Real estate investors pursuing DSCR loan financing often encounter unexpected hurdles during the appraisal process. While DSCR loans focus primarily on rental income rather than personal income, the property valuation remains a crucial component that can make or break your deal. Understanding common DSCR loan appraisal issues helps investors prepare for potential challenges and develop effective strategies to overcome valuation obstacles that might otherwise derail profitable investment opportunities.

Common DSCR Loan Appraisal Challenges

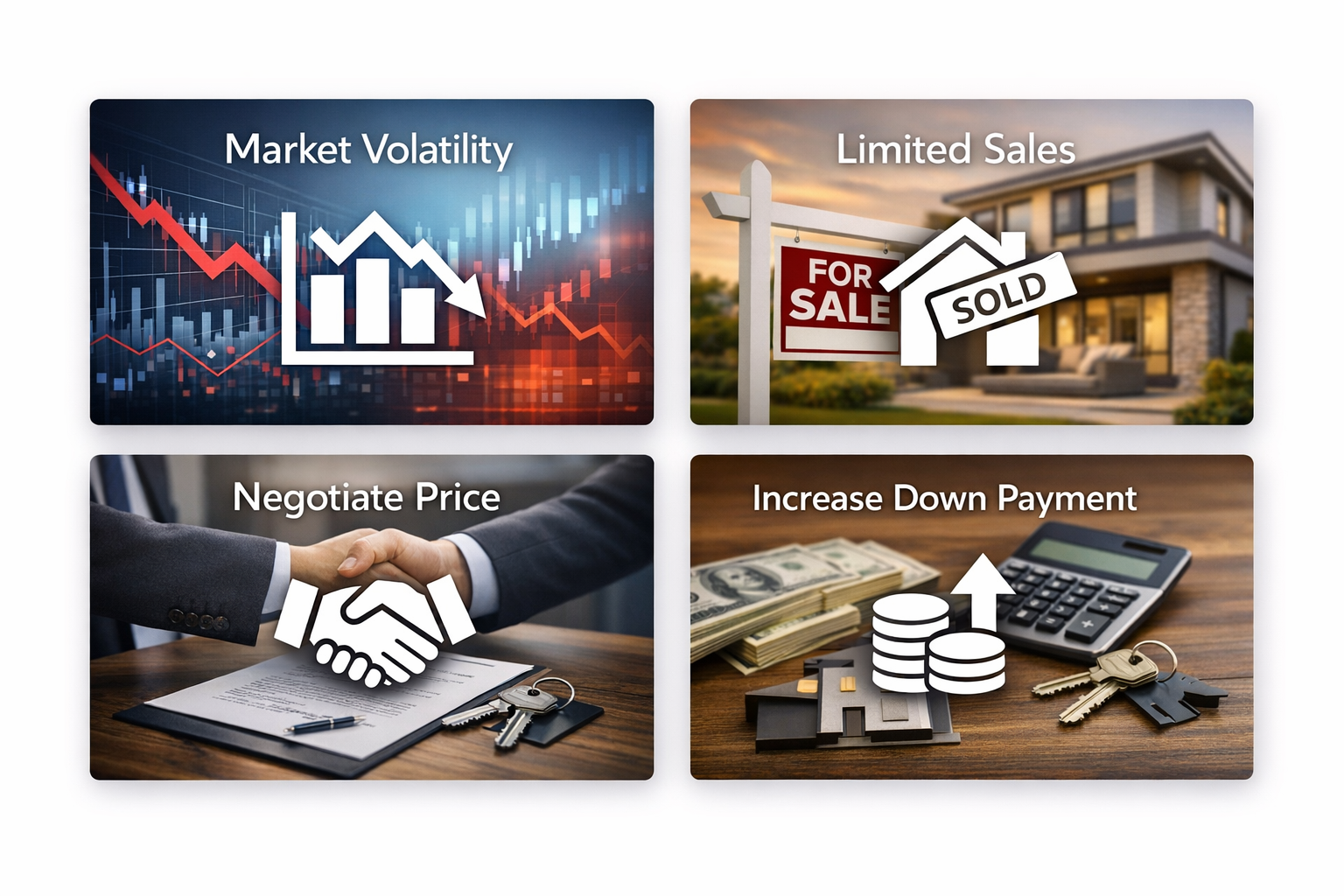

DSCR loan appraisal issues typically emerge from several key factors that investors should anticipate. The appraisal process for investment properties often presents unique complications that differ from owner-occupied residential evaluations.

