Navigating DSCR Loans for Properties with Challenging Occupancy Rates

High vacancy properties often present unique financing challenges that can discourage even experienced real estate investors. However, securing a DSCR loan for high vacancy properties remains possible when you understand the right approach and strategies.

Unlike traditional mortgages that rely heavily on borrower income, DSCR loans focus on the property's ability to generate rental income. This shift in evaluation criteria creates opportunities for investors dealing with income instability, though it also introduces specific risk factors that lenders carefully assess.

The key lies in understanding how lenders evaluate these properties and positioning your application to address their primary concerns about cash flow and long-term viability.

Essential Do's for DSCR Loan Success

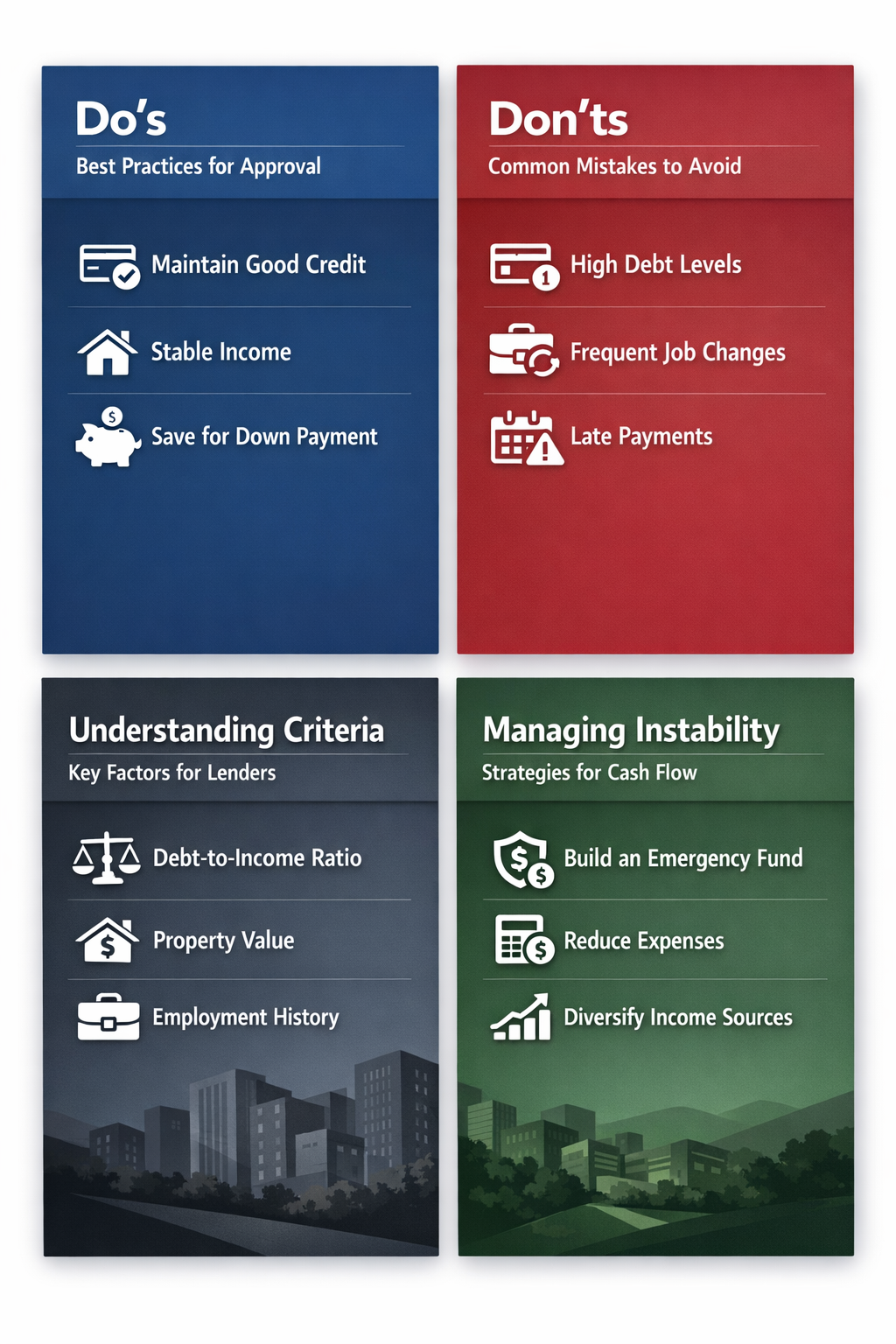

When pursuing a DSCR loan for high vacancy properties, following proven best practices can significantly improve your approval odds and help you navigate the complexities of income instability.

