Unlocking Higher Returns with DSCR Loans and Rent-by-Room Strategies

Real estate investors constantly search for ways to boost their property income without dramatically increasing their workload. That's where a DSCR loan for rent by room strategy comes into play. Instead of leasing an entire property to one tenant, you're renting individual rooms to multiple occupants, potentially increasing your gross rental income significantly.

This approach has gained traction in densely populated urban areas and near colleges where demand for affordable individual rooms remains strong. When paired with DSCR financing, which focuses on property cash flow rather than personal income, investors can scale their portfolios faster while tapping into the growing co-living movement.

In this guide, we'll walk through how DSCR loans work for rent-by-room models, the financial advantages of co-living income, common lease structure considerations, and the underwriting challenges you might face. By the end, you'll have a clear roadmap for evaluating whether this strategy fits your investment goals.

Why Rent by Room Makes Financial Sense for Investors

Rent by room makes financial sense for investors because it often generates higher total monthly income compared to traditional single-tenant leases. Instead of receiving one rent check for the entire property, you're collecting multiple payments from individual tenants occupying separate rooms. This model can improve your property's net operating income, which directly impacts your ability to qualify for a DSCR loan.

Higher occupancy potential: Even if one room sits vacant, the other rooms continue generating income, reducing your overall vacancy risk and stabilizing cash flow.

Increased gross rents: Renting four rooms at 800 dollars each typically exceeds what you'd collect from a single family renting the whole unit, especially in markets near universities or employment hubs.

Improved DSCR ratios: Lenders calculate your debt service coverage ratio based on the property's income, so higher rental income from multiple tenants may qualify you for larger loan amounts or better terms.

Appeal in high-demand markets: Urban areas and college towns see strong demand for affordable room rentals, which can lead to shorter vacancy periods and consistent tenant interest.

Of course, this model isn't without its trade-offs. You'll typically face higher turnover, more tenant interactions, and potentially increased wear and tear. Still, for investors willing to manage these factors or hire property managers with co-living experience, the financial upside can be substantial.

How Lenders Calculate Income for DSCR Loans on Rent-by-Room Properties

How lenders calculate income for DSCR loans on rent-by-room properties can differ from traditional rental underwriting. Instead of looking at a single lease agreement, lenders may evaluate the total income generated by all rented rooms combined. This per-room income approach can work in your favor if you've structured leases carefully and can demonstrate consistent occupancy.

Room-based income projections: Lenders might assess the rental income potential of each room separately, then aggregate those figures to determine total monthly revenue for DSCR calculations.

Lease documentation: You'll typically need to provide individual lease agreements or a master lease with room-by-room rent schedules, showing clear proof of income from each tenant.

Occupancy assumptions: Some lenders apply a conservative occupancy rate, such as 85% or 90%, to account for turnover and vacancy periods inherent in rent-by-room models.

Market rent analysis: Expect lenders to compare your stated rents against local market data for similar room rentals to ensure your income projections are realistic and sustainable.

Because this model involves multiple tenants and lease structures that differ from standard residential rentals, not every lender will be comfortable underwriting it. Working with mortgage providers familiar with co-living income and rent-by-room strategies can streamline the approval process and help you secure favorable loan terms.

Co-Living Income and Its Impact on Loan Approval

Co-living income can have a significant impact on loan approval because it may outperform traditional rental models by 10 to 30 percent in net operating income. This boost comes from the combination of higher rents per square foot, shared amenities, and efficient use of space. For investors seeking DSCR loans, stronger cash flow translates directly into better debt service coverage ratios, which lenders use to assess risk.

