Real estate investors face a unique challenge when rental markets soften and property values plateau. The debt service coverage ratio loan remains a powerful tool for building portfolios, but qualifying for a DSCR loan for properties in declining markets requires a different approach than financing properties in booming areas. Lenders become more selective, appraisals carry greater weight, and demonstrating sustainable cash flow becomes critical.

Understanding how rent pressure, appraisal risk, and lender sensitivity interact can mean the difference between closing your next deal and watching opportunities slip away. Many investors assume that declining markets automatically disqualify them from favorable financing terms, but that's not necessarily the case. The key lies in knowing how to position your properties and present your investment thesis in ways that address lender concerns head-on.

This guide walks through the essential strategies for securing DSCR financing even when market indicators point downward. From preparing robust income projections to leveraging alternative loan structures, you'll learn how to navigate the challenges that come with investing during market corrections.

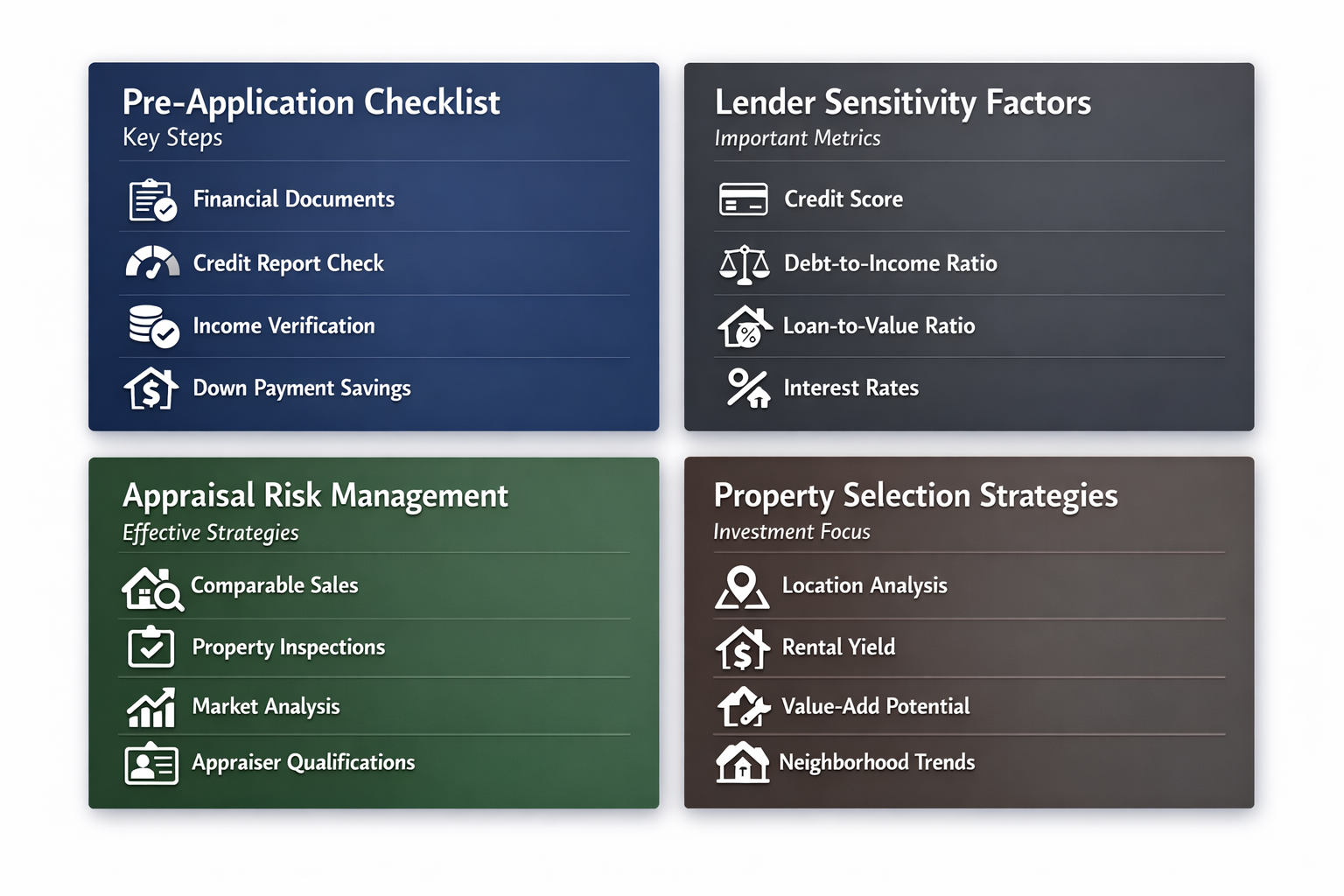

Pre-Application Preparation Checklist

Pre-application preparation can significantly improve your chances of securing a DSCR loan for properties in declining markets. When lenders sense market weakness, they scrutinize applications more carefully, which means your documentation and analysis need to be exceptionally thorough. Getting ahead of lender questions before they're asked demonstrates sophistication and reduces the perceived risk of your investment.

Compile comprehensive market analysis: Gather rental comps, vacancy rates, and absorption data for your target area. Show that you understand current conditions and have realistic expectations about income potential rather than relying on outdated rent projections.

Document your value-add strategy: If the property requires improvements, provide detailed cost estimates and post-renovation income projections. Lenders respond positively when they see a clear path from acquisition to stabilized cash flow.

Prepare multiple income scenarios: Create conservative, moderate, and optimistic rent projections based on current market data. This shows lenders you've stress-tested the investment and aren't banking on best-case scenarios to make the numbers work.

Organize your track record: Compile performance data from existing properties, especially those that weathered previous downturns. Demonstrating resilience across market cycles can offset lender concerns about current conditions.

Understanding Lender Sensitivity Factors

Understanding lender sensitivity factors helps you anticipate objections and address them proactively. When markets show signs of weakness, lenders adjust their underwriting criteria in specific, predictable ways. Knowing which metrics they're watching most closely allows you to strengthen those areas of your application before submission.

