DSCR Loan for California Rental Property: Financing That Works for Investors

California's rental market presents unique opportunities and challenges for real estate investors. High property values often create barriers to traditional financing, yet strong rental demand can generate substantial cash flow. This is where a DSCR loan for California rental property becomes a strategic tool worth considering.

Unlike conventional mortgages that scrutinize your personal income, tax returns, and employment history, DSCR loans focus on one primary metric: the property's ability to cover its own debt. For investors building or scaling rental portfolios in competitive markets like Los Angeles, San Diego, or the Bay Area, this financing approach may offer pathways that traditional lending simply can't match.

In this article, we'll explore how DSCR loans work specifically within California's real estate landscape, what approval considerations matter most, and how savvy investors can leverage property cash flow to expand their holdings despite the state's notoriously high entry costs.

Common Questions About DSCR Loans in California

Common questions about DSCR loans in California often center on how these financing products differ from traditional mortgages and whether they truly simplify the qualification process for rental property investors.

Q: What makes a DSCR loan for California rental property different from a conventional mortgage?

The fundamental difference lies in underwriting criteria. Conventional loans typically require W-2s, tax returns, and verification of personal income. DSCR loans, on the other hand, qualify borrowers based on the rental income the property generates compared to its debt obligations. This approach can be particularly beneficial for self-employed investors, those with complex tax situations, or anyone whose personal income documentation doesn't reflect their actual investment capacity.

Q: Can foreign nationals use DSCR loans to invest in California rental properties?

Yes, DSCR loans may be accessible to foreign nationals looking to enter California's rental market. Since these loans assess property cash flow rather than American income or tax returns, they can remove typical barriers that international investors face. This flexibility potentially widens the pool of capital flowing into California real estate and offers non-U.S. residents a viable path to property ownership based purely on the investment's fundamentals.

Q: Do California state regulations impact DSCR loan terms or availability?

While DSCR loans are structured around property performance rather than borrower income, state regulations around lending practices, property insurance requirements, and rental laws can indirectly affect loan terms. California's specific insurance challenges, such as wildfire and earthquake coverage in certain regions, may influence lender requirements or property eligibility. Working with lenders experienced in California's regulatory environment helps ensure smooth approval processes.

Why DSCR Financing Works Well in California Markets

Why DSCR financing works well in California markets becomes clear when you examine the state's unique combination of high property values and equally strong rental rates. These market dynamics create conditions where property cash flow can support financing even when purchase prices seem daunting.

High rental rates offset property costs: California's rental demand, driven by population density and limited housing supply in key markets, often produces rental income sufficient to achieve favorable debt service coverage ratios. Even though purchase prices run high, the corresponding rental rates may generate enough monthly income to satisfy lender requirements for DSCR loans.

No personal income verification required: For investors who reinvest profits, utilize tax strategies that reduce taxable income, or earn income through non-traditional sources, DSCR loans eliminate the documentation headaches associated with proving personal earnings. This feature proves especially valuable in California, where many successful investors operate multiple LLCs or partnerships.

Portfolio scaling becomes more manageable: When you're not constrained by personal debt-to-income ratios, adding properties to your portfolio depends primarily on finding deals with solid cash flow. This approach allows investors to expand their California holdings based on property fundamentals rather than personal financial snapshots that might not reflect true investment capacity.

Diverse property types qualify: DSCR loans typically work across various property types, including single-family homes, condos, townhomes, and small multifamily buildings. California's diverse real estate landscape offers all these options, enabling investors to diversify their portfolios while using consistent financing structures.

