especially when income instability raises concerns. The key is demonstrating that the vacancy gap represents a temporary situation rather than a fundamental problem with the property.

Time your application strategically: If possible, wait until you have a signed lease agreement or at least solid rental applications in hand before submitting your loan application. Even a lease that hasn't started yet can significantly strengthen your position. Some lenders will use future lease income in their calculations if the lease is signed and the tenant has been screened.

Consider a larger down payment: Reducing your loan-to-value ratio can offset concerns about recent tenant turnover. A lower LTV means less risk for the lender and might help you qualify even with a temporarily lower DSCR. Many DSCR programs offer more favorable terms at 75% LTV compared to 80% or higher.

Shop multiple DSCR lenders: Different lenders have varying appetites for properties with recent vacancy gaps. Some specialize in working with investors during transition periods, while others prefer only fully stabilized properties. Don't assume one rejection means all lenders will pass on your deal.

Prepare a property business plan: While not always required, a simple one-page overview explaining the vacancy situation, your re-tenanting strategy, and projected timeline can address lender concerns proactively. This shows you're thinking strategically about the property rather than simply reacting to circumstances.

How Lenders Calculate DSCR With Incomplete Rental History

How lenders calculate DSCR with incomplete rental history varies somewhat between programs, but most follow similar general approaches. Understanding these methods helps you anticipate what numbers will appear in your loan analysis and how to present your property most favorably.

When current rental income is unavailable due to vacancy, lenders typically turn to market rent analysis. The appraiser will research comparable properties in your area, looking at similar size, condition, and location factors. This market rent figure then becomes the basis for calculating your DSCR, even if no tenant currently occupies the property.

Market rent appraisal method: The appraiser provides an opinion of market rent based on recent comparable rentals. This figure gets multiplied by 12 to create an annual income projection, which is then divided by the annual debt service. This method can work well if your property is in a strong rental market with clear comparables.

Lease agreement method: If you have a signed lease for a future move-in date, many lenders will use that actual lease amount rather than estimated market rent. This provides the most certainty and often results in smoother underwriting since there's less estimation involved.

Historical average method: Some lenders may look at the property's rental history over the past 12 to 24 months and use an average figure. If the property was rented successfully before the recent turnover, this historical data can support your current application.

Adjusted income method: A few lenders might reduce the market rent figure by a vacancy factor, typically 5% to 10%, to account for realistic occupancy rates. This conservative approach helps ensure the DSCR calculation reflects real-world performance rather than best-case scenarios.

Common Mistakes to Avoid With Turnover Properties

Common mistakes to avoid with turnover properties can save you time, money, and frustration during the financing process. Even experienced investors sometimes stumble when applying for a DSCR loan during vacancy periods, often due to preventable missteps.

Failing to document the vacancy reason: Lenders want context. Was the turnover due to normal lease expiration, property improvements, or tenant issues? Providing a brief explanation helps underwriters understand the situation isn't a red flag about the property's desirability or your management capabilities.

Overestimating market rents: It's tempting to use optimistic rent figures, especially when you need the income to hit a certain DSCR threshold. However, inflated projections that don't match market comparables will get caught during appraisal. Stick with realistic, defensible numbers that align with actual market conditions.

Neglecting property presentation: If the property is vacant during the appraisal, make sure it shows well. A neglected, dirty, or damaged-looking property will appraise lower and raise questions about its rental potential. Clean, stage lightly if possible, and complete any obvious repairs before the appraiser visits.

Ignoring cash reserve requirements: Don't drain your bank accounts to maximize your down payment if it leaves you with insufficient reserves. Many DSCR lenders require proof of several months of reserves, and being cash-poor after closing can actually disqualify you.

Missing the lease-up timeline: If you tell a lender you'll have the property re-tenanted within 30 days, make sure that timeline is realistic. Some lenders may follow up post-closing, and establishing credibility matters for future financing relationships.

Alternative Income Documentation During Vacancy Gaps

Alternative income documentation during vacancy gaps can bridge the credibility gap when current rent rolls don't tell the full story. DSCR lenders who work regularly with investors understand that properties cycle through vacancy periods, and they've developed various ways to evaluate income potential beyond just current occupancy.

Property management projections: If you work with a professional property management company, their written opinion on market rent and expected lease-up timeline carries weight with lenders. These third-party assessments provide objective validation of your property's income potential. A letter from your property manager outlining comparable rents and typical vacancy periods for similar properties can support your application.

Previous tax returns for the property: If you've owned the property for a while, Schedule E from your tax returns shows historical rental income. This documentation proves the property has generated income in the past and can do so again once re-tenanted. Even if recent months show vacancy, the overall pattern matters.

Rental applications or interest documentation: If you've been marketing the property and have received applications or serious inquiries, documentation of this interest demonstrates demand. Email exchanges with prospective tenants, showing requests, or application copies all indicate the property will rent successfully.

Neighborhood rental demand data: Market reports showing low vacancy rates in your area, average days on market for rental properties, or rising rent trends all support the case that your property represents a temporary vacancy rather than a problematic asset. Local rental market reports from real estate associations or property management companies can provide this data.

Navigating financing for properties with recent tenant turnover doesn't have to derail your investment strategy. A DSCR loan for properties with recent tenant turnover offers a practical solution by focusing on the property's income potential rather than fixating on temporary vacancy gaps. This approach recognizes the reality of rental property investing: turnover happens, but strong properties in good markets will perform over time.

The key to success lies in understanding what lenders need to see and positioning your property accordingly. Market rent documentation, clear explanations of the vacancy situation, and demonstrated property quality all work together to build confidence in your application. While income instability might create hurdles with traditional financing, DSCR lenders who specialize in investor properties often have the flexibility to look beyond short-term gaps.

Remember that different lenders have different appetites for properties in transition. What one lender views as too risky, another might see as a standard investor scenario. Taking time to shop multiple DSCR programs and prepare thorough documentation can make all the difference in securing favorable financing terms.

At Trulo Mortgage, we understand that real estate investing doesn't follow a perfectly linear path. Tenant turnover, property upgrades, and market repositioning are all part of building a successful rental portfolio. If you're dealing with vacancy gaps or income instability and need financing that works with your situation rather than against it, reach out to explore your DSCR loan options. The right financing partner can turn a temporary challenge into your next successful deal.