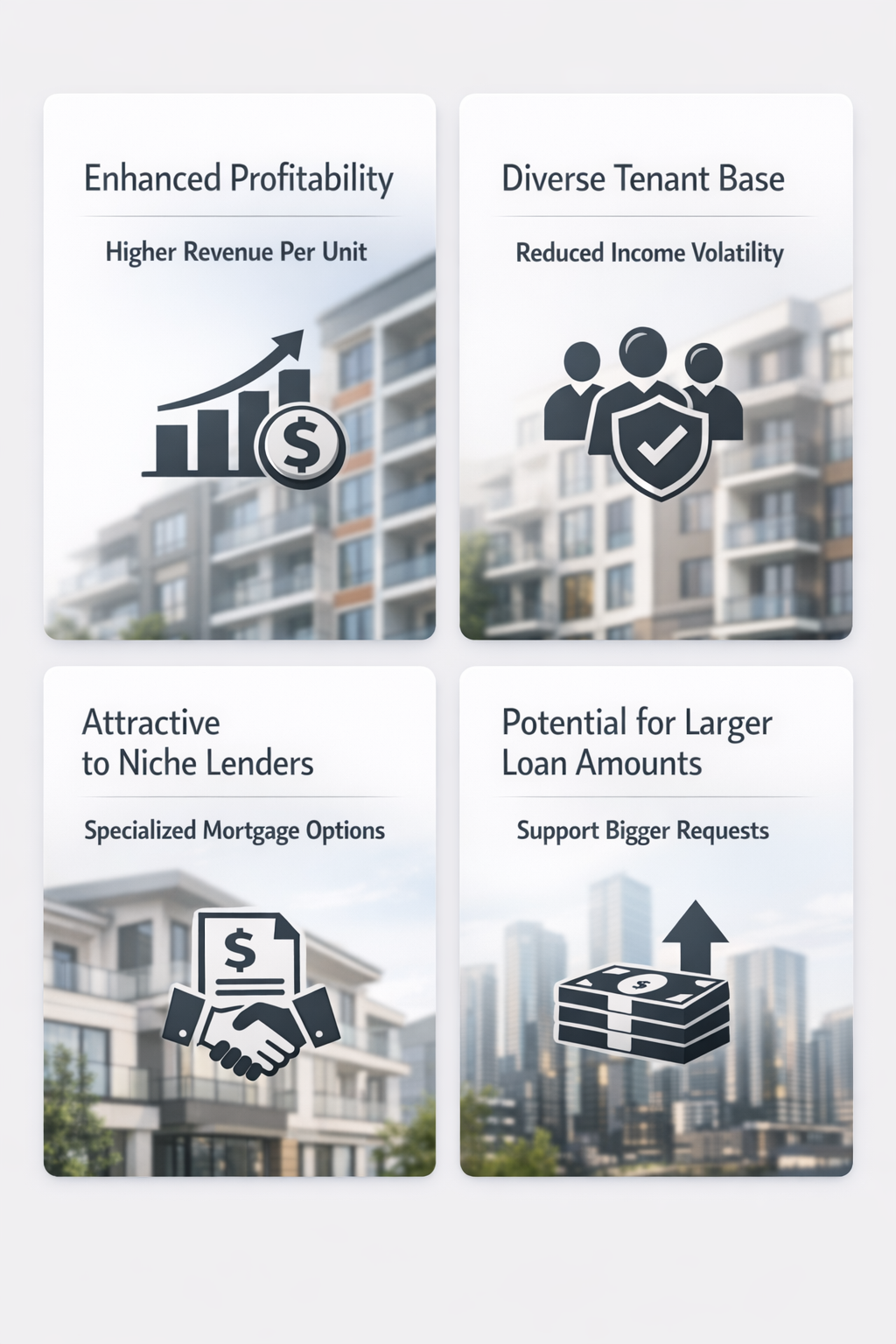

Enhanced profitability: Co-living properties often generate more revenue per unit than conventional rentals, improving your property's financial performance and making it easier to meet lender DSCR thresholds.

Diverse tenant base: Renting to multiple individuals can reduce income volatility, as the departure of one tenant doesn't eliminate all rental income at once.

Attractive to niche lenders: Some mortgage lenders specialize in investment properties with non-traditional income streams, and they may offer competitive rates for well-managed co-living setups.

Potential for larger loan amounts: Because lenders base DSCR loans on property income rather than your personal earnings, higher co-living income can support bigger loan requests and help you expand your portfolio faster.

That said, co-living income isn't guaranteed. You'll need to maintain high occupancy, manage tenant relationships effectively, and ensure your property meets local zoning and safety regulations. When done right, though, this income model can significantly strengthen your loan application and long-term investment returns.

Structuring Leases for Rent-by-Room Success

Structuring leases for rent-by-room success requires clarity, consistency, and compliance with local landlord-tenant laws. Unlike traditional leases that cover an entire dwelling, rent-by-room agreements must define each tenant's rights and responsibilities for their private space and any shared common areas. Getting this right protects you legally and ensures smooth operations that keep lenders confident in your property's income stability.

Individual vs. master leases: Decide whether each tenant signs a separate lease for their room or if all tenants sign a single master lease with room assignments. Individual leases may offer more flexibility and reduce disputes, but they also mean more paperwork and administrative effort.

Clear common area rules: Spell out how tenants share kitchens, bathrooms, living spaces, and other amenities. Include guidelines for cleanliness, quiet hours, guest policies, and maintenance responsibilities to minimize conflicts.

Rent collection and payment terms: Specify due dates, accepted payment methods, and late fee policies for each tenant. Consistent rent collection is critical for maintaining the cash flow that supports your DSCR loan obligations.

Move-in and move-out procedures: Outline security deposit handling, inspection processes, and notice requirements for lease termination. These details help you manage turnover efficiently and maintain occupancy levels lenders expect.