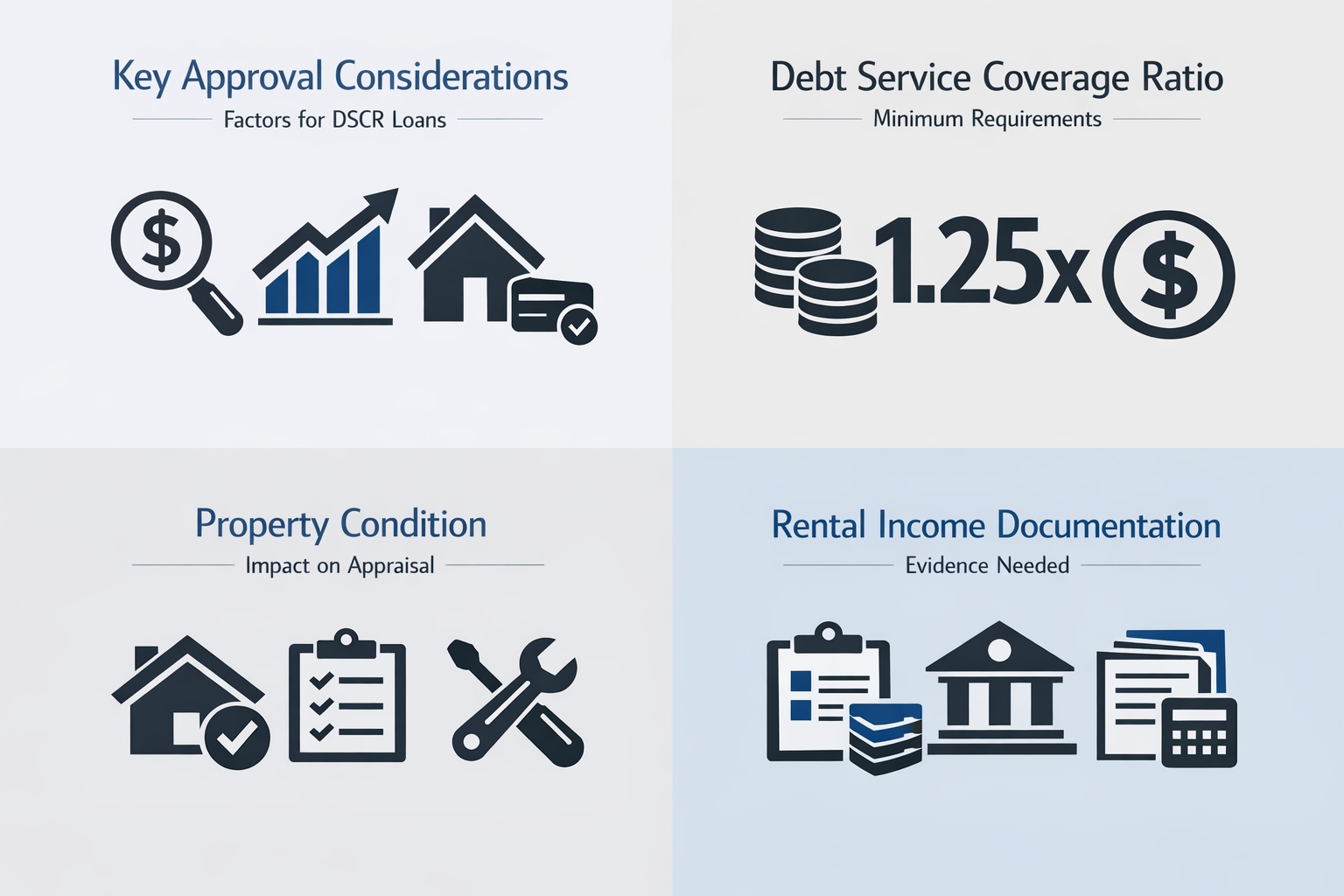

Key Approval Considerations for California Rental Properties

Key approval considerations for California rental properties using DSCR loans revolve around demonstrating that the investment can reliably cover its debt obligations. Understanding what lenders evaluate helps investors prepare stronger applications and select properties more likely to qualify.

Debt Service Coverage Ratio threshold: Lenders typically look for a DSCR of 1.0 or higher, meaning the property's rental income equals or exceeds the monthly debt payment. Many lenders prefer seeing ratios of 1.25 or above for better terms. In California, high rental rates can help achieve these thresholds even on expensive properties, though investors should calculate ratios carefully before making offers.

Property condition and appraisal: The property must appraise at or above the purchase price, and its condition affects both appraisal value and rental income projections. Properties requiring significant repairs might struggle to demonstrate adequate cash flow until renovations are complete. Investors should factor in how condition impacts both immediate qualification and long-term rental potential.

Rental income documentation: Lenders need evidence of current or projected rental income. For occupied properties, this might include existing lease agreements. For vacant properties, lenders may use comparable market rents or appraisal rent schedules. California's varying rental markets mean investors should research area-specific rental comps thoroughly to support their applications.

Reserve requirements: Many DSCR lenders require borrowers to maintain cash reserves equivalent to several months of debt payments. This protects against vacancy or unexpected expenses. Reserve requirements can vary, so investors should clarify these expectations upfront and plan liquidity accordingly.

Navigating California Insurance Challenges

Navigating California insurance challenges represents a critical approval consideration that can affect both loan qualification and ongoing investment profitability. The state's exposure to natural disasters and evolving insurance marketplace create unique hurdles for rental property investors.

Wildfire and earthquake coverage: Properties in certain California regions may require specialized insurance for wildfire or earthquake risks. Lenders typically mandate adequate hazard insurance as a loan condition, and in some high-risk areas, obtaining affordable coverage has become increasingly difficult. Investors should verify insurance availability and costs before committing to properties in fire-prone zones.

Rising insurance premiums: California has seen insurance carriers exit certain markets or dramatically increase premiums. These cost increases directly impact property cash flow and, consequently, DSCR calculations. When underwriting potential acquisitions, investors should use current insurance quotes rather than seller-provided figures, which might not reflect current market rates.

Lender insurance requirements: Beyond state minimums, DSCR lenders often have specific coverage requirements that might exceed standard policies. This could include higher liability limits, loss of rents coverage, or flood insurance in designated zones. Understanding these requirements early helps investors budget accurately and avoid surprises during the approval process.

Strategic Steps to Secure DSCR Loan Approval

Strategic steps to secure DSCR loan approval in California start well before you submit an application. Preparation and property selection significantly influence whether your financing comes through smoothly or faces unnecessary delays.