Market volatility impacts: Rapidly changing market conditions can create discrepancies between purchase contracts and current valuations, particularly in areas experiencing significant price fluctuations

Limited comparable sales: Investment properties in certain markets may have insufficient recent sales data, making accurate valuations challenging for appraisers

Property condition assessments: Appraisers might identify maintenance issues or needed improvements that weren't initially apparent during property inspections

Income approach complications: For rental properties, appraisers must consider both market value and income potential, which can sometimes conflict with investor expectations

Low Appraisal Solutions for Investors

When faced with a low appraisal on your DSCR loan, several low appraisal solutions can help salvage your investment deal. The key is acting quickly and strategically to address the valuation gap.

Negotiate purchase price reductions: Work with sellers to lower the contract price to match the appraised value, maintaining your original loan-to-value ratio

Increase down payment: Bridge the gap between appraised value and purchase price with additional cash, though this impacts your return calculations

Request value reconsideration: Submit additional comparable sales data or property improvement documentation to support a higher valuation

Seek second appraisal opinions: Some lenders may allow alternative appraisals, though this typically extends closing timelines and increases costs

Comps Selection Strategies

Effective comps selection can significantly influence appraisal outcomes for DSCR loans. Investors who understand how appraisers evaluate comparable properties can better position their deals for successful valuations.

Geographic proximity focus: Identify recent sales within a half-mile radius when possible, as appraisers typically prioritize nearby transactions over distant comparables

Property type matching: Ensure comparable properties share similar characteristics such as single-family versus multi-unit, age ranges, and square footage within reasonable parameters

Sale date relevance: Focus on transactions within the past six months, as older sales may carry less weight in current market valuations

Condition considerations: Select comparables that reflect similar property conditions and improvement levels to support accurate value assessments

Value Reconsideration Process

The value reconsideration process offers investors a formal mechanism to challenge low appraisals with additional supporting documentation. This approach requires careful preparation and strategic presentation of relevant market data.

Document preparation requirements: Gather recent comparable sales, property improvement records, and market analysis reports that support your target valuation

Professional presentation standards: Submit requests through proper channels with organized supporting materials and clear explanations of valuation discrepancies

Timeline management: Account for additional processing time, typically 5-10 business days, when planning closing schedules and contract deadlines

Success probability factors: Understand that reconsideration requests succeed most often when backed by compelling new comparable sales data or significant property improvements

Preparing for DSCR Appraisal Success

Proactive preparation can minimize DSCR loan appraisal issues before they become deal-breaking obstacles. Smart investors take specific steps to position their properties favorably for the valuation process.

Conduct preliminary market analysis: Research recent comparable sales in your target area before making offers to ensure realistic price expectations align with current market conditions

Complete necessary repairs: Address obvious maintenance issues and cosmetic improvements that could negatively impact appraiser perceptions and final valuations

Organize property documentation: Compile improvement records, rental agreements, and property tax assessments that demonstrate value-adding investments and income potential

Coordinate with your lender: Maintain open communication about appraisal timing and requirements to avoid last-minute complications that could delay closing schedules

Working with DSCR Lenders on Appraisal Issues

Building strong relationships with DSCR lenders who understand investment property challenges can provide valuable support when appraisal issues arise. Experienced lenders often offer flexibility and solutions that less specialized institutions might not provide.

Choose experienced investment lenders: Partner with lenders who regularly handle DSCR loans and understand the unique appraisal challenges that investment properties present

Discuss appraisal concerns upfront: Address potential valuation risks during the initial loan application process to establish realistic expectations and contingency plans

Leverage lender networks: Work with lenders who maintain relationships with appraisers experienced in investment property valuations and local market conditions

Explore alternative solutions: Discuss options such as portfolio lending or asset-based lending if traditional appraisal methods consistently undervalue your investment properties

Successfully navigating DSCR loan appraisal issues requires preparation, market knowledge, and strategic partnerships with experienced lenders. While appraisal challenges can complicate investment deals, understanding common problems and available solutions helps investors maintain deal momentum even when valuations fall short of expectations. As DSCR loan demand continues to grow in 2026, investors who master the appraisal process will find themselves better positioned to secure favorable financing for their real estate portfolios. Remember that each appraisal challenge represents a learning opportunity that can improve your future deal evaluation and negotiation strategies.