Loan-to-value ratio preferences shift: In declining markets, lenders typically reduce their maximum LTV ratios to protect against further value erosion. Expect lower leverage and plan to bring additional capital to the table if needed.

Reserve requirements increase: Lenders may require larger cash reserves to cover potential vacancy periods or unexpected expenses. Having six to twelve months of debt service in liquid reserves can make your application considerably more attractive.

DSCR minimum thresholds rise: While a 1.0 DSCR might suffice in strong markets, lenders facing rent pressure often require ratios of 1.15 or higher. Structure your purchase price and financing to meet these elevated thresholds.

Property condition scrutiny intensifies: Deferred maintenance becomes a bigger concern when values are declining. Properties in excellent condition with recent capital improvements face less resistance than those requiring immediate work.

Managing Appraisal Risk Effectively

Managing appraisal risk effectively protects your deal from last-minute surprises that can derail financing. Appraisal risk becomes particularly acute in declining markets where recent comparable sales may reflect lower values than properties commanded just months earlier. Traditional appraisal methods might not capture the full income potential of properties with alternative revenue streams or those positioned for repositioning.

Order pre-purchase property inspections: Identifying issues before the lender's appraisal allows you to adjust your offer price or repair budget accordingly. Appraisers may reduce valuations significantly when they discover deferred maintenance or code violations.

Provide appraiser with income documentation: Share existing lease agreements, market rent surveys, and your income projections. While appraisers conduct their own research, providing organized data helps ensure they consider all relevant factors.

Request appraisers experienced with investment properties: Not all appraisers understand income-producing properties equally well. An appraiser familiar with rental valuation methods and DSCR loan requirements will likely produce a more accurate assessment.

Strategic Property Selection in Weak Markets

Strategic property selection in weak markets requires focusing on assets that can weather continued rent pressure while offering upside potential. Not all properties in declining markets present equal risk, and choosing the right asset type makes a substantial difference in both qualifying for financing and achieving positive returns. Markets with slowing construction activity may offer opportunities to acquire properties at reduced prices while facing less new competition for tenants.

Prioritize workforce housing over luxury segments: While some sources indicate both segments face challenges, workforce housing typically recovers faster and maintains higher occupancy during downturns. Properties serving essential workers and moderate-income tenants tend to demonstrate more stable cash flow.

Target properties with below-market rents: Assets where current rents sit 10-20% below market averages provide built-in cushion against further market declines. Even if market rents fall another 5%, you can still implement modest increases as leases turn.