Run preliminary DSCR calculations on potential properties: Before making offers, calculate the expected DSCR using realistic rental income projections and estimated debt payments. Include property taxes, insurance, HOA fees if applicable, and the anticipated loan payment. This preliminary analysis helps you identify which properties will likely qualify and allows you to negotiate purchase prices that support favorable ratios.

Gather rental market data for your target area: Compile recent rental comps, vacancy rates, and market trends for the neighborhoods you're considering. This documentation supports your income projections and demonstrates market knowledge to lenders. California's rental markets vary dramatically by region, so hyperlocal data proves more valuable than statewide averages.

Connect with lenders experienced in California investment properties: Not all DSCR lenders operate in every state or understand California's specific regulatory environment and insurance landscape. Working with lenders who regularly close California rental property investors loans can streamline approval and help you navigate state-specific challenges more effectively.

Prepare reserves and down payment documentation: Even though DSCR loans don't scrutinize personal income, you'll still need to demonstrate available funds for down payments and reserves. Organize bank statements and asset documentation in advance. Most DSCR loans require larger down payments than conventional mortgages, often 20-25% or more, so ensure your capital is properly positioned.

Consider timing and rate lock opportunities: Interest rate movements can significantly impact both your monthly debt service and the property's DSCR. When market conditions present favorable rates, locking them in quickly may improve your deal economics. Stay informed about rate trends and be prepared to move decisively when opportunities arise.

Property Types and Portfolio Diversification

Property types and portfolio diversification matter when building a California rental portfolio using DSCR financing. Understanding which property categories typically qualify helps investors make strategic acquisition decisions aligned with their investment goals.

Single-family residences: These properties often represent the most straightforward path to DSCR loan approval. They typically attract stable, long-term tenants and have clear rental comp data. California's strong single-family rental market in both urban and suburban areas makes these properties reliable cash flow generators, particularly in markets where homeownership remains out of reach for many residents.

Condos and townhomes: These property types can work well for DSCR loans, though investors should verify that the development is warrantable and meets lender requirements. HOA fees must be factored into DSCR calculations, and some lenders have restrictions on condo concentrations in their portfolios. California's coastal markets and urban centers offer numerous condo opportunities where rental demand remains consistently strong.

Small multifamily properties: Duplexes, triplexes, and fourplexes can be excellent DSCR loan candidates because multiple units provide income diversification within a single property. Vacancy in one unit doesn't eliminate all rental income, potentially making these properties more resilient. California's multifamily markets in established neighborhoods often generate attractive cash-on-cash returns.

Balancing property types across your portfolio: Using DSCR loans to acquire different property types helps spread risk across various market segments and tenant demographics. A mix of single-family homes and small multifamily buildings, for example, can provide both appreciation potential and steady cash flow while protecting against market shifts that might affect one property type more than another.

Maximizing Returns With Cash Flow-Based Financing

Maximizing returns with cash flow-based financing requires investors to think differently about property selection and portfolio management. When qualification depends on property performance rather than personal income, different strategies come into play.

Focus on properties where rental rates substantially exceed debt service. California markets with strong employment centers, limited new construction, or demographic tailwinds often produce the rent growth and occupancy rates that support healthy DSCRs. Properties that barely meet minimum ratio requirements leave little margin for error if vacancy occurs or expenses increase.

Consider properties with value-add potential that can boost rental income after acquisition. Cosmetic improvements, unit upgrades, or better property management might increase achievable rents by 10-20%, significantly improving your DSCR and overall returns. California's diverse housing stock includes many properties where modest investments yield substantial rent increases.

Monitor ongoing property performance to maintain favorable ratios. Even after closing, your DSCR matters for future refinancing opportunities or additional acquisitions. Keeping rents at market rates, controlling expenses, and maintaining high occupancy ensures your properties continue to perform well by the metrics that matter most for this financing approach.

Build relationships with lenders who offer competitive DSCR loan terms. As you prove yourself with successful properties and timely payments, you may gain access to better rates, higher leverage, or more flexible underwriting on subsequent deals. California's large investment property market means multiple lenders compete for quality borrowers, potentially giving experienced investors negotiating leverage.

A DSCR loan for California rental property offers investors a powerful alternative to conventional financing, particularly in markets where high property values might otherwise create barriers to entry or portfolio expansion. By qualifying based on rental income rather than personal financial documentation, these loans align perfectly with the realities of professional real estate investing.

California's combination of strong rental demand, diverse property types, and substantial appreciation potential creates an environment where cash flow-based financing can truly shine. Whether you're acquiring your first rental property or adding to an established portfolio, understanding how DSCR loans work within California's specific regulatory and insurance landscape positions you to make smarter acquisition decisions.

Success with DSCR financing comes down to thorough preparation: running accurate cash flow projections, understanding approval considerations, securing adequate insurance coverage, and selecting properties with fundamentals strong enough to support themselves financially. When you approach California rental property investment with these principles in mind, DSCR loans become more than just a financing tool. They become a strategic advantage that lets you scale based on deal quality rather than artificial constraints.

The California rental market continues to evolve, but properties that generate solid cash flow relative to their debt will always attract financing. By mastering DSCR loan strategies, you position yourself to capitalize on opportunities that other investors, constrained by traditional lending requirements, might have to pass up.