Real estate investors who focus on renovating rental properties face unique financing challenges that traditional mortgages often can't address effectively. A DSCR loan for newly renovated rentals provides a strategic solution by qualifying investors based on property income rather than personal financial statements. This approach proves particularly valuable for experienced investors who've completed substantial renovations and need financing that reflects their property's enhanced rental potential.

Understanding how DSCR loans work with renovated properties requires knowledge of post rehab valuation methods, optimal refinance timing, and rent repositioning strategies. These loans typically feature interest rates between 6.5% and 8.75% for residential investment properties, with qualification requirements that might include minimum credit scores of 740 and down payments of at least 25%.

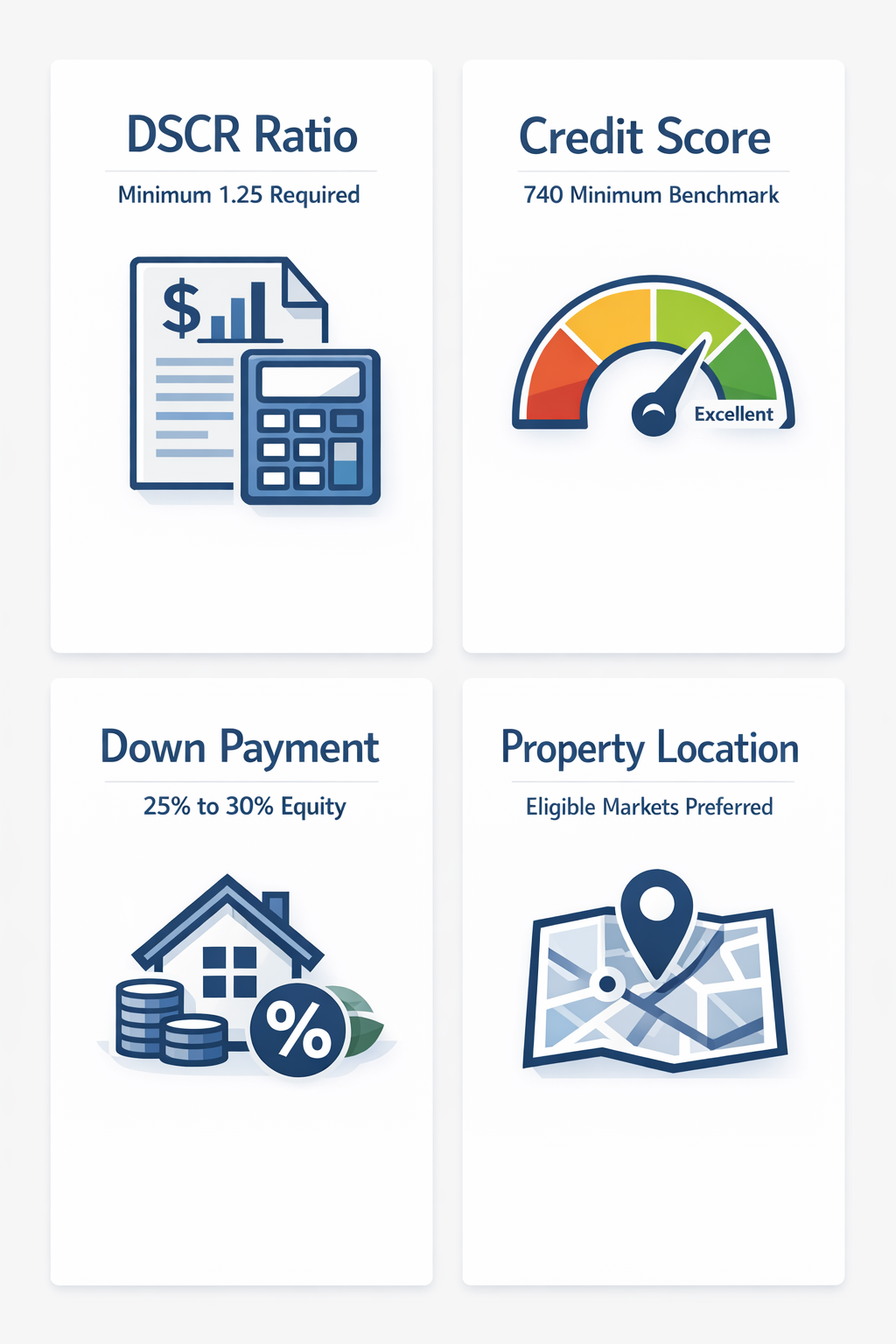

Essential DSCR Loan Qualification Requirements

Essential DSCR loan qualification requirements establish the foundation for securing financing on your renovated rental properties. These criteria ensure lenders can confidently assess your property's income-generating potential after renovations.