Lease structure also impacts how lenders view your property. Clean, well-documented agreements demonstrate professional management and reduce perceived risk. If you're new to rent-by-room investing, consulting with a real estate attorney familiar with co-living arrangements can help you create compliant, investor-friendly lease templates.

Common Underwriting Challenges and How to Overcome Them

Common underwriting challenges for rent-by-room properties often stem from lender unfamiliarity with the model and concerns about income volatility. Because DSCR loans rely heavily on projected rental income, any uncertainty in your numbers can lead to delays, lower loan amounts, or outright denials. Understanding these hurdles upfront lets you prepare stronger applications and choose lenders who specialize in non-traditional rental strategies.

Overestimating occupancy rates: Lenders worry that investors might project 100% occupancy year-round, which rarely happens. To counter this, provide conservative estimates backed by local market data and historical performance from similar properties.

Underestimating operating expenses: Rent-by-room models typically incur higher utility costs, maintenance, and turnover expenses. Show detailed budgets that account for these realities, proving you understand the true cost of running a co-living property.

Lack of comparable sales or income data: Traditional appraisals may struggle to find direct comps for rent-by-room properties. Work with appraisers experienced in multi-tenant or co-living valuations, and supplement their reports with your own income documentation.

Zoning and legal compliance concerns: Some municipalities have strict rules about the number of unrelated tenants allowed in a single dwelling. Verify your property meets all local codes and provide proof to lenders to avoid last-minute compliance issues.

Addressing these challenges proactively can make the difference between a smooth approval and a frustrating rejection. Transparency, realistic projections, and thorough documentation build lender trust and improve your chances of securing favorable DSCR loan terms for your rent-by-room investment.

Maximizing Property Performance in Co-Living Models

Maximizing property performance in co-living models goes beyond simply filling rooms. It involves creating an environment that attracts quality tenants, encourages longer stays, and maintains high occupancy rates. These factors directly influence your property's cash flow, which is the foundation of any DSCR loan approval and ongoing financial success.

Tenant screening and compatibility: Select tenants who are likely to coexist peacefully by conducting thorough background checks and setting clear expectations about shared living during the application process.

Amenities and community building: Offer features like high-speed internet, furnished common areas, and community events that make your property more appealing than competitors, reducing turnover and vacancy.

Proactive maintenance and communication: Address repair requests quickly and maintain open lines of communication with all tenants to prevent small issues from escalating into move-out triggers.

Regular financial monitoring: Track income, expenses, and occupancy trends monthly so you can adjust rents, marketing strategies, or property improvements as needed to sustain strong DSCR ratios.

Effective property management can be the deciding factor between a profitable co-living investment and a cash-draining headache. If you're managing multiple properties or prefer a hands-off approach, partnering with a property manager who specializes in co-living spaces might be worth the cost. Their expertise can help you maintain the performance metrics lenders look for when renewing or refinancing your DSCR loan.

Is a DSCR Loan for Rent by Room Right for Your Portfolio

Is a DSCR loan for rent by room strategy right for your portfolio? That depends on your investment goals, risk tolerance, and willingness to manage a more hands-on rental model. This approach can deliver impressive returns and strong cash flow, but it also demands more active involvement than traditional single-tenant properties.

Consider this strategy if you're targeting high-demand markets near universities, medical centers, or tech hubs where young professionals and students seek affordable housing. The ability to generate multiple income streams from one property can significantly improve your debt service coverage ratio, making it easier to qualify for financing and expand your holdings.

On the flip side, rent-by-room investing may not suit every investor. If you prefer long-term, low-maintenance tenants and minimal turnover, a traditional rental model might align better with your goals. You'll also need to ensure your property complies with local zoning laws and that you have systems in place to handle higher tenant turnover and more frequent communications.

Before diving in, run the numbers carefully. Calculate potential rental income using conservative occupancy assumptions, factor in realistic operating expenses, and compare your projected DSCR to lender requirements. If the math works and you're comfortable with the operational demands, a DSCR loan for rent by room could be a powerful addition to your investment strategy, unlocking higher income and faster portfolio growth.

A DSCR loan for rent by room strategy offers real estate investors a compelling path to higher rental income and improved cash flow. By renting individual rooms instead of entire units, you can tap into strong demand in urban and college markets while potentially boosting your net operating income by 10 to 30 percent compared to traditional models.

Success in this space requires careful attention to lease structures, realistic income projections, and thorough preparation for the underwriting process. Lenders who understand co-living income and room-based rental models can be valuable partners, helping you navigate the unique challenges and secure financing that supports your growth.

Whether you're exploring your first rent-by-room property or looking to scale an existing co-living portfolio, focus on strong property management, conservative financial planning, and clear communication with both tenants and lenders. With the right approach, this strategy can deliver impressive returns and position your portfolio for long-term success.