Leverage projected market rent data: Lenders typically base their approval decisions on projected market rent rather than current occupancy, which provides a pathway for vacant properties to qualify for financing.

Maintain substantial cash reserves: Building and demonstrating adequate reserves shows lenders you can handle periods of income instability and cover expenses during vacancy periods.

Provide comprehensive market analysis: Present detailed comparable rent studies and market data to support your projected income figures and justify the property's rental potential.

Document your investment experience: Highlight your track record with similar properties to demonstrate your ability to manage challenging assets and minimize risk factors.

Prepare for higher down payments: Expect lenders to require larger down payments for high vacancy properties as a way to mitigate their exposure to potential losses.

Critical Don'ts That Could Derail Your Application

Understanding what to avoid when applying for a DSCR loan for high vacancy properties is equally important as knowing what to do. These common mistakes can lead to immediate rejection or unfavorable terms.

Don't rely on unverifiable rental income projections: Lenders need concrete evidence to support your income claims, and vague or unsupported projections often result in loan denials.

Don't over-leverage based on optimistic scenarios: Conservative projections help you avoid financial strain if market conditions shift or vacancy periods extend longer than anticipated.

Don't ignore local market volatility: Failing to account for regional economic factors and rental market instability can create unrealistic expectations and poor investment decisions.

Don't underestimate carrying costs: Properties with income instability require careful budgeting for extended periods without rental income, including taxes, insurance, and maintenance.

Understanding Lender Risk Assessment Criteria

Understanding lender risk assessment criteria helps investors better position their applications and address potential concerns about high vacancy properties before they become deal-breakers.

Debt Service Coverage Ratio calculations: Lenders typically require a DSCR of at least 1.0 to 1.25, meaning the property's projected rental income must cover debt payments with some buffer for risk factors.

Property condition and marketability: The physical condition and location desirability directly impact a property's ability to attract tenants and maintain stable occupancy rates.

Local rental market stability: Lenders examine area vacancy rates, population trends, and economic indicators to assess the likelihood of achieving projected rental income.

Borrower liquidity and reserves: Adequate cash reserves demonstrate your ability to handle income instability and unexpected expenses without defaulting on the loan.

Exit strategy viability: Lenders want assurance that the property can be sold or refinanced if needed, which requires realistic valuation based on comparable sales and market conditions.

Preparing Your Property for DSCR Loan Approval

Preparing your property for DSCR loan approval involves addressing both physical and financial aspects that lenders consider when evaluating high vacancy properties and their income potential.

Complete necessary repairs and improvements: Address deferred maintenance and cosmetic issues that might deter potential tenants or reduce projected rental rates, as property condition directly affects marketability.

Obtain professional rent roll analysis: Work with qualified appraisers or property management companies to establish realistic market rent projections that lenders will accept as credible income estimates.

Document renovation plans and costs: If improvements are needed, provide detailed scopes of work and contractor estimates to show how investments will enhance rental income potential.

Research comparable properties thoroughly: Gather data on similar properties in your area, including their rental rates, vacancy periods, and occupancy histories to support your income projections.

Managing Income Instability During the Process

Managing income instability during the DSCR loan process requires strategic planning and clear communication with lenders about how you'll handle potential cash flow gaps.

Create detailed cash flow projections: Develop realistic scenarios that account for seasonal variations, tenant turnover periods, and potential extended vacancies that could affect your ability to service debt.

Establish relationships with property management companies: Professional management can help reduce vacancy periods and provide lenders with confidence in the property's income-generating potential.

Build contingency funds beyond minimum requirements: Maintain reserves that exceed lender requirements to demonstrate your commitment to the investment and ability to weather income instability.

Consider rent guarantee insurance options: Some investors explore insurance products that can provide income protection during vacancy periods, though these add to operating costs.

Securing a DSCR loan for high vacancy properties requires careful preparation and realistic expectations about both opportunities and challenges. While income instability and elevated risk factors create additional hurdles, lenders' focus on projected market rent rather than current occupancy provides a viable path forward for determined investors.

Success depends largely on your ability to present credible income projections, maintain adequate reserves, and demonstrate experience managing similar investments. The key lies in addressing lenders' concerns proactively rather than hoping they won't notice potential red flags.

As the DSCR loan market continues evolving, staying informed about changing requirements and market conditions will help you adapt your strategies effectively. Remember that while these loans offer flexibility for challenging properties, conservative underwriting and realistic projections protect your long-term investment success better than optimistic assumptions.