Minimum DSCR ratio of 1.25 or greater - Your property's net operating income must exceed debt service payments by at least 25%

Credit score requirement of 740 minimum - This benchmark reflects the non-qualified mortgage standards for investment property lending

Down payment of 25% to 30% - Higher equity requirements help offset the increased risk associated with investment properties

Property location restrictions - Single-family homes in eligible markets typically receive priority consideration

Down Payment and LTV Considerations

Down payment and LTV considerations directly impact your ability to maximize leverage while securing favorable loan terms for newly renovated rentals. Understanding these requirements helps you structure deals more effectively.

Standard down payment range of 20% to 25% - Most lenders require substantial equity to mitigate investment property risks

LTV ratios based on post-renovation value - Completed improvements can increase your borrowing capacity through higher appraised values

Cash-out refinancing opportunities - Renovated properties may qualify for higher loan amounts based on improved valuations

Portfolio considerations for multiple properties - Experienced investors might access more favorable terms across their rental property portfolio

Current Interest Rate Environment

Current interest rate environment for DSCR loans reflects market conditions that directly affect your renovation project profitability and cash flow projections. These rates influence your overall investment strategy.

Rate range between 6.5% and 8.75% - Residential investment properties typically fall within this spectrum based on risk assessment

Rate variations based on credit profile - Higher credit scores and stronger financial positions may secure lower end rates

Property type and location impact - Single-family rentals in stable markets often receive more competitive pricing

Post rehab valuation strategies maximize your property's appraised value to optimize financing terms and borrowing capacity. These approaches ensure your renovation investments translate into measurable equity gains.

Document all improvement costs with receipts and permits - Comprehensive records demonstrate value-add investments to appraisers and underwriters

Schedule appraisal after lease-up completion - Occupied properties with established rent rolls provide stronger income validation

Provide comparable sales of recently renovated properties - Market evidence supports higher valuations for similar improvement levels

Highlight energy efficiency and modern amenity upgrades - These improvements often command premium rents and property values

Optimal Refinance Timing Considerations

Optimal refinance timing considerations help you transition from construction or bridge financing to long-term DSCR loans while maximizing your property's financial performance. Timing affects both approval odds and loan terms.

Complete all renovations before loan application - Finished properties receive more accurate valuations and streamlined underwriting

Establish six months of rental income history - Documented cash flow strengthens your debt service coverage calculations

Monitor interest rate cycles for favorable conditions - Rate improvements can significantly impact long-term profitability

Coordinate with tax planning for optimal deduction timing - Refinancing costs and renovation expenses require strategic tax consideration

Rent Repositioning for Maximum DSCR

Rent repositioning for maximum DSCR involves strategic rental rate adjustments that optimize your debt service coverage ratio while maintaining competitive market positioning. This approach directly impacts loan qualification and terms.

Research comparable rentals with similar renovation levels - Market analysis supports higher rent justification during underwriting review

Implement phased rent increases for existing tenants - Gradual adjustments maintain occupancy while improving cash flow performance

Focus on high-impact amenities that command rent premiums - Updated kitchens, bathrooms, and HVAC systems typically justify significant increases

Document utility savings and efficiency improvements - Lower operating costs improve net operating income calculations

Strategic Implementation Success

Strategic implementation success with DSCR loans for newly renovated rentals requires coordinating renovation completion, tenant placement, and financing applications to achieve optimal results. Successful investors typically focus on properties that can achieve debt service coverage ratios well above the 1.25 minimum requirement, creating buffer room for market fluctuations. The combination of completed renovations, market-rate rents, and strong credit profiles positions investors for favorable loan terms that support long-term portfolio growth and cash flow optimization.

DSCR loans provide a powerful financing tool for investors focused on renovated rental properties, offering qualification based on property performance rather than personal income. Success requires understanding current market rates between 6.5% and 8.75%, meeting qualification standards including 740 credit scores and 25% down payments, and timing applications after renovation completion and tenant placement.

The strategic use of post rehab valuation techniques, combined with effective rent repositioning and optimal refinance timing, can maximize both your property's income potential and your borrowing capacity. As the DSCR loan market continues evolving, investors who master these fundamentals will maintain competitive advantages in acquiring and financing high-quality rental properties.