Focus on locations with employment diversity: Markets dependent on single industries face greater volatility. Areas with varied employment bases tend to experience smaller rent swings and recover more quickly, factors that improve lender confidence.

Consider properties with conversion potential: Assets that can shift between long-term and short-term rental strategies offer flexibility if market conditions change. This adaptability can be attractive when presenting your investment thesis to lenders.

Alternative Financing Structures to Consider

Alternative financing structures to consider can provide solutions when traditional DSCR loans prove challenging in declining markets. Several specialized loan products address specific situations that arise when properties show negative cash flow or when conventional underwriting creates obstacles. Understanding these options expands your toolkit for completing acquisitions even during difficult market conditions.

No-ratio DSCR loans for repositioning plays: These products can be effective tools for acquiring properties with temporary cash flow issues while you implement improvement plans. No-ratio structures look at factors beyond immediate income, making them suitable for value-add investments in weakening markets.

Bridge loans for quick acquisition: Short-term bridge financing allows you to secure properties quickly, then refinance into permanent DSCR loans once you've stabilized income. This two-step approach can work well when you need to act fast on discounted properties.

Portfolio loans for multiple properties: If you're acquiring several properties, portfolio lending might offer better terms than individual property loans. Cross-collateralization can strengthen weak properties with stronger performers in your portfolio.

Seller financing combined with DSCR loans: In declining markets, motivated sellers may carry part of the purchase price. Combining seller financing with a DSCR loan reduces the amount you need to borrow and can improve your debt service coverage ratio.

Leveraging Lower Rates and Market Conditions

Leveraging lower rates and market conditions turns potential challenges into advantages for prepared investors. Recent data suggests DSCR loan rates have declined to more competitive levels, potentially signaling increased competition among lenders or underlying market shifts. While declining rates might indicate market weakness, they also create opportunities for refinancing existing properties or acquiring new investments at improved terms.

Refinance underperforming properties to reduce debt service: Lower rates can substantially decrease monthly payments, improving cash flow and DSCR ratios. Properties that struggled at higher rates might become viable investments when refinanced at current pricing.

Lock rates early when application is strong: If you've prepared thoroughly and addressed lender concerns, securing rate locks protects you from potential increases during underwriting. This becomes particularly valuable if market uncertainty could drive rates higher.

Negotiate terms beyond just rate: In competitive lending environments, you might secure favorable prepayment terms, reduced origination fees, or higher loan-to-value ratios. Focus on the complete package rather than rate alone.

Time purchases to capitalize on distress: Declining markets often produce motivated sellers and discounted properties. Securing financing at favorable rates while acquiring assets below replacement cost can generate strong returns when markets eventually stabilize.

Key Takeaway for Investors

The path to securing a DSCR loan for properties in declining markets centers on thorough preparation and strategic positioning. While lender sensitivity naturally increases when managing rent pressure builds and appraisal risk grows, investors who demonstrate market awareness, present conservative projections, and show clear paths to positive cash flow can still access financing. The key lies in addressing lender concerns before they're raised, choosing properties with inherent advantages, and remaining flexible about loan structures when traditional approaches face obstacles.

Market cycles create opportunities for investors willing to do the work that others avoid. Properties acquired during downturns, financed properly, and managed well often generate the strongest long-term returns. Success requires matching the right property with the right financing structure while maintaining realistic expectations about near-term performance.

Securing DSCR financing in declining markets isn't about hiding weakness or hoping lenders overlook unfavorable trends. It's about demonstrating that you understand current conditions, have accounted for continued challenges, and possess both the expertise and resources to navigate volatility. Lenders make loans even in difficult markets, but they do so selectively, favoring borrowers who show preparation and sophistication.

The strategies outlined here, from comprehensive market analysis to alternative financing structures, provide a framework for approaching DSCR loans when conditions aren't ideal. Markets that decline today may present tomorrow's best opportunities, and having financing in place when others struggle to secure capital creates significant competitive advantages. Focus on properties with strong fundamentals, prepare documentation that addresses lender concerns, and remain patient in your search for the right combination of asset and financing terms.

Declining markets test investor discipline and separate those building sustainable portfolios from those chasing short-term gains. By adapting your approach to current conditions while maintaining focus on long-term wealth building, you position yourself to thrive regardless of where the market cycle leads next.